Blog Archives

Transforming Finance: From ERP to Real-Time Decision Making

There was a time when the role of the CFO could be summarized with a handful of verbs: report, reconcile, allocate, forecast. In the 20th century, the finance office was a bastion of structure and control. The CFO was the high priest of compliance and the gatekeeper of capital. The systems were linear, the rhythms were quarterly, and the decisions were based on historical truths.

That era has passed. In its place emerges the Digital CFO 3.0 – a new kind of enterprise leader who moves beyond control towers and static spreadsheets to architect digital infrastructure, orchestrate intelligent systems, and enable predictive, adaptive, and real-time decision-making across the enterprise.

This is not a change in tools. It is a change in mindset, muscle, and mandate.

The Digital CFO 3.0 is not just a steward of financial truth. They are a strategic systems architect, a data supply chain engineer, and a design thinker for the cognitive enterprise. Their domain now includes APIs, cloud data lakes, process automation, AI-enabled forecasting, and trust-layer governance models. They must reimagine the finance function not as a back-office cost center, but as the neural core of a learning organization.

Let us explore the core principles, capabilities, and operating architecture that define this new role, and how today’s finance leaders must prepare to build the infrastructure of the future enterprise.

1. From Monolithic ERP to Modular Intelligence

Traditional finance infrastructure was built on monolithic ERP systems – massive, integrated, but inflexible. Every upgrade was painful. Data latency was high. Insight was slow.

The Digital CFO 3.0 shifts toward a modular, composable architecture. Finance tools are API-connected, event-driven, and cloud-native. Data moves in real time through finance operations, from procure-to-pay to order-to-cash.

- Core systems remain but are surrounded by microservices for specific tasks: forecasting, scenario modeling, spend analytics, compliance monitoring.

- Data lakes and warehouses serve as integration layers, decoupling applications from reporting.

- AI and ML modules plug into these environments to generate insights on demand.

This architecture enables agility. New use cases can be spun up quickly. Forecasting models can be retrained in hours, not months. Finance becomes a responsive, intelligent grid rather than a transactional pipe.

2. Finance as a Real-Time Operating System

In legacy models, finance operated in batch mode: monthly closes, quarterly forecasts, annual planning. But the modern enterprise operates in real time. Markets shift hourly. Customer behavior changes daily. Capital decisions must respond accordingly.

The Digital CFO builds a real-time finance engine:

- Continuous Close: Transactions are reconciled daily, not monthly. Variances are flagged immediately. The books are always nearly closed.

- Rolling Forecasting: Plans update with each new signal – not by calendar, but by context.

- Embedded Analytics: Metrics travel with the business – inside CRM, procurement, inventory, and workforce systems.

- Streaming KPIs: Finance watches the enterprise like a heart monitor, not a photograph.

This changes how decisions are made. Instead of waiting for reports, leaders ask questions in the flow of business – and get answers in seconds.

3. Trust by Design: The New Governance Layer

As data velocity increases, so does the risk of error, bias, and misinterpretation. The CFO has always been a guardian of trust. But for the Digital CFO 3.0, this mandate extends to the digital trust layer:

- Data Lineage: Every number is traceable. Every transformation is logged.

- Model Governance: AI models used in finance must be explainable, auditable, and ethical.

- Access Control: Fine-grained permissions ensure only the right people see the right numbers.

- Validation Rules: Embedded in pipelines to flag anomalies before they reach the dashboard.

Trust is not a byproduct of strong reporting. It is an outcome of intentional design.

4. Orchestrating the Intelligent Workflow

In the digital enterprise, no team operates in isolation. Sales, operations, procurement, HR are interconnected. The Digital CFO 3.0 builds infrastructure to orchestrate intelligent workflows across silos.

- AP automation connects with vendor portals and treasury systems.

- Forecast adjustments trigger alerts to sourcing and demand planning teams.

- Employee cost changes ripple through headcount plans and productivity dashboards.

This orchestration requires more than software. It demands process choreography and data interoperability. The CFO becomes the conductor of a distributed, dynamic finance system.

5. Redesigning Talent for a Cognitive Finance Team

Digital infrastructure is only as powerful as the team that runs it. The finance org of the future looks different:

- Analysts become insight designers, curating stories from signals.

- Controllers become data quality stewards.

- FP&A teams become simulation strategists.

- Finance business partners become embedded value engineers.

The Digital CFO invests in technical fluency, data storytelling, and systems thinking. Upskilling is continuous. Learning velocity becomes a core KPI.

6. From Reporting the Past to Architecting the Future

Ultimately, the Digital CFO 3.0 is not building systems to describe yesterday. They are designing infrastructure to anticipate tomorrow:

- Capex investments are modeled across geopolitical scenarios.

- ESG metrics are embedded into supplier scoring and budget cycles.

- Strategic choices are evaluated with real option models and probabilistic simulations.

- M&A integration plans are automated, with finance playbooks triggered by transaction type.

The finance function becomes a predictive nerve center, informing everything from product pricing to market entry.

Conclusion: The CFO as Enterprise Architect

The shift to Digital CFO 2.0 is not optional. It is inevitable. Markets are faster. Technology is smarter. Stakeholders expect more. What was once a support function is now a strategic command center.

This is not about buying tools. It is about designing an operating system for the enterprise that is intelligent, adaptive, and deeply aligned with value creation.

The future CFO does not just report results. They engineer outcomes. They do not just forecast growth. They architect the infrastructure to make it happen.

How Strategic CFOs Drive Sustainable Growth and Change

When people ask me what the most critical relationship in a company really is, I always say it’s the one between the CEO and the CFO. And no, I am not being flippant. In my thirty years helping companies manage growth, navigate crises, and execute strategic shifts, the moments that most often determine success or spiraled failure often rests on how tightly the CEO and CFO operate together. One sets a vision. The other turns aspiration into action. Alone, each has influence; together, they can transform the business.

Transformation, after all, is not a project. It is a culture shift, a strategic pivot, a redefinition of operating behaviors. It’s more art than engineering and more people than process. And at the heart of it lies a fundamental tension: You need ambition, yet you must manage risk. You need speed, but you cannot abandon discipline. You must pursue new business models while preserving your legacy foundations. In short, you need to build simultaneously on forward momentum and backward certainty.

That complexity is where the strategic CFO becomes indispensable. The CFO’s job is not just to count beans, it’s to clear the ground where new plants can grow. To unlock capital without unleashing chaos. To balance accountable rigor with growth ambition. To design transformation from the numbers up, not just hammer it into the planning cycle. When this role is fulfilled, the CEO finds their most trusted confidante, collaborator, and catalyst.

Think of it this way. A CEO paints a vision: We must double revenue, globalize our go-to-market, pivot into new verticals, revamp the product, or embrace digital. It sounds exciting. It feels bold. But without a financial foundation, it becomes delusional. Does the company have the cash runway? Can the old cost base support the new trajectory? Are incentives aligned? Are the systems ready? Will the board nod or push back? Who is accountable if sales forecast misses or an integration falters? A CFO’s strategic role is to bring those questions forward not cynically, but constructively—so the ambition becomes executable.

The best CEOs I’ve worked with know this partnership instinctively. They build strategy as much with the CFO as with the head of product or sales. They reward honest challenge, not blind consensus. They request dashboards that update daily, not glossy decks that live in PowerPoint. They ask, “What happens to operating income if adoption slows? Can we reverse full-time hiring if needed? Which assumptions unlock upside with minimal downside?” Then they listen. And change. That’s how transformation becomes durable.

Let me share a story. A leader I admire embarked on a bold plan: triple revenue in two years through international expansion and a new channel model. The exec team loved the ambition. Investors cheered. But the CFO, without hesitation, did not say no. She said let us break it down. Suppose it costs $30 million to build international operations, $12 million to fund channel enablement, plus incremental headcount, marketing expenses, R&D coordination, and overhead. Let us stress test the plan. What if licensing stalls? What if fulfillment issues delay launches? What if cross-border tax burdens permanently drag down the margin?

The CEO wanted the bold headline number. But together, they translated it into executable modules. They set up rolling gates: a $5 million pilot, learn, fund next $10 million, learn, and so on. They built exit clauses. They aligned incentives so teams could pivot without losing credibility. They also built redundancy into systems and analytics, with daily data and optionality-based budgeting. The CEO had the vision, but the CFO gave it a frame. That is partnership.

That framing role extends beyond capital structure or P&L. It bleeds into operating rhythm. The strategic CFO becomes the architect of transformation cadence. They design how weekly, monthly, and quarterly look and feel. They align incentive schemes so that geography may outperform globally while still holding central teams accountable. They align finance, people, product, and GTM teams to shared performance metrics—not top-level vanity metrics, but actionable ones: user engagement, cost per new customer, onboarding latency, support burden, renewal velocity. They ensure data is not stashed in silos. They make it usable, trusted, visible. Because transformation is only as effective as your ability to measure missteps, iterate, and learn.

This is why I say the CFO becomes a strategic weapon: a lever for insight, integration, and investment.

Boards understand this too, especially when it is too late. They see CEOs who talk of digital transformation while still approving global headcount hikes. They see operating legacy systems still dragging FY ‘Digital 2.0’ ambition. They see growth funded, but debt rising with little structural benefit. In those moments, they turn to the CFO. The board does not ask the CFO if they can deliver the numbers. They ask whether the CEO can. They ask, “What’s the downside exposure? What are the guardrails? Who is accountable? How long will transformation slow profitability? And can we reverse if needed?”

That board confidence, when positive, is not accidental. It comes from a CFO who built that trust, not by polishing a spreadsheet, but by building strategy together, testing assumptions early, and designing transformation as a financial system.

Indeed, transformation without control is just creative destruction. And while disruption may be trendy, few businesses survive without solid footing. The CFO ensures that disruption does not become destruction. That investments scale with impact. That flexibility is funded. That culture is not ignored. That when exceptions arise, they do not unravel behaviors, but refocus teams.

This is often unseen. Because finance is a support function, not a front-facing one. But consider this: it is finance that approves the first contract. Finance assists in setting the commission structure that defines behavior. Finance sets the credit policy, capital constraints, and invoice timing, and all of these have strategic logic. A CFO who treats each as a tactical lever becomes the heart of transformation.

Take forecasting. Transformation cannot run on backward-moving averages. Yet too many companies rely on year-over-year rates, lagged signals, and static targets. The strategic CFO resurrects forecasting. They bring forward leading indicators of product usage, sales pipeline, supply chain velocity. They reframe forecasts as living systems. We see a dip? We call a pivot meeting. We see high churn? We call the product team. We see hiring cost creep? We call HR. Forewarned is forearmed. That is transformation in flight.

On the capital front, the CFO becomes a barbell strategist. They pair patient growth funding with disciplined structure. They build in fields of optionality: reserves for opportunistic moves, caps on unfunded headcount, staged deployment, and scalable contracts. They calibrate pricing experiments. They design customer acquisition levers with off ramps. They ensure that at every step of change, you can set a gear to reverse—without losing momentum, but with discipline.

And they align people. Transformation hinges on mindset. In fast-moving companies, people often move faster than they think. Great leaders know this. The strategic CFO builds transparency into compensation. They design equity vesting tied to transformation metrics. They design long-term incentives around cross-functional execution. They also design local authority within discipline. Give leaders autonomy, but align them to the rhythm of finance. Even the best strategy dies when every decision is a global approval. Optionality must scale with coordination.

Risk management transforms too. In the past, the CFO’s role in transformation was to shield operations from political turbulence. Today, it is to internally amplify controlled disruption. That means modeling volatility with confidence. Scenario modeling under market shock, regulatory shift, customer segmentation drift. Not just building firewalls, but designing escape ramps and counterweights. A transformation CFO builds risk into transformation—but as a system constraint to be managed, not a gate to prevent ambition.

I once had a CEO tell me they felt alone when delivering digital transformation. HR was not aligned. Product was moving too slowly. Sales was pushing legacy business harder. The CFO had built a bridge. They brought HR, legal, sales, and marketing into weekly update sessions, each with agreed metrics. They brokered resolutions. They surfaced trade-offs confidently. They pressed accountability floor—not blame, but clarity. That is partnership. That is transformation armor.

Transformation also triggers cultural tectonics. And every tectonic shift features friction zones—power renegotiation, process realignment, work redesign. Without financial discipline, politics wins. Mistrust builds. Change derails. The strategic CFO intervenes not as a policeman, but as an arbiter of fairness: If people are asked to stretch, show them the ROI. If processes migrate, show them the rationale. If roles shift, unpack the logic. Maintaining trust alignment during transformation is as important as securing funding.

The ability to align culture, capital, cadence, and accountability around a single north star—that is the strategic CFO’s domain.

And there is another hidden benefit: the CFO’s posture sets the tone for transformation maturity. CFOs who co-create, co-own, and co-pivot build transformation muscle. Those companies that learn together scale transformation together.

I once wrote that investors will forgive a miss if the learning loops are obvious. That is also true inside the company. When a CEO and CFO are aligned, and the CFO is the first to acknowledge what is not working to expectations, when pivots are driven by data rather than ego, that establishes the foundation for resilient leadership. That is how companies rebuild trust in growth every quarter. That is how transformation becomes a norm.

If there is a fear inside the CFO community, it is the fear of being visible. A CFO may believe that financial success is best served quietly. But the moment they step confidently into transformation, they change that dynamic. They say: Yes, we own the books. But we also own the roadmap. Yes, we manage the tail risk. But we also amplify the tail opportunity. That mindset is contagious. It builds confidence across the company and among investors. That shift in posture is more valuable than any forecast.

So let me say it again. Strategy is not a plan. Mechanics do not make execution. Systems do. And at the junction of vision and execution, between boardroom and frontline, stands the CFO. When transformation is on the table, the CFO walks that table from end to end. They make sure the chairs are aligned. The evidence is available. The accountability is shared. The capital is allocated, measured, and adapted.

This is why I refer to the CFO as the CEO’s most important ally. Not simply a confidante. Not just a number-cruncher. A partner in purpose. A designer of execution. A steward of transformation. Which is why, if you are a CFO reading this, I encourage you: step forward. You do not need permission to rethink transformation. You need conviction to shape it. And if you can build clarity around capital, establish a cadence for metrics, align incentives, and implement systems for governance, you will make your CEO’s job easier. You will elevate your entire company. You will unlock optionality not just for tomorrow, but for the years that follow. Because in the end, true transformation is not a moment. It is a movement. And the CFO, when prepared, can lead it.

Bias and Error: Human and Organizational Tradeoff

“I spent a lifetime trying to avoid my own mental biases. A.) I rub my own nose into my own mistakes. B.) I try and keep it simple and fundamental as much as I can. And, I like the engineering concept of a margin of safety. I’m a very blocking and tackling kind of thinker. I just try to avoid being stupid. I have a way of handling a lot of problems — I put them in what I call my ‘too hard pile,’ and just leave them there. I’m not trying to succeed in my ‘too hard pile.’” : Charlie Munger — 2020 CalTech Distinguished Alumni Award interview

Bias is a disproportionate weight in favor of or against an idea or thing, usually in a way that is closed-minded, prejudicial, or unfair. Biases can be innate or learned. People may develop biases for or against an individual, a group, or a belief. In science and engineering, a bias is a systematic error. Statistical bias results from an unfair sampling of a population, or from an estimation process that does not give accurate results on average.

Error refers to a outcome that is different from reality within the context of the objective function that is being pursued.

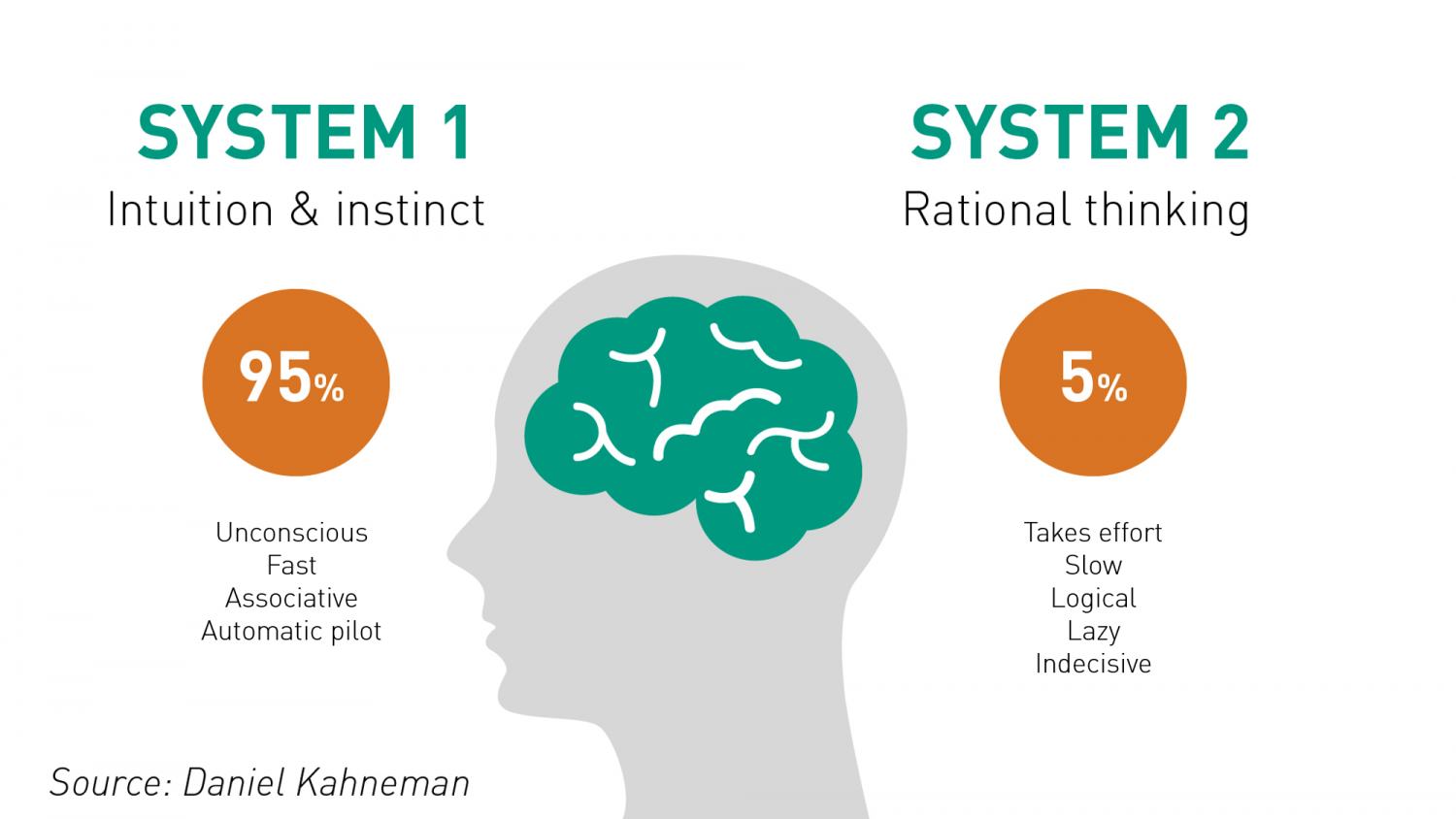

Thus, I would like to think that the Bias is a process that might lead to an Error. However, that is not always the case. There are instances where a bias might get you to an accurate or close to an accurate result. Is having a biased framework always a bad thing? That is not always the case. From an evolutionary standpoint, humans have progressed along the dimension of making rapid judgements – and much of them stemming from experience and their exposure to elements in society. Rapid judgements are typified under the System 1 judgement (Kahneman, Tversky) which allows bias and heuristic to commingle to effectively arrive at intuitive decision outcomes.

And again, the decision framework constitutes a continually active process in how humans or/and organizations execute upon their goals. It is largely an emotional response but could just as well be an automated response to a certain stimulus. However, there is a danger prevalent in System 1 thinking: it might lead one to comfortably head toward an outcome that is seemingly intuitive, but the actual result might be significantly different and that would lead to an error in the judgement. In math, you often hear the problem of induction which establishes that your understanding of a future outcome relies on the continuity of the past outcomes, and that is an errant way of thinking although it still represents a useful tool for us to advance toward solutions.

System 2 judgement emerges as another means to temper the more significant variabilities associated with System 1 thinking. System 2 thinking represents a more deliberate approach which leads to a more careful construct of rationale and thought. It is a system that slows down the decision making since it explores the logic, the assumptions, and how the framework tightly fits together to test contexts. There are a more lot more things at work wherein the person or the organization has to invest the time, focus the efforts and amplify the concentration around the problem that has to be wrestled with. This is also the process where you search for biases that might be at play and be able to minimize or remove that altogether. Thus, each of the two Systems judgement represents two different patterns of thinking: rapid, more variable and more error prone outcomes vs. slow, stable and less error prone outcomes.

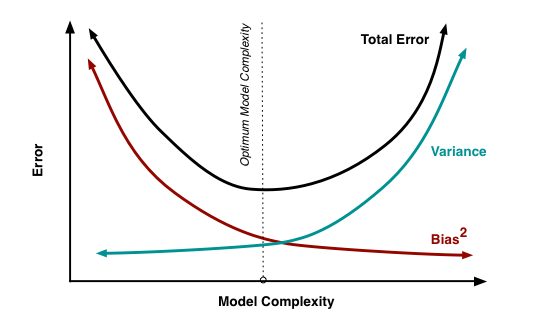

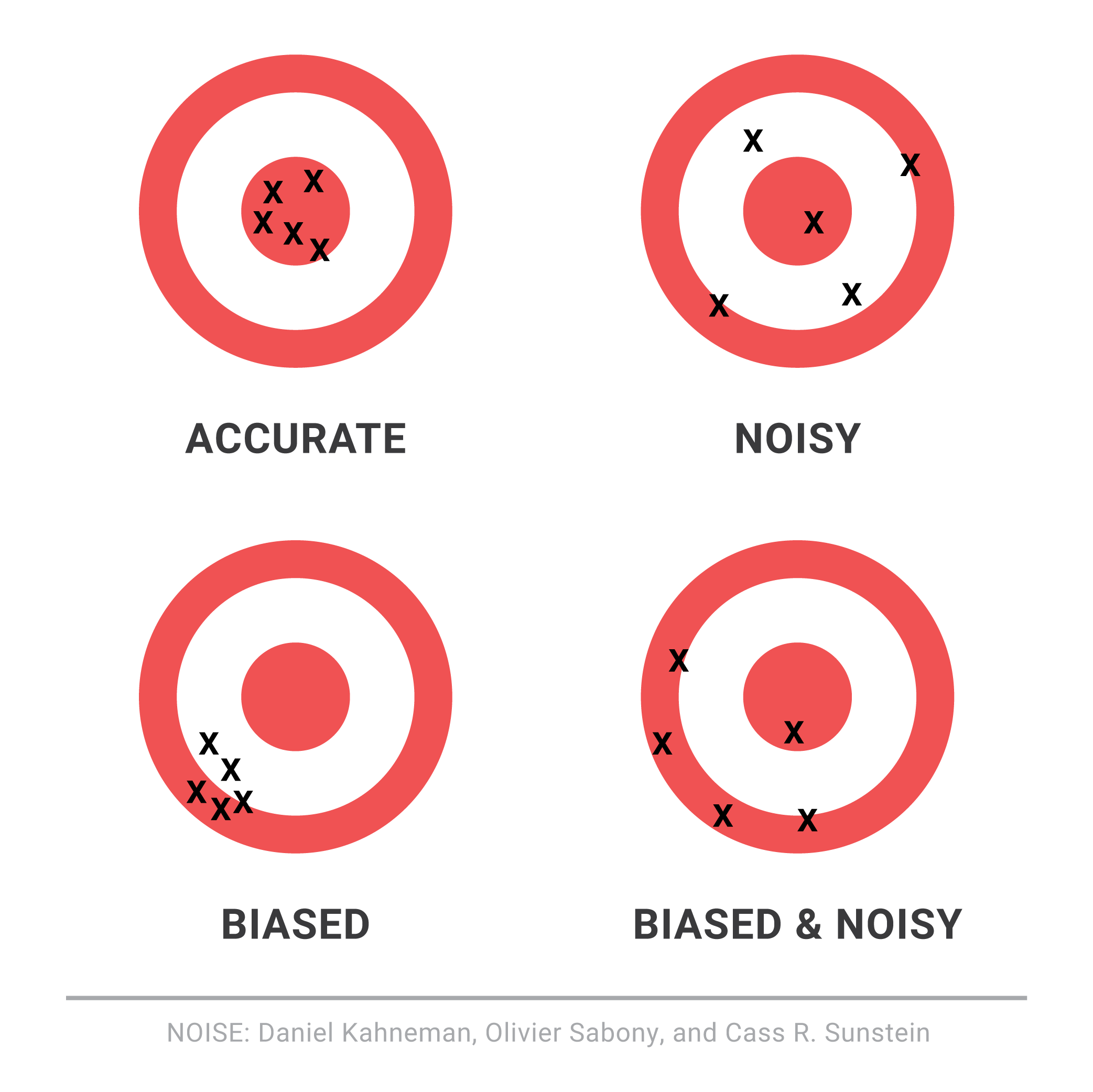

So let us revisit the Bias vs. Variance tradeoff. The idea is that the more bias you bring to address a problem, there is less variance in the aggregate. That does not mean that you are accurate. It only means that there is less variance in the set of outcomes, even if all of the outcomes are materially wrong. But it limits the variance since the bias enforces a constraint in the hypotheses space leading to a smaller and closely knit set of probabilistic outcomes. If you were to remove the constraints in the hypotheses space – namely, you remove bias in the decision framework – well, you are faced with a significant number of possibilities that would result in a larger spread of outcomes. With that said, the expected value of those outcomes might actually be closer to reality, despite the variance – than a framework decided upon by applying heuristic or operating in a bias mode.

So how do we decide then? Jeff Bezos had mentioned something that I recall: some decisions are one-way street and some are two-way. In other words, there are some decisions that cannot be undone, for good or for bad. It is a wise man who is able to anticipate that early on to decide what system one needs to pursue. An organization makes a few big and important decisions, and a lot of small decisions. Identify the big ones and spend oodles of time and encourage a diverse set of input to work through those decisions at a sufficiently high level of detail. When I personally craft rolling operating models, it serves a strategic purpose that might sit on shifting sands. That is perfectly okay! But it is critical to evaluate those big decisions since the crux of the effectiveness of the strategy and its concomitant quantitative representation rests upon those big decisions. Cutting corners can lead to disaster or an unforgiving result!

I will focus on the big whale decisions now. I will assume, for the sake of expediency, that the series of small decisions, in the aggregate or by itself, will not sufficiently be large enough that it would take us over the precipice. (It is also important however to examine the possibility that a series of small decisions can lead to a more holistic unintended emergent outcome that might have a whale effect: we come across that in complexity theory that I have already touched on in a set of previous articles).

Cognitive Biases are the biggest mea culpas that one needs to worry about. Some of the more common biases are confirmation bias, attribution bias, the halo effect, the rule of anchoring, the framing of the problem, and status quo bias. There are other cognition biases at play, but the ones listed above are common in planning and execution. It is imperative that these biases be forcibly peeled off while formulating a strategy toward problem solving.

But then there are also the statistical biases that one needs to be wary of. How we select data or selection bias plays a big role in validating information. In fact, if there are underlying statistical biases, the validity of the information is questionable. Then there are other strains of statistical biases: the forecast bias which is the natural tendency to be overtly optimistic or pessimistic without any substantive evidence to support one or the other case. Sometimes how the information is presented: visually or in tabular format – can lead to sins of the error of omission and commission leading the organization and judgement down paths that are unwarranted and just plain wrong. Thus, it is important to be aware of how statistical biases come into play to sabotage your decision framework.

One of the finest illustrations of misjudgment has been laid out by Charlie Munger. Here is the excerpt link : https://fs.blog/great-talks/psychology-human-misjudgment/ He lays out a very comprehensive 25 Biases that ail decision making. Once again, stripping biases do not necessarily result in accuracy — it increases the variability of outcomes that might be clustered around a mean that might be closer to accuracy than otherwise.

Variability is Noise. We do not know a priori what the expected mean is. We are close, but not quite. There is noise or a whole set of outcomes around the mean. Viewing things closer to the ground versus higher would still create a likelihood of accepting a false hypothesis or rejecting a true one. Noise is extremely hard to sift through, but how you can sift through the noise to arrive at those signals that are determining factors, is critical to organization success. To get to this territory, we have eliminated the cognitive and statistical biases. Now is the search for the signal. What do we do then? An increase in noise impairs accuracy. To improve accuracy, you either reduce noise or figure out those indicators that signal an accurate measure.

This is where algorithmic thinking comes into play. You start establishing well tested algorithms in specific use cases and cross-validate that across a large set of experiments or scenarios. It has been proved that algorithmic tools are, in the aggregate, superior to human judgement – since it systematically can surface causal and correlative relationships. Furthermore, special tools like principal component analysis and factory analysis can incorporate a large input variable set and establish the patterns that would be impregnable for even System 2 mindset to comprehend. This will bring decision making toward the signal variants and thus fortify decision making.

The final element is to assess the time commitment required to go through all the stages. Given infinite time and resources, there is always a high likelihood of arriving at those signals that are material for sound decision making. Alas, the reality of life does not play well to that assumption! Time and resources are constraints … so one must make do with sub-optimal decision making and establish a cutoff point wherein the benefits outweigh the risks of looking for another alternative. That comes down to the realm of judgements. While George Stigler, a Nobel Laureate in Economics, introduce search optimization in fixed sequential search – a more concrete example has been illustrated in “Algorithms to Live By” by Christian & Griffiths. They suggested an holy grail response: 37% is the accurate answer. In other words, you would reach a suboptimal decision by ensuring that you have explored up to 37% of your estimated maximum effort. While the estimated maximum effort is quite ambiguous and afflicted with all of the elements of bias (cognitive and statistical), the best thinking is to be as honest as possible to assess that effort and then draw your search threshold cutoff.

An important element of leadership is about making calls. Good calls, not necessarily the best calls! Calls weighing all possible circumstances that one can, being aware of the biases, bringing in a diverse set of knowledge and opinions, falling back upon agnostic tools in statistics, and knowing when it is appropriate to have learnt enough to pull the trigger. And it is important to cascade the principles of decision making and the underlying complexity into and across the organization.

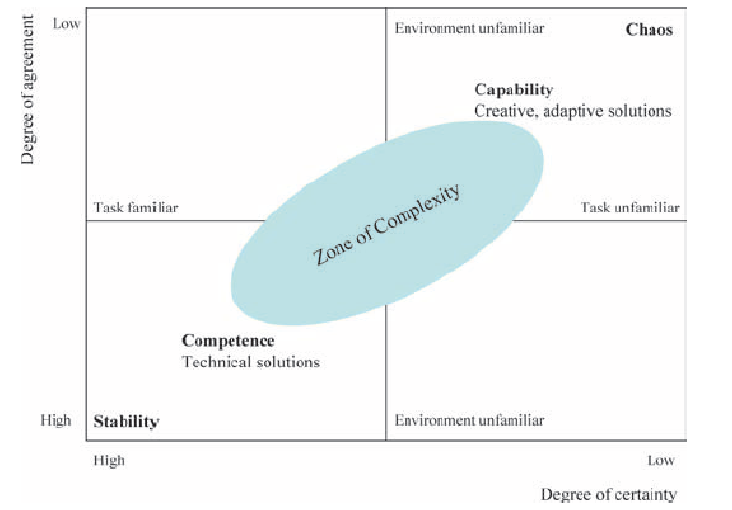

Chaos as a system: New Framework

Chaos is not an unordered phenomenon. There is a certain homeostatic mechanism at play that forces a system that might have inherent characteristics of a “chaotic” process to converge to some sort of stability with respect to predictability and parallelism. Our understanding of order which is deemed to be opposite of chaos is the fact that there is a shared consensus that the system will behave in an expected manner. Hence, we often allude to systems as being “balanced” or “stable” or “in order” to spotlight these systems. However, it is also becoming common knowledge in the science of chaos that slight changes in initial conditions in a system can emit variability in the final output that might not be predictable. So how does one straddle order and chaos in an observed system, and what implications does this process have on ongoing study of such systems?

Chaotic systems can be considered to have a highly complex order. It might require the tools of pure mathematics and extreme computational power to understand such systems. These tools have invariably provided some insights into chaotic systems by visually representing outputs as re-occurrences of a distribution of outputs related to a given set of inputs. Another interesting tie up in this model is the existence of entropy, that variable that taxes a system and diminishes the impact on expected outputs. Any system acts like a living organism: it requires oodles of resources to survive and a well-established set of rules to govern its internal mechanism driving the vector of its movement. Suddenly, what emerges is the fact that chaotic systems display some order while subject to an inherent mechanism that softens its impact over time. Most approaches to studying complex and chaotic systems involve understanding graphical plots of fractal nature, and bifurcation diagrams. These models illustrate very complex re occurrences of outputs directly related to inputs. Hence, complex order occurs from chaotic systems.

A case in point would be the relation of a population parameter in the context to its immediate environment. It is argued that a population in an environment will maintain a certain number and there would be some external forces that will actively work to ensure that the population will maintain at that standard number. It is a very Malthusian analytic, but what is interesting is that there could be some new and meaningful influences on the number that might increase the scale. In our current meaning, a change in technology or ingenuity could significantly alter the natural homeostatic number. The fact remains that forces are always at work on a system. Some systems are autonomic – it self-organizes and corrects itself toward some stable convergence. Other systems are not autonomic and once can only resort to the laws of probability to get some insight into the possible outputs – but never to a point where there is a certainty in predictive prowess.

Organizations have a lot of interacting variables at play at any given moment. In order to influence the organization behavior or/and direction, policies might be formulated to bring about the desirable results. However, these nudges toward setting off the organization in the right direction might also lead to unexpected results. The aim is to foresee some of these unexpected results and mollify the adverse consequences while, in parallel, encourage the system to maximize the benefits. So how does one effect such changes?

It all starts with building out an operating framework. There needs to be a clarity around goals and what the ultimate purpose of the system is. Thus there are few objectives that bind the framework.

- Clarity around goals and the timing around achieving these goals. If there is no established time parameter, then the system might jump across various states over time and it would be difficult to establish an outcome.

- Evaluate all of the internal and external factors that might operate in the framework that would impact the success of organizational mandates and direction. Identify stasis or potential for stasis early since that mental model could stem the progress toward a desirable impact.

- Apply toll gates strategically to evaluate if the system is proceeding along the lines of expectation, and any early aberrations are evaluated and the rules are tweaked to get the system to track on a desirable trajectory.

- Develop islands of learning across the path and engage the right talent and other parameters to force adaptive learning and therefore a more autonomic direction to the system.

- Bind the agents and actors in the organization to a shared sense of purpose within the parameter of time.

- Introduce diversity into the framework early in the process. The engagement of diversity allows the system to modulate around a harmonic mean.

- Finally, maintain a well document knowledge base such that the accretive learning that results due to changes in the organization become springboard for new initiatives that reduces the costs of potential failures or latency in execution.

- Encouraging the leadership to ensure that the vector is pointed toward the right direction at any given time.

Once a framework and the engagement rules are drawn out, it is necessary to rely on the natural velocity and self-organization of purposeful agents to move the agenda forward, hopefully with little or no intervention. A mechanism of feedback loops along the way would guide the efficacy of the direction of the system. The implications is that the strategy and the operations must be aligned and reevaluated and positive behavior is encouraged to ensure that the systems meets its objective.

However, as noted above, entropy is a dynamic that often threatens to derail the system objective. There will be external or internal forces constantly at work to undermine system velocity. The operating framework needs to anticipate that real possibility and pre-empt that with rules or introduction of specific capital to dematerialize these occurrences. Stasis is an active agent that can work against the system dynamic. Stasis is the inclination of agents or behaviors that anchors the system to some status quo – we have to be mindful that change might not be embraced and if there are resistors to that change, the dynamic of organizational change can be invariably impacted. It will take a lot more to get something done than otherwise needed. Identifying stasis and agents of stasis is a foundational element

While the above is one example of how to manage organizations in the shadows of the properties of how chaotic systems behave, another example would be the formulation of strategy of the organization in responses to external forces. How do we apply our learnings in chaos to deal with the challenges of competitive markets by aligning the internal organization to external factors? One of the key insights that chaos surfaces is that it is nigh impossible for one to fully anticipate all of the external variables, and leaving the system to dynamically adapt organically to external dynamics would allow the organization to thrive. To thrive in this environment is to provide the organization to rapidly change outside of the traditional hierarchical expectations: when organizations are unable to make those rapid changes or make strategic bets in response to the external systems, then the execution value of the organization diminishes.

Margaret Wheatley in her book Leadership and the New Science: Discovering Order in a Chaotic World Revised says, “Organizations lack this kind of faith, faith that they can accomplish their purposes in various ways and that they do best when they focus on direction and vision, letting transient forms emerge and disappear. We seem fixated on structures…and organizations, or we who create them, survive only because we build crafty and smart—smart enough to defend ourselves from the natural forces of destruction. Karl Weick, an organizational theorist, believes that “business strategies should be “just in time…supported by more investment in general knowledge, a large skill repertoire, the ability to do a quick study, trust in intuitions, and sophistication in cutting losses.”

We can expand the notion of a chaos in a system to embrace the bigger challenges associated with environment, globalization, and the advent of disruptive technologies.

One of the key challenges to globalization is how policy makers would balance that out against potential social disintegration. As policies emerge to acknowledge the benefits and the necessity to integrate with a new and dynamic global order, the corresponding impact to local institutions can vary and might even lead to some deleterious impact on those institutions. Policies have to encourage flexibility in local institutional capability and that might mean increased investments in infrastructure, creating a diverse knowledge base, establishing rules that govern free but fair trading practices, and encouraging the mobility of capital across borders. The grand challenges of globalization is weighed upon by government and private entities that scurry to create that continual balance to ensure that the local systems survive and flourish within the context of the larger framework. The boundaries of the system are larger and incorporates many more agents which effectively leads to the real possibility of systems that are difficult to be controlled via a hierarchical or centralized body politic Decision making is thus pushed out to the agents and actors but these work under a larger set of rules. Rigidity in rules and governance can amplify failures in this process.

Related to the realities of globalization is the advent of the growth in exponential technologies. Technologies with extreme computational power is integrating and create robust communication networks within and outside of the system: the system herein could represent nation-states or companies or industrialization initiatives. Will the exponential technologies diffuse across larger scales quickly and will the corresponding increase in adoption of new technologies change the future of the human condition? There are fears that new technologies would displace large groups of economic participants who are not immediately equipped to incorporate and feed those technologies into the future: that might be on account of disparity in education and wealth, institutional policies, and the availability of opportunities. Since technologies are exponential, we get a performance curve that is difficult for us to understand. In general, we tend to think linearly and this frailty in our thinking removes us from the path to the future sooner than later. What makes this difficult is that the exponential impact is occurring across various sciences and no one body can effectively fathom the impact and the direction. Bill Gates says it well “We always overestimate the change that will occur in the next two years and underestimate the change that will occur in the next ten. Don’t let yourself be lulled into inaction.” Does chaos theory and complexity science arm us with a differentiated tool set than the traditional toolset of strategy roadmaps and product maps? If society is being carried by the intractable and power of the exponent in advances in technology, than a linear map might not serve to provide the right framework to develop strategies for success in the long-term. Rather, a more collaborative and transparent roadmap to encourage the integration of thoughts and models among the actors who are adapting and adjusting dynamically by the sheer force of will would perhaps be an alternative and practical approach in the new era.

Lately there has been a lot of discussion around climate change. It has been argued, with good reason and empirical evidence, that environment can be adversely impacted on account of mass industrialization, increase in population, resource availability issues, the inability of the market system to incorporate the cost of spillover effects, the adverse impact of moral hazard and the theory of the commons, etc. While there are demurrers who contest the long-term climate change issues, the train seems to have already left the station! The facts do clearly reflect that the climate will be impacted. Skeptics might argue that science has not yet developed a precise predictive model of the weather system two weeks out, and it is foolhardy to conclude a dystopian future on climate fifty years out. However, the alternative argument is that our inability to exercise to explain the near-term effects of weather changes and turbulence does not negate the existence of climate change due to the accretion of greenhouse impact. Boiling a pot of water will not necessarily gives us an understanding of all of the convection currents involved among the water molecules, but it certainly does not shy away from the fact that the water will heat up.

History of Chaos

| Chaos is inherent in all compounded things. Strive on with diligence! –Buddha |

Scientific theories are characterized by the fact that they are open to refutation. To create a scientific model, there are three successive steps that one follows: observe the phenomenon, translate that into equations, and then solve the equations.

One of the early philosophers of science, Karl Popper (1902-1994) discussed this at great length in his book – The Logic of Scientific Discovery. He distinguishes scientific theories from metaphysical or mythological assertions. His main theses is that a scientific theory must be open to falsification: it has to be reproducible separately and yet one can gather data points that might refute the fundamental elements of theory. Developing a scientific theory in a manner that can be falsified by observations would result in new and more stable theories over time. Theories can be rejected in favor of a rival theory or a calibration of the theory in keeping with the new set of observations and outcomes that the theories posit. Until Popper’s time and even after, social sciences have tried to work on a framework that would allow the construction of models that would formulate some predictive laws that govern social dynamics. In his book, Poverty of Historicism, Popper maintained that such an endeavor is not fruitful since it does not take into consideration the myriad of minor elements that interact closely with one another in a meaningful way. Hence, he has touched indirectly on the concept of chaos and complexity and how it touches the scientific method. We will now journey into the past and through the present to understand the genesis of the theory and how it has been channelized by leading scientists and philosophers to decipher a framework for study society and nature.

As we have already discussed, one of the main pillars of Science is determinism: the probability of prediction. It holds that every event is determined by natural laws. Nothing can happen without an unbroken chain of causes that can be traced all the way back to an initial condition. The deterministic nature of science goes all the way back to Aristotelian times. Interestingly, Aristotle argued that there is some degree of indeterminism and he relegated this to chance or accidents. Chance is a character that makes its presence felt in every plot in the human and natural condition. Aristotle wrote that “we do not have knowledge of a thing until we have grasped its why, that is to say, its cause.” He goes on to illustrate his idea in greater detail – namely, that the final outcome that we see in a system is on account of four kinds of influencers: Matter, Form, Agent and Purpose.

Matter is what constitutes the outcome. For a chair it might be wood. For a statue, it might be marble. The outcome is determined by what constitutes the outcome.

Form refers to the shape of the outcome. Thus, a carpenter or a sculptor would have a pre-conceived notion of the shape of the outcome and they would design toward that artifact.

Agent refers to the efficient cause or the act of producing the outcome. Carpentry or masonry skills would be important to shape the final outcome.

Finally, the outcome itself must serve a purpose on its own. For a chair, it might be something to sit on, for a statue it might be something to be marveled at.

However, Aristotle also admits that luck and chance can play an important role that do not fit the causal framework in its own right. Some things do happen by chance or luck. Chance is a rare event, it is a random event and it is typically brought out by some purposeful action or by nature.

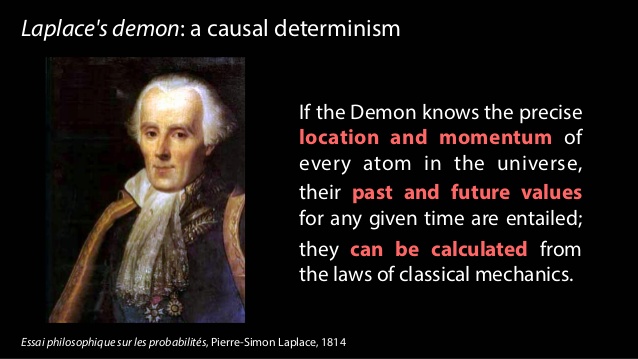

We had briefly discussed the Laplace demon and he summarized this wonderfully: “We ought then to consider the resent state of the universe as the effect of its previous state and as the cause of that which is to follow. An intelligence that, at a given instant, could comprehend all the forces by which nature is animated and the respective situation of the beings that make it up if moreover it were vast enough to submit these data to analysis, would encompass in the same formula the movements of the greatest bodies of the universe and those of the lightest atoms. For such an intelligence nothing would be uncertain, and the future, like the past, would be open to its eyes.” He thus admits to the fact that we lack the vast intelligence and we are forced to use probabilities in order to get a sense of understanding of dynamical systems.

It was Maxwell in his pivotal book “Matter and Motion” published in 1876 lay the groundwork of chaos theory.

“There is a maxim which is often quoted, that “the same causes will always produce the same effects.’ To make this maxim intelligible we must define what we mean by the same causes and the same effects, since it is manifest that no event ever happens more than once, so that the causes and effects cannot be the same in all respects. There is another maxim which must not be confounded with that quoted at the beginning of this article, which asserts “That like causes produce like effects.” This is only true when small variations in the initial circumstances produce only small variations in the final state of the system. In a great many physical phenomena this condition is satisfied: but there are other cases in which a small initial variation may produce a great change in the final state of the system, as when the displacement of the points cause a railway train to run into another instead of keeping its proper course.” What is interesting however in the above quote is that Maxwell seems to go with the notion that in a great many cases there is no sensitivity to initial conditions.

In the 1890’s Henri Poincare was the first exponent of chaos theory. He says “it may happen that small differences in the initial conditions produce very great ones in the final phenomena. A small error in the former will produce an enormous error in the latter. Prediction becomes impossible.” This was a far cry from the Newtonian world which sought order on how the solar system worked. Newton’s model was posted on the basis of the interaction between just two bodies. What would then happen if three bodies or N bodies were introduced into the model. This led to the rise of the Three Body Problem which led to Poincare embracing the notion that this problem could not be solved and can be tackled by approximate numerical techniques. Solving this resulted in solutions that were so tangled that is was difficult to not only draw them, it was near impossible to derive equations to fit the results. In addition, Poincare also discovered that if the three bodies started from slightly different initial positions, the orbits would trace out different paths. This led to Poincare forever being designated as the Father of Chaos Theory since he laid the groundwork on the most important element in chaos theory which is the sensitivity to initial dependence.

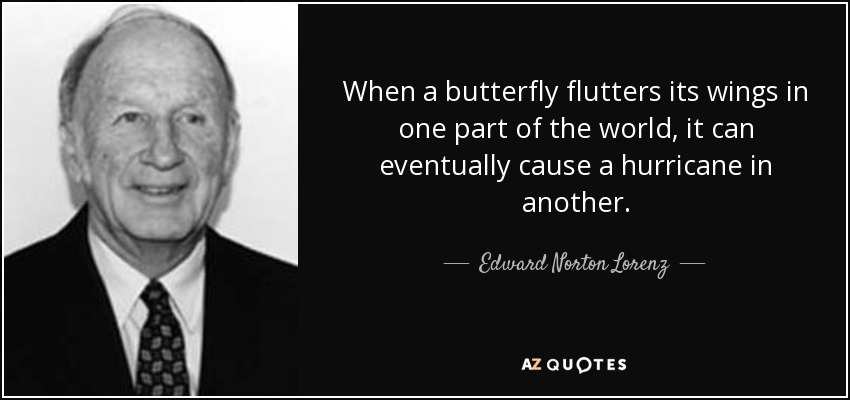

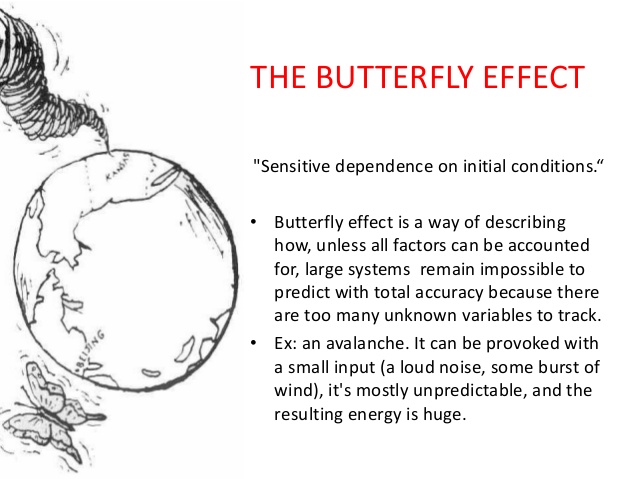

In the early 1960’s, the first true experimenter in chaos was a meteorologist named Edward Lorenz. He was working on a problem in weather prediction and he set up a system with twelve equations to model the weather. He set the initial conditions and the computer was left to predict what the weather might be. Upon revisiting this sequence later on, he inadvertently and by sheer accident, decided to run the sequence again in the middle and he noticed that the outcome was significantly different. The imminent question that followed was why the outcome was so different than the original. He traced this back to the initial condition wherein he noted that the initial input was different with respect to the decimal places. The system incorporated the all of the decimal places rather than the first three. (He had originally input the number .506 and he had concatenated the number from .506127). He would have expected that this thin variation in input would have created a sequence close to the original sequence but that was not to be: it was distinctly and hugely different. This effect became known as the Butterfly effect which is often substituted for Chaos Theory. Ian Stewart in his book, Does God Play Dice? The Mathematics of Chaos, describes this visually as follows:

“The flapping of a single butterfly’s wing today produces a tiny change in the state of the atmosphere. Over a period of time, what the atmosphere actually does diverges from what it would have done. So, in a month’s time, a tornado that would have devastated the Indonesian cost doesn’t happen. Or maybe one that wasn’t going to happen, does.”

Lorenz thus argued that it would be impossible to predict the weather accurately. However, he reduced his experiment to fewer set of equations and took upon observations of how small change in initial conditions affect predictability of smaller systems. He found a parallel – namely, that changes in initial conditions tends to render the final outcome of a system to be inaccurate. As he looked at alternative systems, he found a strange pattern that emerged – namely, that the system always represented a double spiral – the system never settled down to a single point but they never repeated its trajectory. It was a path breaking discovery that led to further advancement in the science of chaos in later years.

Years later, Robert May investigated how this impacts population. He established an equation that reflected a population growth and initialized the equation with a parameter for growth rate value. (The growth rate was initialized to 2.7). May found that as he increased the parameter value, the population grew which was expected. However, once he passed the 3.0 growth value, he noticed that equation would not settle down to a single population but branch out to two different values over time. If he raised the initial value more, the bifurcation or branching of the population would be twice as much or four different values. If he continued to increase the parameter, the lines continue to double until chaos appeared and it became hard to make point predictions.

There was another innate discovery that occurred through the experiment. When one visually looks at the bifurcation, one tends to see similarity between the small and large branches. This self-similarity became an important part of the development of chaos theory.

Benoit Mandelbrot started to study this self-similarity pattern in chaos. He was an economist and he applied mathematical equations to predict fluctuations in cotton prices. He noted that particular price changes were not predictable but there were certain patterns that were repeated and the degree of variation in prices had remained largely constant. This is suggestive of the fact that one might, upon preliminary reading of chaos, arrive at the notion that if weather cannot be predictable, then how can we predict climate many years out. On the contrary, Mandelbrot’s experiments seem to suggest that short time horizons are difficult to predict that long time horizon impact since systems tend to settle into some patterns that is reflecting of smaller patterns across periods. This led to the development of the concept of fractal dimensions, namely that sub-systems develop a symmetry to a larger system.

Feigenbaum was a scientist who became interested in how quickly bifurcations occur. He discovered that regardless of the scale of the system, the came at a constant rate of 4.669. If you reduce or enlarge the scale by that constant, you would see the mechanics at work which would lead to an equivalence in self-similarity. He applied this to a number of models and the same scaling constant took effect. Feigenbaum had established, for the first time, a universal constant around chaos theory. This was important because finding a constant in the realm of chaos theory was suggestive of the fact that chaos was an ordered process, not a random one.

Sir James Lighthill gave a lecture and in that he made an astute observation –

“We are all deeply conscious today that the enthusiasm of our forebears for the marvelous achievements of Newtonian mechanics led them to make generalizations in this area of predictability which, indeed, we may have generally tended to believe before 1960, but which we now recognize were false. We collectively wish to apologize for having misled the general educated public by spreading ideas about determinism of systems satisfying Newton’s laws of motion that, after 1960, were to be proved incorrect.”

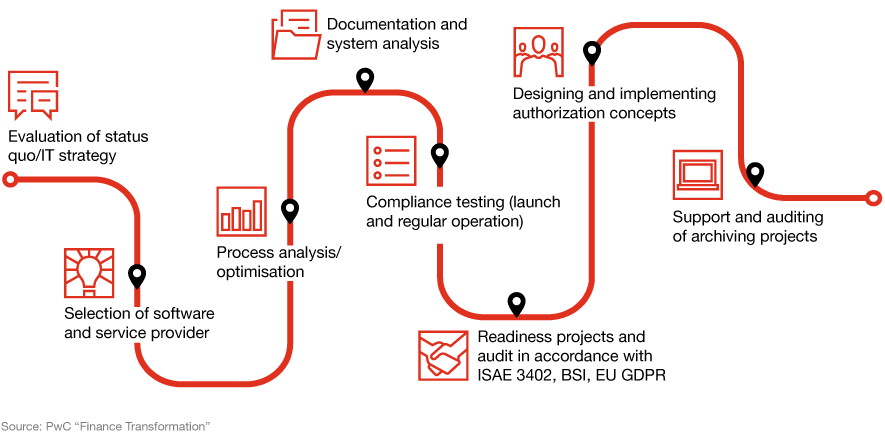

Building a Lean Financial Infrastructure!

A lean financial infrastructure presumes the ability of every element in the value chain to preserve and generate cash flow. That is the fundamental essence of the lean infrastructure that I espouse. So what are the key elements that constitute a lean financial infrastructure?

And given the elements, what are the key tweaks that one must continually make to ensure that the infrastructure does not fall into entropy and the gains that are made fall flat or decay over time. Identification of the blocks and monitoring and making rapid changes go hand in hand.

The Key Elements or the building blocks of a lean finance organization are as follows:

- Chart of Accounts: This is the critical unit that defines the starting point of the organization. It relays and groups all of the key economic activities of the organization into a larger body of elements like revenue, expenses, assets, liabilities and equity. Granularity of these activities might lead to a fairly extensive chart of account and require more work to manage and monitor these accounts, thus requiring incrementally a larger investment in terms of time and effort. However, the benefits of granularity far exceeds the costs because it forces management to look at every element of the business.

- The Operational Budget: Every year, organizations formulate the operational budget. That is generally a bottoms up rollup at a granular level that would map to the Chart of Accounts. It might follow a top-down directive around what the organization wants to land with respect to income, expense, balance sheet ratios, et al. Hence, there is almost always a process of iteration in this step to finally arrive and lock down the Budget. Be mindful though that there are feeders into the budget that might relate to customers, sales, operational metrics targets, etc. which are part of building a robust operational budget.

- The Deep Dive into Variances: As you progress through the year and part of the monthly closing process, one would inquire about how the actual performance is tracking against the budget. Since the budget has been done at a granular level and mapped exactly to the Chart of Accounts, it thus becomes easier to understand and delve into the variances. Be mindful that every element of the Chart of Account must be evaluated. The general inclination is to focus on the large items or large variances, while skipping the small expenses and smaller variances. That method, while efficient, might not be effective in the long run to build a lean finance organization. The rule, in my opinion, is that every account has to be looked and the question should be – Why? If the management has agreed on a number in the budget, then why are the actuals trending differently. Could it have been the budget and that we missed something critical in that process? Or has there been a change in the underlying economics of the business or a change in activities that might be leading to these “unexpected variances”. One has to take a scalpel to both – favorable and unfavorable variances since one can learn a lot about the underlying drivers. It might lead to managerially doing more of the better and less of the worse. Furthermore, this is also a great way to monitor leaks in the organization. Leaks are instances of cash that are dropping out of the system. Much of little leaks amounts to a lot of cash in total, in some instances. So do not disregard the leaks. Not only will that preserve the cash but once you understand the leaks better, the organization will step up in efficiency and effectiveness with respect to cash preservation and delivery of value.

- Tweak the process: You will find that as you deep dive into the variances, you might want to tweak certain processes so these variances are minimized. This would generally be true for adverse variances against the budget. Seek to understand why the variance, and then understand all of the processes that occur in the background to generate activity in the account. Once you fully understand the process, then it is a matter of tweaking this to marginally or structurally change some key areas that might favorable resonate across the financials in the future.

- The Technology Play: Finally, evaluate the possibilities of exploring technology to surface issues early, automate repetitive processes, trigger alerts early on to mitigate any issues later, and provide on-demand analytics. Use technology to relieve time and assist and enable more thinking around how to improve the internal handoffs to further economic value in the organization.

All of the above relate to managing the finance and accounting organization well within its own domain. However, there is a bigger step that comes into play once one has established the blocks and that relates to corporate strategy and linking it to the continual evolution of the financial infrastructure.

The essential question that the lean finance organization has to answer is – What can the organization do so that we address every element that preserves and enhances value to the customer, and how do we eliminate all non-value added activities? This is largely a process question but it forces one to understand the key processes and identify what percentage of each process is value added to the customer vs. non-value added. This can be represented by time or cost dimension. The goal is to yield as much value added activities as possible since the underlying presumption of such activity will lead to preservation of cash and also increase cash acquisition activities from the customer.

Aaron Swartz took down a piece of the Berlin Wall! We have to take it all down!

“The world’s entire scientific … heritage … is increasingly being digitized and locked up by a handful of private corporations… The Open Access Movement has fought valiantly to ensure that scientists do not sign their copyrights away but instead ensure their work is published on the Internet, under terms that allow anyone to access it.” – Aaron Swartz

Information, in the context of scholarly articles by research at universities and think-tanks, is not a zero sum game. In other words, one person cannot have more without having someone have less. When you start creating “Berlin” walls in the information arena within the halls of learning, then learning itself is compromised. In fact, contributing or granting the intellectual estate into the creative commons serves a higher purpose in society – an access to information and hence, a feedback mechanism that ultimately enhances the value to the end-product itself. How? Since now the product has been distributed across a broader and diverse audience, and it is open to further critical analyses.

The universities have built a racket. They have deployed a Chinese wall between learning in a cloistered environment and the world who are not immediate participants. The Guardian wrote an interesting article on this matter and a very apt quote puts it all together.

“Academics not only provide the raw material, but also do the graft of the editing. What’s more, they typically do so without extra pay or even recognition – thanks to blind peer review. The publishers then bill the universities, to the tune of 10% of their block grants, for the privilege of accessing the fruits of their researchers’ toil. The individual academic is denied any hope of reaching an audience beyond university walls, and can even be barred from looking over their own published paper if their university does not stump up for the particular subscription in question.

This extraordinary racket is, at root, about the bewitching power of high-brow brands. Journals that published great research in the past are assumed to publish it still, and – to an extent – this expectation fulfils itself. To climb the career ladder academics must get into big-name publications, where their work will get cited more and be deemed to have more value in the philistine research evaluations which determine the flow of public funds. Thus they keep submitting to these pricey but mightily glorified magazines, and the system rolls on.”

http://www.guardian.co.uk/commentisfree/2012/apr/11/academic-journals-access-wellcome-trust

JSTOR is a not-for-profit organization that has invested heavily in providing an online system for archiving, accessing, and searching digitized copies of over 1,000 academic journals. More recently, I noticed some effort on their part to allow public access to only 3 articles over a period of 21 days. This stinks! This policy reflects an intellectual snobbery beyond Himalayan proportions. The only folks that have access to these academic journals and studies are professors, and researchers that are affiliated with a university and university libraries. Aaron Swartz noted the injustice of hoarding such knowledge and tried to distribute a significant proportion of JSTOR’s archive through one or more file-sharing sites. And what happened thereafter was perhaps one of the biggest misapplication of justice. The same justice that disallows asymmetry of information in Wall Street is being deployed to preserve the asymmetry of information at the halls of learning.

MSNBC contributor Chris Hayes criticized the prosecutors, saying “at the time of his death Aaron was being prosecuted by the federal government and threatened with up to 35 years in prison and $1 million in fines for the crime of—and I’m not exaggerating here—downloading too many free articles from the online database of scholarly work JSTOR.”

The Associated Press reported that Swartz’s case “highlights society’s uncertain, evolving view of how to treat people who break into computer systems and share data not to enrich themselves, but to make it available to others.”

Chris Soghioian, a technologist and policy analyst with the ACLU, said, “Existing laws don’t recognize the distinction between two types of computer crimes: malicious crimes committed for profit, such as the large-scale theft of bank data or corporate secrets; and cases where hackers break into systems to prove their skillfulness or spread information that they think should be available to the public.”

Kelly Caine, a professor at Clemson University who studies people’s attitudes toward technology and privacy, said Swartz “was doing this not to hurt anybody, not for personal gain, but because he believed that information should be free and open, and he felt it would help a lot of people.”

And then there were some modest reservations, and Swartz actions were attributed to reckless judgment. I contend that this does injustice to someone of Swartz’s commitment and intellect … the recklessness was his inability to grasp the notion that an imbecile in the system would pursue 35 years of imprisonment and $1M fine … it was not that he was not aware of what he was doing but he believed, as does many, that scholarly academic research should be available as a free for all.

We have a Berlin wall that needs to be taken down. Swartz started that but he was unable to keep at it. It is important to not rest in this endeavor and that everyone ought to actively petition their local congressman to push bills that will allow open access to these academic articles.

John Maynard Keynes had warned of the folly of “shutting off the sun and the stars because they do not pay a dividend”, because what is at stake here is the reach of the light of learning. Aaron was at the vanguard leading that movement, and we should persevere to become those points of light that will enable JSTOR to disseminate the information that they guard so unreservedly.

LinkedIn Endorsements: A Failure or a Brilliant Strategy?

LinkedIn endorsements have no value. So says many pundits! Here are some interesting articles that speaks of the uselessness of this product feature in LinkedIn.

http://www.businessinsider.com/linkedin-drops-endorsements-by-year-end-2013-3

http://mashable.com/2013/01/03/linkedins-endorsements-meaningless/

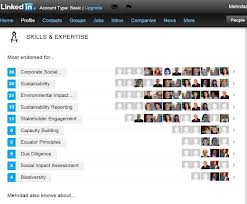

I have some opinions on this matter. I started a company last year that allows people within and outside of the company to recommend professionals based on projects. We have been ushered into a world where our jobs, for the most part, constitute a series of projects that are undertaken over the course of a person’s career. The recognition system around this granular element is lacking; we have recommendations and recognition systems that have been popularized by LinkedIn, Kudos, Rypple, etc. But we have not seen much development in tools that address recognition around projects in the public domain. I foresee the possibility of LinkedIn getting into this space soon. Why? It is simple. The answer is in their “useless” Endorsement feature that has been on since late last year. As of March 13, one billion endorsements have been given to 56 million LinkedIn members, an average of about 4 per person. What does this mean? It means that LinkedIn has just validated a potential feature which will add more flavor to the endorsements – Why have you granted these endorsements in the first place?

Thus, it stands to reason the natural step is to reach out to these endorsers by providing them appropriate templates to add more flavor to the endorsements. Doing so will force a small community of the 56 million participants to add some flavor. Even if that constitutes 10%, that is almost 5.6M members who are contributing to this feature. Now how many products do you know that release one feature and very quickly gather close to six million active participants to use it? In addition, this would only gain force since more and more people would use this feature and all of a sudden … the endorsements become a beachhead into a very strategic product.

The other area that LinkedIn will probably step into is to catch the users young. Today it happens to be professionals; I will not be surprised if they start moving into the university/college space and what is a more effective way to bridge than to position a product that recognizes individuals against projects the individuals have collaborated on.

LinkedIn and Facebook are two of the great companies of our time and they are peopled with incredibly smart people. So what may seemingly appear as a great failure in fact will become the enabler of a successful product that will significantly increase the revenue streams of LinkedIn in the long run!

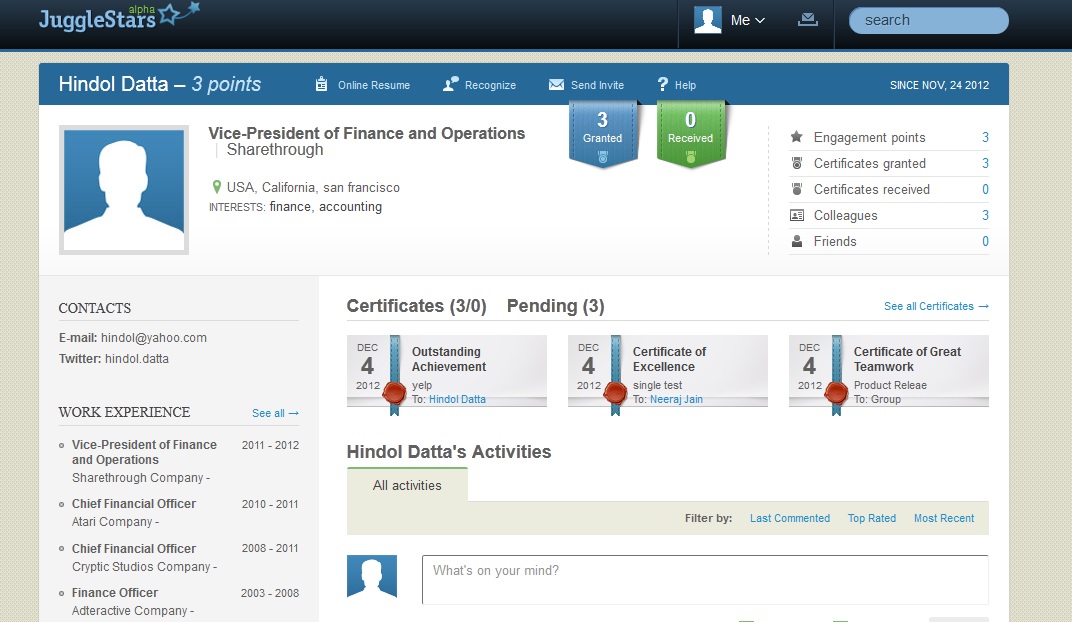

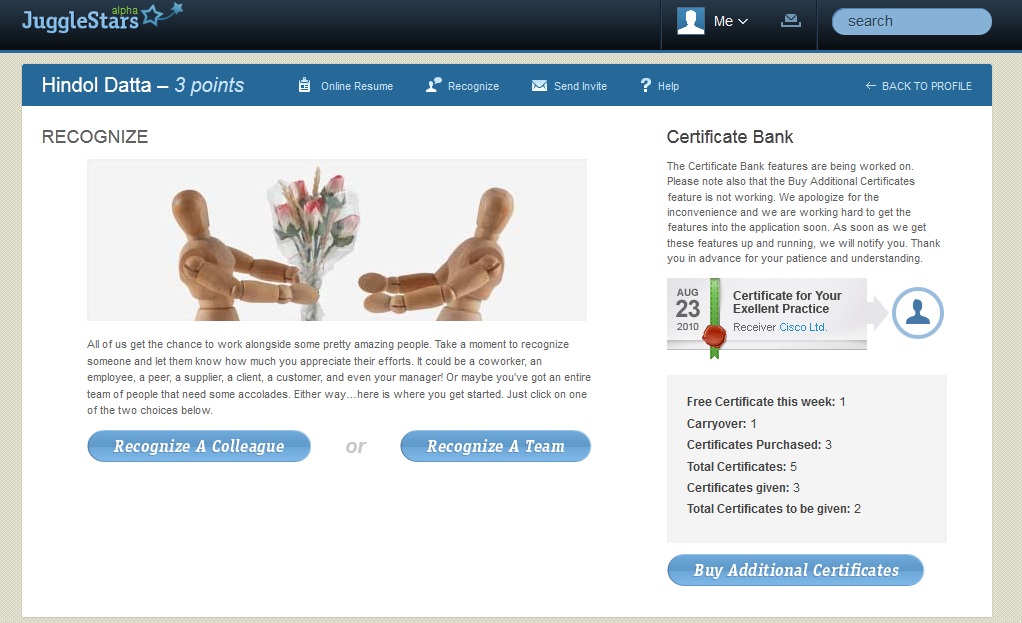

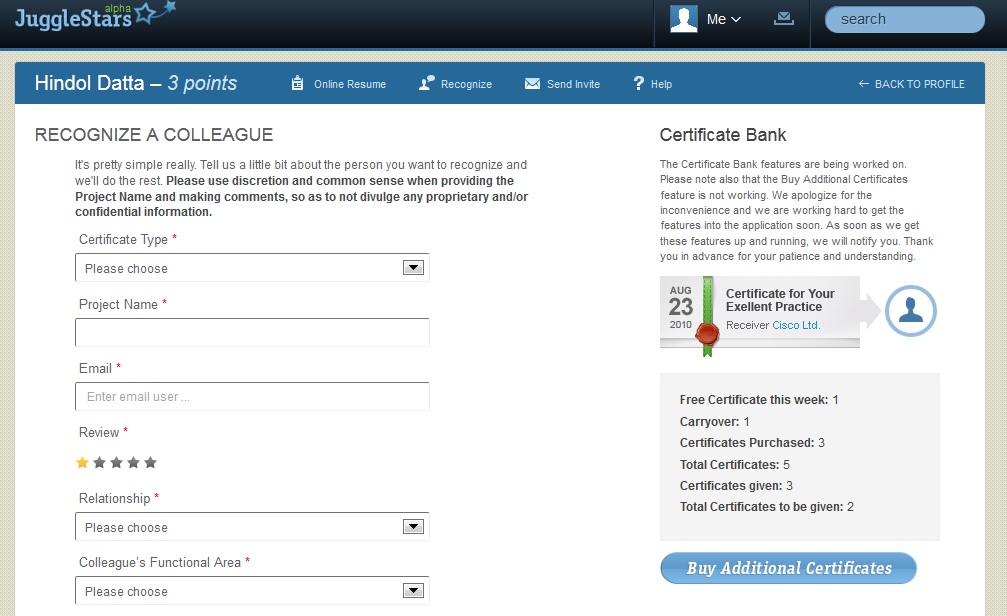

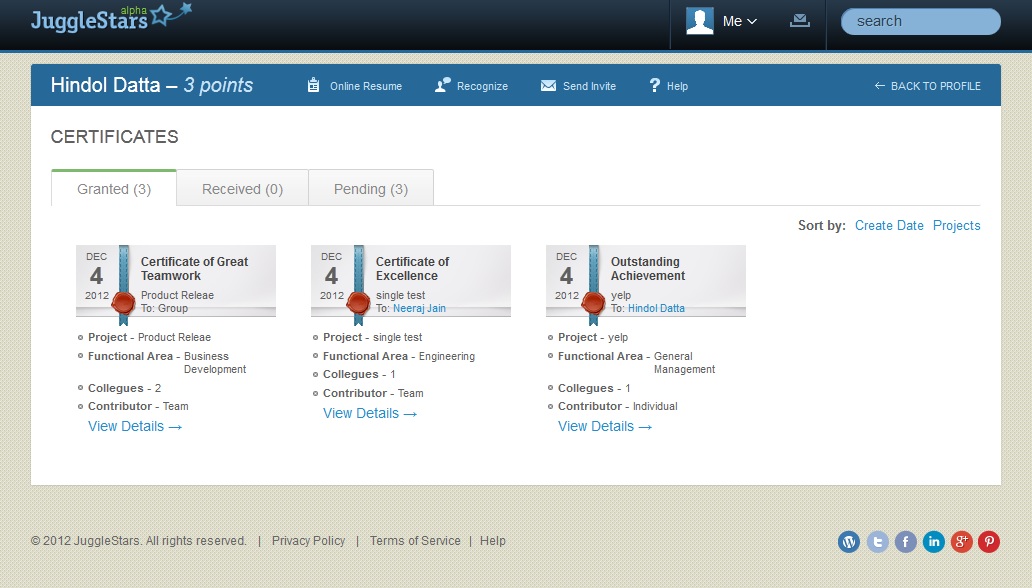

Why Jugglestars? How will this benefit you?

Consider this. Your professional career is a series of projects. Employers look for accountability and performance, and they measure you by how you fare on your projects. Everything else, for the most part, is white noise. The projects you work on establish your skill set and before long – your career trajectory. However, all the great stuff that you have done at work is for the most part hidden from other people in your company or your professional colleagues. You may get a recommendation on LinkedIn, which is fairly high-level, or you may receive endorsements for your skills, which is awesome. But the Endorsements on LinkedIn seem a little random, don’t they? Wouldn’t it be just awesome to recognize, or be recognized by, your colleagues for projects that you have worked on. We are sure that there are projects that you have worked on that involves third-party vendors, consultants, service providers, clients, etc. – well, now you have a forum to send and receive recognition, in a beautiful form factor, that you can choose to display across your networks.

Imagine an employee review. You must have spent some time thinking through all the great stuff that you have done that you want to attach to your review form. And you may have, in your haste, forgotten some of the great stuff that you have done and been recognized for informally. So how cool would it be to print or email all the projects that you’ve worked on and the recognition you’ve received to your manager? How cool would it be to send all the people that you have recognized for their phenomenal work? For in the act of participating in the recognition ecosystem that our application provides you – you are an engaged and prized employee that any company would want to retain, nurture and develop.

Now imagine you are looking for a job. You have a resume. That is nice. And then the potential employer or recruiter is redirected to your professional networks and they have a glimpse of your recommendations and skill sets. That is nice too! But seriously…wouldn’t it be better for the hiring manager or recruiter to have a deeper insight into some of the projects that you have done and the recognition that you have received? Wouldn’t it be nice for them to see how active you are in recognizing great work of your other colleagues and project co-workers? Now they would have a more comprehensive idea of who you are and what makes you tick.

We help you build your professional brand and convey your accomplishments. That translates into greater internal development opportunities in your company, promotion, increase in pay, and it also makes you more marketable. We help you connect to high-achievers and forever manage your digital portfolio of achievements that can, at your request, exist in an open environment. JuggleStars.com is a great career management tool.

Check out www.jugglestars.com

.

JuggleStars launched! Great Application for Employee Recognition.

About JuggleStars www.jugglestars.com

Please support Jugglestars. This is an Alpha Release. Use the application in your organization. The Jugglestars team will be adding in more features over the next few months. Give them your feedback. They are an awesome team with great ideas. Please click on www.jugglestars.com and you can open an account, go to Account Settings and setup your profile and then you are pretty much ready to go to recognize your team and your colleagues at a project level.