Category Archives: startup

Network Theory and Network Effects

Complexity theory needs to be coupled with network theory to get a more comprehensive grasp of the underlying paradigms that govern the outcomes and morphology of emergent systems. In order for us to understand the concept of network effects which is commonly used to understand platform economics or ecosystem value due to positive network externalities, we would like to take a few steps back and appreciate the fundamental theory of networks. This understanding will not only help us to understand complexity and its emergent properties at a low level but also inform us of the impact of this knowledge on how network effects can be shaped to impact outcomes in an intentional manner.

There are first-order conditions that must be met to gauge whether the subject of the observation is a network. Firstly, networks are all about connectivity within and between systems. Understanding the components that bind the system would be helpful. However, do keep in mind that complexity systems (CPS and CAS) might have emergent properties due to the association and connectivity of the network that might not be fully explained by network theory. All the same, understanding networking theory is a building block to understanding emergent systems and the outcome of its structure on addressing niche and macro challenges in society.

Networks operates spatially in a different space and that has been intentionally done to allow some simplification and subsequent generalization of principles. The geometry of network is called network topology. It is a 2D perspective of connectivity.

Networks are subject to constraints (physical resources, governance constraint, temporal constraints, channel capacity, absorption and diffusion of information, distribution constraint) that might be internal (originated by the system) or external (originated in the environment that the network operates in).

Finally, there is an inherent non-linearity impact in networks. As nodes increase linearly, connections will increase exponentially but might be subject to constraints. The constraints might define how the network structure might morph and how information and signals might be processed differently.

Graph theory is the most widely used tool to study networks. It consists of four parts: vertices which represent an element in the network, edges refer to relationship between nodes which we call links, directionality which refers to how the information is passed ( is it random and bi-directional or follows specific rules and unidirectional), channels that refer to bandwidth that carry information, and finally the boundary which establishes specificity around network operations. A graph can be weighted – namely, a number can be assigned to each length to reflect the degree of interaction or the strength of resources or the proximity of the nodes or the ordering of discernible clusters.

The central concept of network theory thus revolves around connectivity between nodes and how non-linear emergence occurs. A node can have multiple connections with other node/nodes and we can weight the node accordingly. In addition, the purpose of networks is to pass information in the most efficient manner possible which relays into the concept of a geodesic which is either the shortest path between two nodes that must work together to achieve a purpose or the least number of leaps through links that information must negotiate between the nodes in the network.

Technically, you look for the longest path in the network and that constitutes the diameter while you calculate the average path length by examining the shortest path between nodes, adding all of those paths up and then dividing by the number of pairs. Significance of understanding the geodesic allows an understanding of the size of the network and throughput power that the network is capable of.

Nodes are the atomic elements in the network. It is presumed that its degree of significance is related to greater number of connections. There are other factors that are important considerations: how adjacent or close are the nodes to one another, does some nodes have authority or remarkable influence on others, are nodes positioned to be a connector between other nodes, and how capable are the nodes in absorbing, processing and diffusing the information across the links or channels. How difficult is it for the agents or nodes in the network to make connections? It is presumed that if the density of the network is increased, then we create a propensity in the overall network system to increase the potential for increased connectivity.

As discussed previously, our understanding of the network is deeper once we understand the elements well. The structure or network topology is represented by the graph and then we must understand size of network and the patterns that are manifested in the visual depiction of the network. Patterns, for our purposes, might refer to clusters of nodes that are tribal or share geographical proximity that self-organize and thus influence the structure of the network. We will introduce a new term homophily where agents connect with those like themselves. This attribute presumably allows less resources needed to process information and diffuse outcomes within the cluster. Most networks have a cluster bias: in other words, there are areas where there is increased activity or increased homogeneity in attributes or some form of metric that enshrines a group of agents under one specific set of values or activities. Understanding the distribution of cluster and the cluster bias makes it easier to influence how to propagate or even dismantle the network. This leads to an interesting question: Can a network that emerges spontaneously from the informal connectedness between agents be subjected to some high dominance coefficient – namely, could there be nodes or links that might exercise significant weight on the network?

The network has to align to its environment. The environment can place constraints on the network. In some instances, the agents have to figure out how to overcome or optimize their purpose in the context of the presence of the environmental constraints. There is literature that suggests the existence of random networks which might be an initial state, but it is widely agreed that these random networks self-organize around their purpose and their interaction with its environment. Network theory assigns a number to the degree of distribution which means that all or most nodes have an equivalent degree of connectivity and there is no skewed influence being weighed on the network by a node or a cluster. Low numbers assigned to the degree of distribution suggest a network that is very democratic versus high number that suggests centralization. To get a more practical sense, a mid-range number assigned to a network constitutes a decentralized network which has close affinities and not fully random. We have heard of the six degrees of separation and that linkage or affinity is most closely tied to a mid-number assignment to the network.

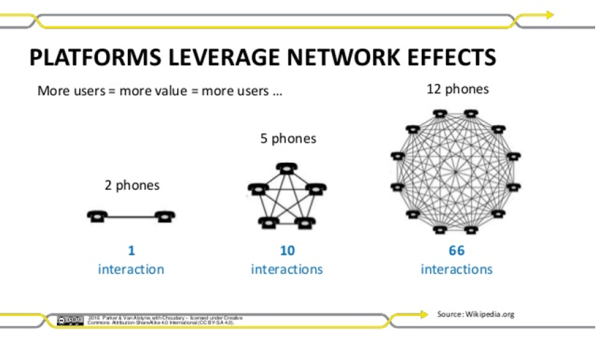

We are now getting into discussions on scale and binding this with network theory. Metcalfe’s law states that the value of a network grows as a square of the number of the nodes in the network. More people join the network, the more valuable the network. Essentially, there is a feedback loop that is created, and this feedback loop can kindle a network to grow exponentially. There are two other topics – Contagion and Resilience. Contagion refers to the ability of the agents to diffuse information. This information can grow the network or dismantle it. Resilience refers to how the network is organized to preserve its structure. As you can imagine, they have huge implications that we see. How do certain ideas proliferate over others, how does it cluster and create sub-networks which might grow to become large independent networks and how it creates natural defense mechanisms against self-immolation and destruction?

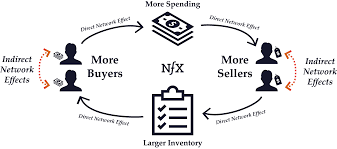

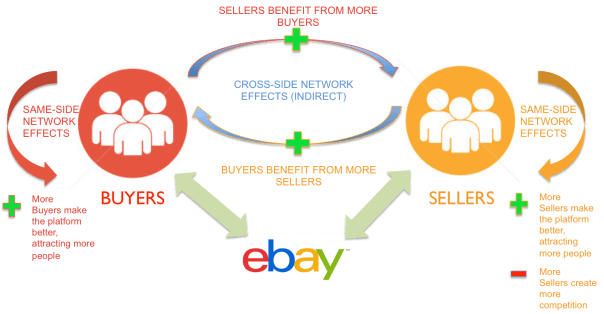

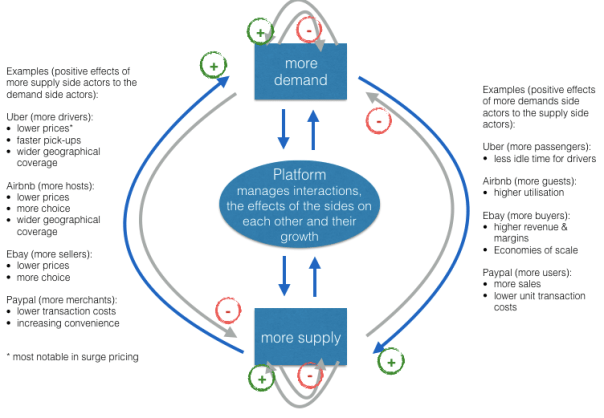

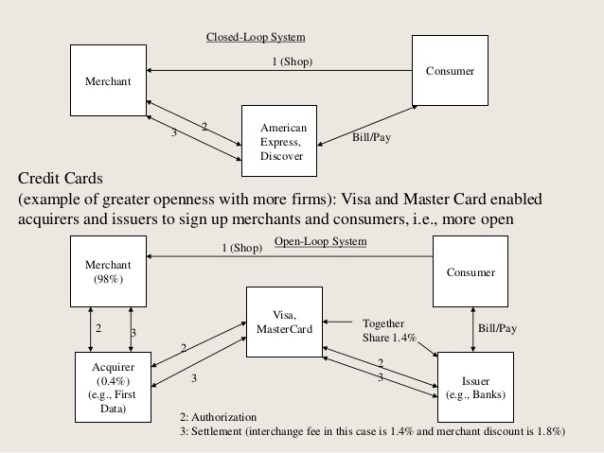

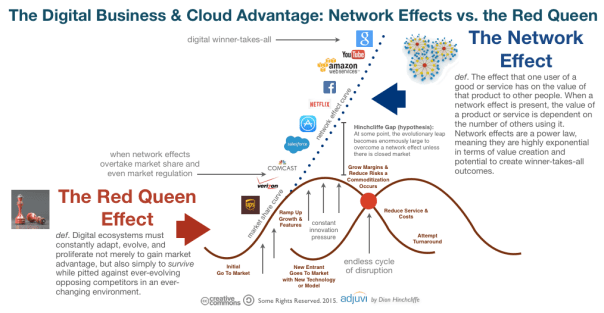

Network effect is commonly known as externalities in economics. It is an effect that is external to the transaction but influences the transaction. It is the incremental benefit gained by an existing user for each new user that joins the network. There are two types of network effects: Direct network effects and Indirect network effect. Direct network effects are same side effects. The value of a service goes up as the number of users goes up. For example, if more people have phones, it is useful for you to have a phone. The entire value proposition is one-sided. Indirect networks effects are multi-sided. It lends itself to our current thinking around platforms and why smart platforms can exponentially increase the network. The value of the service increases for one user group when a new user group joins the network. Take for example the relationship between credit card banks, merchants and consumers. There are three user groups, and each gather different value from the network of agents that have different roles. If more consumers use credit cards to buy, more merchants will sign up for the credit cards, and as more merchants sign up – more consumers will sign up with the bank to get more credit cards. This would be an example of a multi-sided platform that inherently has multi-sided network effects. The platform inherently gains significant power such that it becomes more valuable for participants in the system to join the network despite the incremental costs associated with joining the network. Platforms that are built upon effective multi-sided network effects grow quickly and are generally sustainable. Having said that, it could be just as easy that a few dominant bad actors in the network can dismantle and unravel the network completely. We often hear of the tipping point: namely, that once the platform reaches a critical mass of users, it would be difficult to dismantle it. That would certainly be true if the agents and services are, in the aggregate, distributed fairly across the network: but it is also possible that new networks creating even more multi-sided network effects could displace an entrenched network. Hence, it is critical that platform owners manage the quality of content and users and continue to look for more opportunities to introduce more user groups to entrench and yet exponentially grow the network.

Winner Take All Strategy

Being the first to cross the finish line makes you a winner in only one phase of life. It’s what you do after you cross the line that really counts.

– Ralph Boston

Does winner-take-all strategy apply outside the boundaries of a complex system? Let us put it another way. If one were to pursue a winner-take-all strategy, then does this willful strategic move not bind them to the constraints of complexity theory? Will the net gains accumulate at a pace over time far greater than the corresponding entropy that might be a by-product of such a strategy? Does natural selection exhibit a winner-take-all strategy over time and ought we then to regard that winning combination to spur our decisions around crafting such strategies? Are we fated in the long run to arrive at a world where there will be a very few winners in all niches and what would that mean? How does that surmise with our good intentions of creating equal opportunities and a fair distribution of access to resources to a wider swath of the population? In other words, is a winner take all a deterministic fact and does all our trivial actions to counter that constitute love’s labor lost?

Natural selection is a mechanism for evolution. It explains how populations or species evolve or modify over time in such a manner that it becomes better suited to their environments. Recall the discussion on managing scale in the earlier chapter where we discussed briefly about aligning internal complexity to external complexity. Natural selection is how it plays out at a biological level. Essentially natural selection posits that living organisms have inherited traits that help them to survive and procreate. These organisms will largely leave more offspring than their peers since the presumption is that these organisms will carry key traits that will survive the vagaries of external complexity and environment (predators, resource scarcity, climate change, etc.) Since these traits are passed on to the next generate, these traits will become more common until such time that the traits are dominant over generations, if the environment has not been punctuated with massive changes. These organisms with these dominant traits will have adapted to their environment. Natural selection does not necessarily suggest that what is good for one is good for the collective species.

An example that was shared by Robert Frank in his book “The Darwin Economy” was the case of large antlers of the bull elk. These antlers developed as an instrument for attracting mates rather than warding off predators. Big antlers would suggest a greater likelihood of the bull elk to marginalize the elks with smaller antlers. Over time, the bull elks with small antlers would die off since they would not be able to produce offspring and pass their traits. Thus, the bull elks would largely comprise of those elks with large antlers. However, the flip side is that large antlers compromise mobility and thus are more likely to be attacked by predators. Although the individual elk with large antler might succeed to stay around over time, it is also true that the compromised mobility associated with large antlers would overall hurt the propagation of the species as a collective group. We will return to this very important concept later. The interests of individual animals were often profoundly in conflict with the broader interests of their own species. Corresponding to the development of the natural selection mechanism is the introduction of the concept of the “survival of the fittest” which was introduced by Herbert Spencer. One often uses natural selection and survival of the fittest interchangeable and that is plain wrong. Natural selection never claims that the species that will emerge is the strongest, the fastest, the largest, etc.: it simply claims that the species will be the fittest, namely it will evolve in a manner best suited for the environment in which it resides. Put it another way: survival of the most sympathetic is perhaps more applicable. Organisms that are more sympathetic and caring and work in harmony with the exigencies of an environment that is largely outside of their control would likely succeed and thrive.

We will digress into the world of business. A common conception that is widely discussed is that businesses must position toward a winner-take-all strategy – especially, in industries that have very high entry costs. Once these businesses entrench themselves in the space, the next immediate initiative would be to literally launch a full-frontal assault involving huge investments to capture the mind and the wallet of the customer. Peter Thiel says – Competition is for losers. If you want to create and capture lasting value, look to build a monopoly.” Once that is built, it would be hard to displace!

Scaling the organization intentionally is key to long-term success. There are a number of factors that contribute toward developing scale and thus establishing a strong footing in the particular markets. We are listing some of the key factors below:

- Barriers to entry: Some organizations have natural cost prohibitive barriers to entry like utility companies or automobile plants. They require large investments. On the other hand, organizations can themselves influence and erect huge barriers to entry even though the barriers did not exist. Organizations would massively invest in infrastructure, distribution, customer acquisition and retention, brand and public relations. Organizations that are able to rapidly do this at a massive scale would be the ones that is expected to exercise their leverage over a big consumption base well into the future.

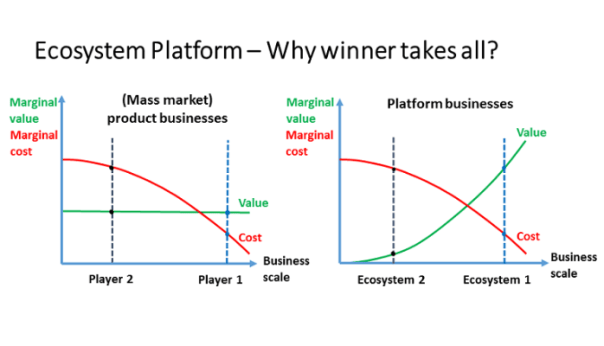

- Multi-sided platform impacts: The value of information across multiple subsystems: company, supplier, customer, government increases disproportionately as it expands. We had earlier noted that if cities expand by 100%, then there is increasing innovating and goods that generate 115% -the concept of super-linear scaling. As more nodes are introduced into the system and a better infrastructure is created to support communication and exchange between the nodes, the more entrenched the business becomes. And interestingly, the business grows at a sub-linear scale – namely, it consumes less and less resources in proportion to its growth. Hence, we see the large unicorn valuation among companies where investors and market makers place calculated bets on investments of colossal magnitudes. The magnitude of such investments is relatively a recent event, and this is largely driven by the advances in technology that connect all stakeholders.

- Investment in learning: To manage scale is to also be selective of information that a system receives and how the information is processed internally. In addition, how is this information relayed to the external system or environment. This requires massive investment in areas like machine learning, artificial intelligence, big data, enabling increased computational power, development of new learning algorithms, etc. This means that organizations have to align infrastructure and capability while also working with external environments through public relations, lobbying groups and policymakers to chaperone a comprehensive and a very complex hard-to-replicate learning organism.

- Investment in brand: Brand personifies the value attributes of an organization. One connects brand to customer experience and perception of the organization’s product. To manage scale and grow, organizations must invest in brand: to capture increased mindshare of the consumer. In complexity science terms, the internal systems are shaped to emit powerful signals to the external environment and urge a response. Brand and learning work together to allow a harmonic growth of an internal system in the context of its immediate environment.

However, one must revert to the science of complexity to understand the long-term challenges of a winner-take-all mechanism. We have already seen the example that what is good for the individual bull-elk might not be the best for the species in the long-term. We see that super-linear scaling systems also emits significant negative by-products. Thus, the question that we need to ask is whether the organizations are paradoxically cultivating their own seeds of destruction in their ambitions of pursuing scale and market entrenchment.

Internal versus External Scale

This article discusses internal and external complexity before we tee up a more detailed discussion on internal versus external scale. This chapter acknowledges that complex adaptive systems have inherent internal and external complexities which are not additive. The impact of these complexities is exponential. Hence, we have to sift through our understanding and perhaps even review the salient aspects of complexity science which have already been covered in relatively more detail in earlier chapter. However, revisiting complexity science is important, and we will often revisit this across other blog posts to really hit home the fundamental concepts and its practical implications as it relates to management and solving challenges at a business or even a grander social scale.

A complex system is a part of a larger environment. It is a safe to say that the larger environment is more complex than the system itself. But for the complex system to work, it needs to depend upon a certain level of predictability and regularity between the impact of initial state and the events associated with it or the interaction of the variables in the system itself. Note that I am covering both – complex physical systems and complex adaptive systems in this discussion. A system within an environment has an important attribute: it serves as a receptor to signals of external variables of the environment that impact the system. The system will either process that signal or discard the signal which is largely based on what the system is trying to achieve. We will dedicate an entire article on system engineering and thinking later, but the uber point is that a system exists to serve a definite purpose. All systems are dependent on resources and exhibits a certain capacity to process information. Hence, a system will try to extract as many regularities as possible to enable a predictable dynamic in an efficient manner to fulfill its higher-level purpose.

Let us understand external complexities. We can interchangeably use the word environmental complexity as well. External complexity represents physical, cultural, social, and technological elements that are intertwined. These environments beleaguered with its own grades of complexity acts as a mold to affect operating systems that are mere artifacts. If operating systems can fit well within the mold, then there is a measure of fitness or harmony that arises between an internal complexity and external complexity. This is the root of dynamic adaptation. When external environments are very complex, that means that there are a lot of variables at play and thus, an internal system has to process more information in order to survive. So how the internal system will react to external systems is important and they key bridge between those two systems is in learning. Does the system learn and improve outcomes on account of continuous learning and does it continually modify its existing form and functional objectives as it learns from external complexity? How is the feedback loop monitored and managed when one deals with internal and external complexities? The environment generates random problems and challenges and the internal system has to accept or discard these problems and then establish a process to distribute the problems among its agents to efficiently solve those problems that it hopes to solve for. There is always a mechanism at work which tries to align the internal complexity with external complexity since it is widely believed that the ability to efficiently align the systems is the key to maintaining a relatively competitive edge or intentionally making progress in solving a set of important challenges.

Internal complexity are sub-elements that interact and are constituents of a system that resides within the larger context of an external complex system or the environment. Internal complexity arises based on the number of variables in the system, the hierarchical complexity of the variables, the internal capabilities of information pass-through between the levels and the variables, and finally how it learns from the external environment. There are five dimensions of complexity: interdependence, diversity of system elements, unpredictability and ambiguity, the rate of dynamic mobility and adaptability, and the capability of the agents to process information and their individual channel capacities.

If we are discussing scale management, we need to ask a fundamental question. What is scale in the context of complex systems? Why do we manage for scale? How does management for scale advance us toward a meaningful outcome? How does scale compute in internal and external complex systems? What do we expect to see if we have managed for scale well? What does the future bode for us if we assume that we have optimized for scale and that is the key objective function that we have to pursue?

Debt Financing: Notable Elements to consider

We have discussed financing via Convertible Debts and Equity Financing. There is a third element that is equally important and ought to be in the arsenal for financing the working capital requirements for the company.

Here are some common Term Sheet lexicons that you have to be aware of for opening up a credit facility.

Formula based Line of Credit: There are some variants to this, but the key driver is that the LOC is extended against eligible receivables. Generally, eligible receivables are defined as receivables that are within 90 days at an uber level. There are some additional elements that can reduce the eligible base. Those items that can be excluded would be as follows

Accounts outstanding for more than 90 days from invoice date

Credit balances over 90 days

Foreign AR. Some banks would specifically exclude foreign AR.

Intra-Company AR

Banks might impose a concentration limit. For example, any account that represents more than 30% of the AR that is outstanding may be excluded from the mix. Alternatively, credit may be extended up to the cap of 30% and no more.

Cross Aging Limit of 35%, defined as those accounts where 35% or more of an accounts receivable past due (greater than 90 days). In such instances, the entire account is ineligible.

Pre-bills are not eligible. Services have to be rendered or goods shipped. That constitutes a true invoice.

Some instances, you may be precluded from including receivables from government. Non-Formula based LOC: Credit is extended not on AR but based on what you negotiate with the Bank. The Bank will generally provide a non-formula based LOC based on historical cash flows and EBITDA and a board-approved budget. In some instances, if you feel that you can capitalize the company via an equity line in the near future, the bank would be inclined to raise the LOC.

Interest Rate

In either of the above 2 cases, the interest rate charged is basically a prime reference rate + some basis points. For example, the bank may spell out that the interest rate is the Prime Referenced Rate + 1.25%. If the Prime rate is 3.25%, then the cost to the company is 4.5%. Note though that if the company is profitable and the average tax rate is 40%, then the real cost to the company is 4.5 %*( 1-40%) = 2.7%.

Maturity Period

For all facilities, there is Maturity Period. In most instances, it is 24 months. Interest is paid monthly and the principal is due at maturity.

Facility Fees

Banks will charge a Facility Fee. Depending on the size of the facility, there could be some amount due at close and some amount due at the first year anniversary from the date the facility contract has been executed.

First Priority Rights

Bank will have a first priority UCC-1 security interest on all assets of Borrower like present and future inventory, chattel paper, accounts, contract rights, unencumbered equipment, general intangibles (excluding intellectual property), and the right to proceeds from accounts receivable and inventory from the sale of intellectual property to repay any outstanding Bank debt.

Bank may insist on having the right to the IP. That becomes another negotiation point. You can negotiate a negative pledge which effectively means that you will not pledge your IP to any third party.

Bank Covenants

The Bank will also insist on some financial covenants. Some of the common covenants are

- Adjusted Quick Ratio which is (Cash held at the Bank + Eligible Receivables)/ (Current Liabilities less Deferred Revenue)

- Trailing EBITDA requirement. Could be a six month or 12 month trailing EBITDA requirement

- EBIT to Interest Coverage Ratio = EBIT/Interest Payments. Bank may require a 1.5 or 2 coverage.

Monthly Financial Requirements

Bank will require the monthly financial statements according to GAAP and the Bank Compliance Certificate.

Bank may seek an Audit or an independent review of the Financial Statements within 90-180 days after each fiscal year ends.

You will have to provide AR and AP aging monthly and inventory breakdown.

In the event that there is a reforecast of the Budget or Operating Plan and it has been approved by the Board, you will have to provide the information to the bank as well.

Bank Oversight and Audit

Bank will reserve the right to do a collateral audit for the formula based line of credit financing. You will have to pay the audit fees. In general, you can negotiate and cap these fees and the frequency of such audits.

Most of the above relate to a large number of startups that do not carry inventory and acquire inventory from international suppliers.

Bankers Acceptance

BAs are frequently used in international trade because of advantages for both sides. Exporters often feel safer relying on payment from a reputable bank than a business with which it has little if any history. Once the bank verifies, or “accepts”, a time draft, it becomes a primary obligation of that institution.

Here’s one typical example. You decide to purchase 100 widgets from Lee Ku, a Chinese exporter. After completing the trade agreement, you approach your bank for a letter of credit. This letter of credit makes your bank the intermediary responsible for completing the transaction.

Once Lee Ku, your supplier, ships the goods, it sends the appropriate documents – typically through its own financial bank to your bank in the United States. The exporter now has a couple choices. It could keep the acceptance until maturity, or it could sell it to a third party, perhaps to your bank responsible for making the payment. In this case, Lee Ku receives an amount less than the face value of the draft, but it doesn’t have to wait on the funds. Bank makes some fees and the Supplier gets their money.

When a bank buys back the acceptance at a lower price, it is said to be “discounting” the acceptance. If your bank does this, it essentially has the same choices that your Chinese exporter had. It could hold the draft until it matures, which is akin to extending the importer a loan. More commonly, though, the bank will charge you a fee in advance which is a percentage of the acceptance. Could be anywhere from 2-4% of the value of the acceptance. In theory, you can get anywhere between 90-180 days financing using BA as an instrument to fund your inventory.

Dangers of Debt Financing

Debt Financing can be a cheap financing method. However, it carries potential risk. If you are not able to service debt, then the bank can, at the extreme, force you into bankruptcy. Alternatively, they can put you in forbearance and work out a plan to get back their principal amount. They can take over the role of receivership and collect the money on your behalf. These are all draconian triggers that may happen, and hence it is important to maintain a good relationship with your banker. Most importantly, give them any bad news ahead of time. It is really bad when they learn of bad news later. It would limit your ability to negotiate terms with the bank.

Manage Debt

In general, if you draw down against the LOC, it is always a good idea to pay that down as soon as possible. That ought to be your primary operational strategy. That will minimize interest expense, keep the line open, establish a better rapport with the bank and most importantly – force you to become a more disciplined organization. You ought to regard the bank financing as a bridge for your working capital requirements. To the extent you can minimize the bridge by converting your receivables to cash, minimizing operating expenses, and maximizing your margin … you would be in a happier place. Debt financing also gives you the time to build value in the organization rather than relying upon equity line which is a costly form of financing. Having said that, there will be times when your investors may push back on your debt financing strategy. In fact, if you have raised equity prior to debt, you may even have to get signoff from the equity investors. Their big concern is that having leverage takes away from the value of the company. That is not necessarily true, because corporate finance theory suggests that intelligent debt financing can, in fact, increase corporate value. However, the investors may see debt as your way out to stall more investment requirements and thus defer their inclination toward owning more of your company at a lower value.

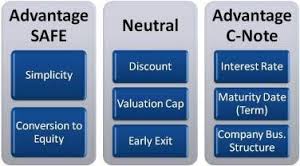

Convertible Debt: What, How, Plus, Minus?

Convertible Debt is also called convertible loans or convertible notes. This is a common method of financing for early stage companies. Typically, an investor or a group of investors (investor syndicate) extends a loan to a company that could later convert to an equity instrument. Like any debt, it is an interest bearing instrument. However, the key element in this form of financing is that the investors will get equity at a discount when the Company raises a Series A round. In other cases, it could be a warrant issue. In most instances, there is a cap on the valuation at which the debt will convert.

Hence, there are four key components of convertible debt:

- Convertible Debt has an interest.

- Convertible Debt has a discount

- Convertible Debt may have warrants

- Valuation at which Debt converts is capped.

Let us discuss each of these in detail.

Convertible Debt is interest bearing.

Like any debt, the borrower has a loan on their balance sheet. They are responsible for the principal and the interest. The interest is simple interest rate, and there is a fixed due date (or “maturity date”) for repayment of the amount borrowed. In other words, if there is no Series A funding before the maturity of the convertible debt, there could be some problems for the company. In an extreme case, the note holder can force the company into bankruptcy, unless the startup can renegotiate and extend the terms. The appropriate interest rate for convertible debt could be anywhere between 6% up to 10%. The Applicable Federal Rates (AFRs) can establish the lowest legally allowable interest rates.

Convertible Note Discount.

As a sweetener, the note will have an automatic conversion discount feature by which the investor will exchange the convertible debt for shares of a Series A Preferred Stock at a discount to the price per share paid by a VC in a Qualified Financing Round. Here is how this works:

A) Angel invests $100,000 in the startup company.

B) Startup issues the convertible note for $100K which has an interest and maturity date.

C) The Note has an automatic conversion feature at $1M with a conversion discount equal to 20%.

D) Now, let us say that the Startup closes $1M Series A Preferred Stock at $1 per share.

E) The Angel thus gets the shares at 80 cents.

F) So Angel gets $100,000/$0.80 per share of the Series A Preferred which totals to 125,000 shares.

Convertible Notes may have warrants.

The warrants are very similar to options. In a typical convertible note, the Warrant will be an option for whatever security is sold in the next round. It is often expressed in terms of “warrant coverage percentage”. A 20% warrant coverage means that you can take the same $1M, multiply by 20%, and the Warrant independently will enable you to get $200K of additional securities in the next round. For example, let us say a Series A round is $4M (Company has raised $4M). The warrant coverage kicks in and now the size of the round becomes $5.2M. ($4M New Fund + $1M size of Note + $200K warrant coverage = $5.2M) So there is a dilution impact of $1.2M for the $1M of angel cash that was extended in the form of the Note with the Warrant Coverage.

Convertible Notes Caps

Cap is a term that protects the angel investor and puts a ceiling on the conversion price of debt. This is seen mostly in seed financings. For example, angel invests a $100K in a company at 20% discount and thinks that the pre-money valuation maxes out at $3M. If the angel was correct and the valuation was indeed at $3M (assume $1.00 for preferred share) , then the angel would have 125,000 shares. That would be 125,000 shares/(3M shares + 125,000) = 4%. The investor would own 4% immediately upon Qualified Financing.

However, assume that the company is hugely successful and the pre-money valuation is assessed at $10M. Let us say that the preferred stock is at $1.00. So now you have 10M shares. Angel Investor gets 125,000 shares. Then the Investor is diluted down to 1.23%. (125K shares/ (10M shares + 125K shares)). Hence the higher the valuation in Series A, the investor gets diluted down further. Hence they use Convertible Notes Caps as a protection to their downside dilution risk. The cap sets a limit for how much the Company can raise before the investor’s shares stop getting diluted. It sets an upper limit. So if the investor in the above example sets a cap at $5M, then the discount would increase to offset the additional dilution that occurred. So in this case, the investor actually gets a 50% discount, not a 20% discount. It is important to note that the cap is structured as either or – in other words, the angel investor gets the value of the greater of the two discounts.

Advantages of Convertible Debt Financing

- Easy to raise

- Paperwork could be less than 10 pages.

- Quick turnaround time to get this signed off

- Terms are generally clearly defined

- Legal Expenses are typically less than $5000-$8000.

- Company can defer the valuation discussion until a later date

- Notes have fewer rights than Equity. Investors in Notes have less say in the direction and execution of company plans.

Disadvantages of Convertible Debt Financing

- It is a loan and there is a maturity date on the loan. If financing does not occur, the investor can recall the note and force the company into bankruptcy.

- Incentives are not necessarily aligned. Company wants more valuation in Series A but investor would want less to own larger pool. With a cap, they accomplish that but the Company owners are diluted down depending on cap or size of discount.

- Size of discount or cap could create problems for the Company seeking Series A. Series A investors might force a renegotiation thus increasing legal and other costs to the Company. A low valuation cap could adversely affect the owners of the Company.

- Conversion to equity would mean equivalent privileges with respect to rights. Bear in mind that angel investors are generally not professional VC’s and each of them have very different expertise. Equivalent rights for the different expertise may create problems and issues among all parties involved.

- Convertible Notes may have senior preferences. In the event of liquidation, the Note Holders are first in line to get their money back.

- Some angel investors may want subscription rights or super pro-rata rights to the next round of funding. This is to prevent their dilution. So they may want to have the option to participate up to a certain percentage of the next round. In other words, if the round is $5M, the subscription right might specify that the investor can participate up to 30% and that would mean that the investor has a bigger seat on the table. Such clauses may not be favorably looked at by Series A investor and these clauses could hold up financing.