Category Archives: Financial Metrics

Beyond the Buzz: The Real Economics Behind SaaS, AI, and Everything in Between

Introduction

Throughout my career, I have had the privilege of working in and leading finance teams across several SaaS companies. The SaaS model is familiar territory to me: its economics are well understood, its metrics are measurable, and its value creation pathways have been tested over time. Erich Mersch’s book on SaaS Hacks is my Bible. In contrast, my exposure to pure AI companies has been more limited. I have directly supported two AI-driven businesses, and much of my perspective comes from observation, benchmarking, and research. This combination of direct experience and external study has hopefully shaped a balanced view: one grounded in practicality yet open to the new dynamics emerging in the AI era.

Across both models, one principle remains constant: a business is only as strong as its unit economics. When leaders understand the economics of their business, they gain the ability to map them to daily operations, and from there, to the financial model. The linkage from unit economics to operations to financial statements is what turns financial insight into strategic control. It ensures that decisions on pricing, product design, and investment are all anchored in how value is truly created and captured.

Today, CFOs and CEOs must not only manage their profit and loss (P&L) statement but also understand the anatomy of revenue, cost, and cash flow at the micro level. SaaS, AI, and hybrid SaaS-AI models each have unique economic signatures. SaaS rewards scalability and predictability. AI introduces variability and infrastructure intensity. Hybrids offer both opportunity and complexity. This article examines the financial structure, gross margin profile, and investor lens of each model to help finance leaders not only measure performance but also interpret it by turning data into judgment and judgment into a better strategy.

Part I: SaaS Companies — Economics, Margins, and Investor Lens

The heart of any SaaS business is its recurring revenue model. Unlike traditional software, where revenue is recognized upfront, SaaS companies earn revenue over time as customers subscribe to a service. This shift from ownership to access creates predictable revenue streams but also introduces delayed payback cycles and continuous obligations to deliver value. Understanding the unit economics behind this model is essential for CFOs and CEOs, as it enables them to see beyond top-line growth and assess whether each customer, contract, or cohort truly creates long-term value.

A strong SaaS company operates like a flywheel. Customer acquisition drives recurring revenue, which funds continued innovation and improved service, in turn driving more customer retention and referrals. But a flywheel is only as strong as its components. The economics of SaaS can be boiled down to a handful of measurable levers: gross margin, customer acquisition cost, retention rate, lifetime value, and cash efficiency. Each one tells a story about how the company converts growth into profit.

The SaaS Revenue Engine

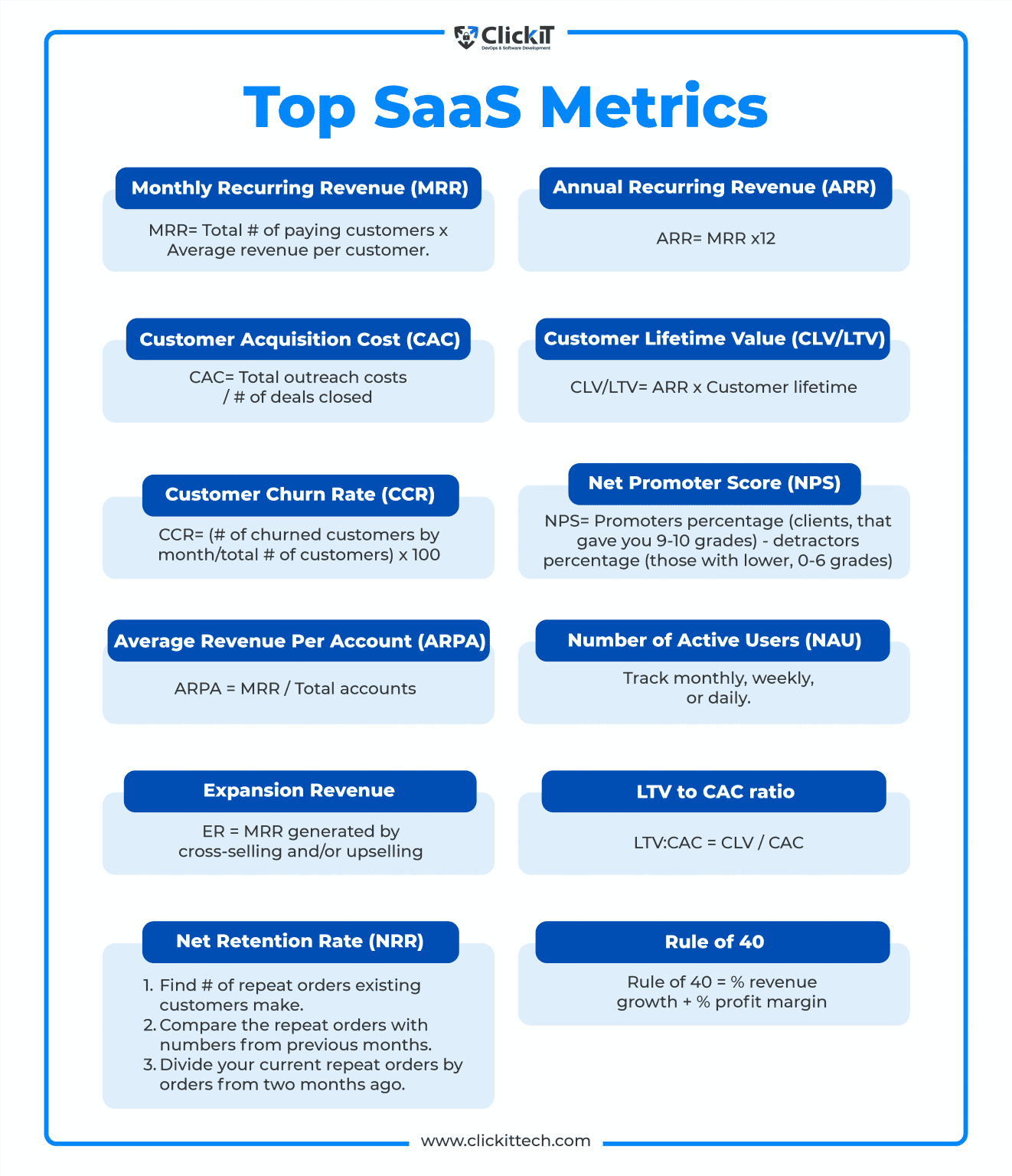

At its simplest, a SaaS company makes money by providing access to its platform on a subscription basis. The standard measure of health is Annual Recurring Revenue (ARR). ARR represents the contracted annualized value of active subscriptions. It is the lifeblood metric of the business. When ARR grows steadily with low churn, the company can project future cash flows with confidence.

Revenue recognition in SaaS is governed by time. Even if a customer pays upfront, the revenue is recognized over the duration of the contract. This creates timing differences between bookings, billings, and revenue. CFOs must track all three to understand both liquidity and profitability. Bookings signal demand, billings signal cash inflow, and revenue reflects the value earned.

One of the most significant advantages of SaaS is predictability. High renewal rates lead to stable revenues. Upsells and cross-sells increase customer lifetime value. However, predictability can also mask underlying inefficiencies. A SaaS business can grow fast and still destroy value if each new customer costs more to acquire than they bring in lifetime revenue. This is where unit economics comes into play.

Core Unit Metrics in SaaS

The three central metrics every CFO and CEO must know are:

- Customer Acquisition Cost (CAC): The total sales and marketing expenses needed to acquire one new customer.

- Lifetime Value (LTV): The total revenue a customer is expected to generate over their relationship with the company.

- Payback Period: The time it takes for gross profit from a customer to recover CAC.

A healthy SaaS business typically maintains an LTV-to-CAC ratio of at least 3:1. This means that for every dollar spent acquiring a customer, the company earns three dollars in lifetime value. Payback periods under twelve months are typically considered strong, especially in mid-market or enterprise SaaS. Long payback periods signal cash inefficiency and high-risk during downturns.

Retention is equally essential. The stickier the product, the lower the churn, and the more predictable the revenue. Net revenue retention (NRR) is a powerful metric because it combines churn and expansion. A business with 120 percent NRR is growing revenue even without adding new customers, which investors love to see.

Gross Margin Dynamics

Gross margin is the backbone of SaaS profitability. It measures how much of each revenue dollar remains after deducting direct costs, such as hosting, support, and third-party software fees. Well-run SaaS companies typically achieve gross margins of between 75% and 85%. This reflects the fact that software is highly scalable. Once built, it can be replicated at almost no additional cost. They use the margins to fund their GTM strategy. They have room until they don’t.

However, gross margin is not guaranteed. In practice, it can erode for several reasons. First, rising cloud infrastructure costs can quietly eat into margins if not carefully managed. Companies that rely heavily on AWS, Azure, or Google Cloud need cost optimization strategies, including reserved instances and workload tuning. Second, customer support and success functions, while essential, can become heavy if processes are not automated. Third, complex integrations or data-heavy products can increase variable costs per customer.

Freemium and low-entry pricing models can also dilute margins if too many users remain on free tiers or lower-paying plans. The CFO’s job is to ensure that pricing reflects the actual value delivered and that the cost-to-serve remains aligned with revenue per user. A mature SaaS company tracks unit margins by customer segment to identify where profitability thrives or erodes.

Operating Leverage and the Rule of 40

The power of SaaS lies in its potential for operating leverage. Fixed costs, such as R&D, engineering, and sales infrastructure, remain relatively constant as revenue scales. As a result, incremental revenue flows disproportionately to the bottom line once the business passes break-even. This makes SaaS an attractive model once scale is achieved, although reaching that scale can take a considerable amount of time.

The Rule of 40 is a shorthand metric many investors use to gauge the balance between growth and profitability. It states that a SaaS company’s revenue growth rate, plus its EBITDA margin, should equal or exceed 40 percent. A company growing 30 percent annually with a 15 percent EBITDA margin scores 45, which is considered healthy. A company growing at 60 percent but losing 30 percent EBITDA would score 30, suggesting inefficiency. This rule forces management to strike a balance between ambition and discipline. This 40% rule was based on empirical analysis, and every Jack and Jill swears by it. I am not sure that we can have this Rule and apply it blindly. I am not generally in favor of these broad rules. That is a lot of fodder for a different conversation.

Cash Flow and Efficiency

Cash flow timing is another defining feature of SaaS. Many customers prepay annually, creating favorable working capital dynamics. This gives SaaS companies negative net working capital, which can help fund growth. However, high upfront CAC and long payback periods can strain cash reserves. CFOs must ensure growth is financed efficiently and that burn multiples remain sustainable. Burn-multiple measures the cash burn relative to net new ARR added. A burn rate of multiple below 1 is excellent; it means the company spends one dollar to generate one dollar of recurring revenue. Ratios above 2 suggest inefficiency.

As markets have tightened, investors have shifted focus from pure growth to efficient growth. Cash is no longer cheap, and dilution from equity raises is costly. I attended a networking event in San Jose about a month ago, and one of the finance leaders said, “We are in the middle of a nuclear winter.” I thought that summarized the current state of the funding market. Therefore, SaaS CFOs must guide companies toward self-funding growth, improving gross margins, and shortening CAC payback cycles.

Valuation and Investor Perspective

Investors view SaaS companies through the lens of predictability, scalability, and margin potential. Historically, during low-interest-rate periods, high-growth SaaS companies traded at 10 to 15 times ARR. In the current normalized environment, top performers trade between 5 and 8 times ARR, with discounts for slower growth or lower margins.

The key drivers of valuation include:

- Growth Rate: Faster ARR growth leads to higher multiples, provided it is efficient.

- Gross Margin: High margins indicate scalability and control over cost structure.

- Retention and Expansion: Strong NRR signals durable revenue and pricing power.

- Profitability Trajectory: Investors reward companies that balance growth with clear paths to cash flow breakeven.

Investors now differentiate between the quality of growth and the quantity of growth. Revenue driven by deep discounts or heavy incentives is less valuable than revenue driven by customer adoption and satisfaction. CFOs must clearly communicate cohort performance, renewal trends, and contribution margins to demonstrate that growth is sustainable and durable.

Emerging Challenges in SaaS Economics

While SaaS remains a powerful model, new challenges have emerged. Cloud infrastructure costs are rising, putting pressure on gross margins. AI features are becoming table stakes, but they introduce new variable costs tied to compute. Customer expectations are also shifting toward usage-based pricing, which can lead to reduced predictability in revenue recognition.

To navigate these shifts, CFOs must evolve their financial reporting and pricing strategies. Gross margin analysis must now include compute efficiency metrics. Sales compensation plans must reflect profitability, not just bookings. Pricing teams must test elasticity to ensure ARPU growth outpaces cost increases.

SaaS CFOs must also deepen their understanding of cohort economics. Not all customers are equal. Some segments deliver faster payback and higher retention, while others create drag. Segmented reporting enables management to allocate capital wisely and avoid pursuing unprofitable markets.

The Path Forward

The essence of SaaS unit economics is discipline. Growth only creates value when each unit of growth strengthens the financial foundation. This requires continuous monitoring of margins, CAC, retention, and payback. It also requires cross-functional collaboration between finance, product, and operations. Finance must not only report outcomes but also shape strategy, ensuring that pricing aligns with value and product decisions reflect cost realities.

For CEOs, understanding these dynamics is vital to setting priorities. For CFOs, the task is to build a transparent model that links operational levers to financial outcomes. Investors reward companies that can tell a clear story with data: a path from top-line growth to sustainable free cash flow.

Ultimately, SaaS remains one of the most attractive business models when executed effectively. The combination of recurring revenue, high margins, and operating leverage creates long-term compounding value. But it rewards precision. The CFO who masters unit economics can turn growth into wealth, while the one who ignores it may find that scale without discipline is simply a faster road to inefficiency. The king is not dead: Long live the king.

Part II: Pure AI Companies — Economics, Margins, and Investor Lens

Artificial intelligence companies represent a fundamentally different business model from traditional SaaS. Where SaaS companies monetize access to pre-built software, AI companies monetize intelligence: the ability of models to learn, predict, and generate. This shift changes everything about unit economics. The cost per unit of value is no longer near zero. It is tied to the underlying cost of computation, data processing, and model maintenance. As a result, CFOs and CEOs leading AI-first companies must rethink what scale, margin, and profitability truly mean.

While SaaS scales easily once software is built, AI scales conditionally. Each customer interaction may trigger new inference requests, consume GPU time, and incur variable costs. Every additional unit of demand brings incremental expenses. The CFO’s challenge is to translate these technical realities into financial discipline, which involves building an organization that can sustain growth without being constrained by its own cost structure.

Understanding the AI Business Model

AI-native companies generate revenue by providing intelligence as a service. Their offerings typically fall into three categories:

- Platform APIs: Selling access to models that perform tasks such as image recognition, text generation, or speech processing.

- Enterprise Solutions: Custom model deployments tailored for specific industries like healthcare, finance, or retail.

- Consumer Applications: AI-powered tools like copilots, assistants, or creative generators.

Each model has unique economics. API-based businesses often employ usage-based pricing, resembling utilities. Enterprise AI firms resemble consulting hybrids, blending software with services. Consumer AI apps focus on scale, requiring low-cost inference to remain profitable.

Unlike SaaS subscriptions, AI revenue is often usage-driven. This makes it more elastic but less predictable. When customers consume more tokens, queries, or inferences, revenue rises but so do costs. This tight coupling between revenue and cost means margins depend heavily on technical efficiency. CFOs must treat cost-per-inference as a central KPI, just as SaaS leaders track gross margin percentage.

Gross Margins and Cost Structures

For pure AI companies, the gross margin reflects the efficiency of their infrastructure. In the early stages, margins often range between 40% and 60%. With optimization, some mature players approach 70 percent or higher. However, achieving SaaS-like margins requires significant investment in optimization techniques, such as model compression, caching, and hardware acceleration.

The key cost components include:

- Compute: GPU and cloud infrastructure costs are the most significant variable expenses. Each inference consumes compute cycles, and large models require expensive hardware.

- Data: Training and fine-tuning models involve significant data acquisition, labeling, and storage costs.

- Serving Infrastructure: Orchestration, latency management, and load balancing add further expenses.

- Personnel: Machine learning engineers, data scientists, and research teams represent high fixed costs.

Unlike SaaS, where the marginal cost per user declines toward zero, AI marginal costs can remain flat or even rise with increasing complexity. The more sophisticated the model, the more expensive it is to serve each request. CFOs must therefore design pricing strategies that match the cost-to-serve, ensuring unit economics remain positive.

To track progress, leading AI finance teams adopt new metrics such as cost per 1,000 tokens, cost per inference, or cost per output. These become the foundation for gross margin improvement programs. Without these metrics, management cannot distinguish between profitable and loss-making usage.

Capital Intensity and Model Training

A defining feature of AI economics is capital intensity. Training large models can cost tens or even hundreds of millions of dollars. These are not operating expenses in the traditional sense; they are long-term investments. The question for CFOs is how to treat them. Should they be expensed, like research and development, or capitalized, like long-lived assets? The answer depends on accounting standards and the potential for model reuse.

If a model will serve as a foundation for multiple products or customers over several years, partial capitalization may be a defensible approach. However, accounting conservatism often favors expensing, which depresses near-term profits. Regardless of treatment, management must view training costs as sunk investments that must earn a return through widespread reuse.

Due to these high upfront costs, AI firms must carefully plan their capital allocation. Not every model warrants training from scratch. Fine-tuning open-source or pre-trained models may achieve similar outcomes at a fraction of the cost. The CFO’s role is to evaluate return on invested capital in R&D and ensure technical ambition aligns with commercial opportunity.

Cash Flow Dynamics

Cash flow management in AI businesses is a significant challenge. Revenue often scales more slowly than costs in early phases. Infrastructure bills accrue monthly, while customers may still be in pilot stages. This results in negative contribution margins and high burn rates. Without discipline, rapid scaling can amplify losses.

The path to positive unit economics comes from optimization. Model compression, quantization, and batching can lower the cost per inference. Strategic use of lower-cost hardware, such as CPUs for lighter tasks, can also be beneficial. Some firms pursue vertical integration, building proprietary chips or partnering for preferential GPU pricing. Others use caching and heuristic layers to reduce the number of repeated inference calls.

Cash efficiency improves as AI companies move from experimentation to productization. Once a model stabilizes and workload patterns become predictable, cost forecasting and margin planning become more reliable. CFOs must carefully time their fundraising and growth, ensuring the company does not overbuild infrastructure before demand materializes.

Pricing Strategies

AI pricing remains an evolving art. Standard models include pay-per-use, subscription tiers with usage caps, or hybrid pricing that blends base access fees with variable usage charges. The proper structure depends on the predictability of usage, customer willingness to pay, and cost volatility.

Usage-based pricing aligns revenue with cost but increases forecasting uncertainty. Subscription pricing provides stability but can lead to margin compression if usage spikes. CFOs often employ blended approaches, utilizing base subscriptions that cover average usage, with additional fees for exceeding demand. This provides a buffer against runaway costs while maintaining customer flexibility.

Transparent pricing is crucial. Customers need clarity about what drives cost. Complexity breeds disputes and churn. Finance leaders should collaborate with product and sales teams to develop pricing models that are straightforward, equitable, and profitable. Scenario modeling helps anticipate edge cases where heavy usage erodes margins.

Valuation and Investor Perspective

Investors evaluate AI companies through a different lens than SaaS. Because AI is still an emerging field, investors look beyond current profitability and focus on technical moats, data advantages, and the scalability of cost curves. A strong AI company demonstrates three things:

- Proprietary Model or Data: Access to unique data sets or model architectures that competitors cannot easily replicate.

- Cost Curve Mastery: A clear path to reducing cost per inference as scale grows.

- Market Pull: Evidence of real-world demand and willingness to pay for intelligence-driven outcomes.

Valuations often blend software multiples with hardware-like considerations. Early AI firms may be valued at 6 to 10 times forward revenue if they show strong growth and clear cost reduction plans. Companies perceived as purely research-driven, without commercial traction, face steeper discounts. Investors are increasingly skeptical of hype and now seek proof of sustainable margins.

In diligence, investors focus on gross margin trajectory, data defensibility, and customer concentration. They ask questions like: How fast is the cost per inference declining? What portion of revenue comes from repeat customers? How dependent is the business on third-party models or infrastructure? The CFO’s job is to prepare crisp, data-backed answers.

Measuring Efficiency and Scale

AI CFOs must introduce new forms of cost accounting. Traditional SaaS dashboards that focus solely on ARR and churn are insufficient. AI demands metrics that link compute usage to financial outcomes. Examples include:

- Compute Utilization Rate: Percentage of GPU capacity effectively used.

- Model Reuse Ratio: Number of applications or customers served by a single trained model.

- Cost per Output Unit: Expense per generated item, prediction, or token.

By tying these technical metrics to revenue and gross margin, CFOs can guide engineering priorities. Finance becomes a strategic partner in improving efficiency, not just reporting cost overruns. In a later article, we will discuss complexity and Scale. I am writing a book on that subject, and this is highly relevant to how AI-based businesses are evolving. It is expected to be released by late February next year and will be available on Kindle as an e-book.

Risk Management and Uncertainty

AI companies face unique risks. Dependence on external cloud providers introduces pricing and supply risks. Regulatory scrutiny over data usage can limit access to models or increase compliance costs. Rapid technological shifts may render models obsolete before their amortization is complete. CFOs must build contingency plans, diversify infrastructure partners, and maintain agile capital allocation processes.

Scenario planning is essential. CFOs should model high, medium, and low usage cases with corresponding cost structures. Sensitivity analysis on cloud pricing, GPU availability, and demand elasticity helps avoid surprises. Resilience matters as much as growth.

The Path Forward

For AI companies, the journey to sustainable economics is one of learning curves. Every technical improvement that reduces the cost per unit enhances the margin. Every dataset that improves model accuracy also enhances customer retention. Over time, these compounding efficiencies create leverage like SaaS, but the path is steeper.

CFOs must view AI as a cost-compression opportunity. The winners will not simply have the best models but the most efficient ones. Investors will increasingly value businesses that show declining cost curves, strong data moats, and precise product-market fit.

For CEOs, the message is focus. Building every model from scratch or chasing every vertical can drain capital. The best AI firms choose their battles wisely, investing deeply in one or two defensible areas. Finance leaders play a crucial role in guiding these choices with evidence, rather than emotion.

In summary, pure AI companies operate in a world where scale is earned, not assumed. The economics are challenging but not insurmountable. With disciplined pricing, rigorous cost tracking, and clear communication to investors, AI businesses can evolve from capital-intensive experiments into enduring, high-margin enterprises. The key is turning intelligence into economics and tackling it one inference at a time.

Part III: SaaS + AI Hybrid Models: Economics and Investor Lens

In today’s market, most SaaS companies are no longer purely software providers. They are becoming intelligence platforms, integrating artificial intelligence into their products to enhance customer value. These hybrid models combine the predictability of SaaS with the innovation of AI. They hold great promises, but they also introduce new complexities in economics, margin structure, and investor expectations. For CFOs and CEOs, the challenge is not just understanding how these elements coexist but managing them in harmony to deliver profitable growth.

The hybrid SaaS-AI model is not simply the sum of its parts. It requires balancing two different economic engines: one that thrives on recurring, high-margin revenue and another that incurs variable costs linked to compute usage. The key to success lies in recognizing where AI enhances value and where it risks eroding profitability. Leaders who can measure, isolate, and manage these dynamics can unlock superior economics and investor confidence.

The Nature of Hybrid SaaS-AI Businesses

A hybrid SaaS-AI company starts with a core subscription-based platform. Customers pay recurring fees for access, support, and updates. Additionally, the company leverages AI-powered capabilities to enhance automation, personalization, analytics, and decision-making. These features can be embedded into existing workflows or offered as add-ons, sometimes billed based on usage.

Examples include CRMs with AI-assisted forecasting, HR platforms with intelligent candidate screening, or project tools with predictive insights. In each case, AI transforms user experience and perceived value, but it also introduces incremental cost per transaction. Every inference call, data model query, or real-time prediction consumes compute power and storage.

This hybridization reshapes the traditional SaaS equation. Revenue predictability remains strong due to base subscriptions, but gross margins become more variable. CFOs must now consider blended margins and segment economics. The task is to ensure that AI features expand total lifetime value faster than they inflate cost-to-serve.

Dual Revenue Streams and Pricing Design

Hybrid SaaS-AI companies often operate with two complementary revenue streams:

- Subscription Revenue: Fixed or tiered recurring revenue, predictable and contract-based.

- Usage-Based Revenue: Variable income tied to AI consumption, such as per query, token, or transaction.

This dual model offers flexibility. Subscriptions provide stability, while usage-based revenue captures upside from heavy engagement. However, it also complicates forecasting. CFOs must model revenue variance under various usage scenarios and clearly communicate these assumptions to the Board and investors.

Pricing design becomes a strategic lever. Some firms include AI features in premium tiers to encourage upgrades. Others use consumption pricing, passing compute costs directly to customers. The right approach depends on customer expectations, cost structure, and product positioning. For enterprise markets, predictable pricing is often a preferred option. For developer- or API-driven products, usage-based pricing aligns better with the delivery of value.

The most effective hybrid models structure pricing so that incremental revenue per usage exceeds incremental cost per usage. This ensures positive unit economics across both streams. Finance teams should run sensitivity analyses to test break-even points and adjust thresholds as compute expenses fluctuate.

Gross Margin Bifurcation

Gross margin in hybrid SaaS-AI companies must be analyzed in two layers:

- SaaS Core Margin: Typically, 75 to 85 percent is driven by software delivery, hosting, and support.

- AI Layer Margin: Often 40 to 60 percent, and it depends on compute efficiency and pricing.

When blended, the total margin may initially decline, especially if AI usage grows faster than subscription base revenue. The risk is that rising compute costs erode profitability before pricing can catch up. To manage this, CFOs should report segmented gross margins to the Board. This transparency helps avoid confusion when consolidated margins fluctuate.

The goal is not to immediately maximize blended margins, but to demonstrate a credible path toward margin expansion through optimization. Over time, as AI models become more efficient and the cost per inference declines, blended margins can recover. Finance teams should measure and communicate progress in terms of margin improvement per usage unit, not just overall percentages.

Impact on Customer Economics

AI features can materially improve customer economics. They increase stickiness, reduce churn, and create opportunities for upsell. A customer who utilizes AI-driven insights or automation tools is more likely to renew, as the platform becomes an integral part of their workflow. This improved retention directly translates into a higher lifetime value.

In some cases, AI features can also justify higher pricing or premium tiers. The key is measurable value. Customers pay more when they see clear ROI: for example, faster decision-making, labor savings, or improved accuracy. CFOs should work with product and customer success teams to quantify these outcomes and use them in renewal and pricing discussions.

The critical financial question is whether AI-enhanced LTV grows faster than CAC and variable cost. If so, AI drives profitable growth. If not, it becomes an expensive feature rather than a revenue engine. Regular cohort analysis helps ensure that AI adoption is correlated with improved unit economics.

Operating Leverage and Efficiency

Hybrid SaaS-AI companies must rethink operating leverage. Traditional SaaS gains leverage by spreading fixed costs over recurring revenue. In contrast, AI introduces variable costs tied to usage. This weakens the traditional leverage model. To restore it, finance leaders must focus on efficiency levers within AI operations.

Techniques such as caching, batching, and model optimization can reduce compute costs per request. Partnering with cloud providers for reserved capacity or leveraging model compression can further improve cost efficiency. The finance team’s role is to quantify these savings and ensure engineering priorities align with economic goals.

Another form of leverage comes from data reuse. The more a single model or dataset serves multiple customers or use cases, the higher the effective ROI on data and training investment. CFOs should track data utilization ratios and model reuse metrics as part of their financial dashboards.

Cash Flow and Capital Planning

Cash flow in hybrid businesses depends on the balance between stable subscription inflows and variable infrastructure outflows. CFOs must forecast not only revenue but also compute consumption. During early rollout, AI usage can spike unpredictably, leading to cost surges. Scenario planning is essential. Building buffers into budgets prevents margin shocks.

Capital allocation should prioritize scalability. Investments in AI infrastructure should follow demonstrated demand, not speculative projections. Over-provisioning GPU capacity can result in unnecessary cash expenditures. Many firms start with cloud credits or pay-as-you-go models before committing to long-term leases or hardware purchases. The objective is to match the cost ramp with revenue realization.

As with SaaS, negative working capital from annual prepayments can be used to fund expansion. However, CFOs should reserve portions of this cash for compute variability and cost optimization initiatives.

Investor Perspective

Investors view hybrid SaaS-AI models with both enthusiasm and scrutiny. They appreciate the potential for differentiation and pricing power, but expect clear evidence that AI integration enhances, rather than dilutes, economics. The investment thesis often centers on three questions:

- Does AI materially increase customer lifetime value?

- Can the company sustain or improve gross margins as AI usage scales?

- Is there a clear path to efficient growth under the Rule of 40?

Companies that answer yes to all three earn premium valuations. Investors will typically apply core SaaS multiples (5 to 8 times Annual Recurring Revenue, or ARR) with modest uplifts if AI features drive measurable revenue growth. However, if AI costs are poorly controlled or margins decline, valuations compress quickly.

To maintain investor confidence, CFOs must provide transparency. This includes segmented reporting, sensitivity scenarios, and clear explanations of cost drivers. Investors want to see not just innovation, but financial stewardship.

Strategic Positioning

The strategic role of AI within a SaaS company determines how investors perceive it. There are three broad positioning models:

- AI as a Feature: Enhances existing workflows but is not core to monetization. Example: an email scheduling tool with AI suggestions.

- AI as a Co-Pilot: Drives user productivity and becomes central to customer experience. Example: CRM with AI-generated insights.

- AI as a Platform: Powers entire ecosystems and opens new revenue lines. Example: a developer platform offering custom AI models.

Each model carries different costs and pricing implications. CFOs should ensure that the company’s financial model aligns with its strategic posture. A feature-based AI approach should be margin-accretive. A platform-based approach may accept lower margins initially in exchange for future ecosystem revenue.

Risk Management and Governance

Hybrid models also introduce new risks. Data privacy, model bias, and regulatory compliance can create unexpected liabilities. CFOs must ensure robust governance frameworks are in place. Insurance, audit, and legal teams should work closely together to manage exposure effectively. Transparency in AI decision-making builds customer trust and reduces reputational risk.

Another risk is dependency on third-party models or APIs. Companies that use external large language models face risks related to cost and reliability. CFOs should evaluate the total cost of ownership between building and buying AI capabilities. Diversifying across providers or developing proprietary models can mitigate concentration risk.

The CFO’s Role

In hybrid SaaS-AI organizations, the CFO’s role expands beyond financial reporting. Finance becomes the integrator of technology, strategy, and economics. The CFO must help design pricing strategies, measure the cost-to-serve, and effectively communicate value to investors. This requires fluency in both financial and technical language.

Regular dashboards should include metrics such as blended gross margin, compute cost per user, AI utilization rate, and LTV uplift resulting from AI adoption. This data-driven approach allows management to make informed trade-offs between innovation and profitability.

The CFO also acts as an educator. Boards and investors may not yet be familiar with AI-driven cost structures. Clear, simple explanations build confidence and support strategic decisions.

The Path Forward

The future belongs to companies that combine SaaS predictability with AI intelligence. Those who succeed will treat AI not as a novelty but as an economic engine. They will manage AI costs with the same rigor they apply to headcount or cloud spend. They will design pricing that reflects value creation, not just usage volume. And they will communicate to investors how each new AI feature strengthens the overall financial model.

Hybrid SaaS-AI companies occupy the forefront of modern business economics. They demonstrate that innovation and discipline are not opposites, but they are partners working toward a common objective. For CFOs and CEOs, the path forward is clear: measure what matters, value price, and guide the organization with transparency and foresight. Over time, this combination of creativity and control will separate enduring leaders from experimental wanderers.

Summary

In every business model, clarity around unit economics forms the foundation for sound decision-making. Whether one is building a SaaS company, an AI company, or a hybrid of both, understanding how revenue and costs behave at the most granular level allows management to design operations and financial models that scale intelligently. Without that clarity, growth becomes noise and is not sustainable.

From years of working across SaaS businesses, I have seen firsthand how the model rewards discipline. Predictable recurring revenue, high gross margins, and scalable operating leverage create a compounding effect when managed carefully. The challenge lies in balancing acquisition cost, retention, and cash efficiency, so that each new unit of growth strengthens rather than strains the business.

In AI, the economic story changes. Here, each unit of output incurs tangible costs, such as computation, data, and inference. The path to profitability lies not in volume alone, but in mastering the cost curve. Efficiency, model reuse, and pricing alignment become as critical as sales growth. AI firms must show investors that scaling demand will compress, not inflate, the cost per unit. I have no clue how they intend to do that with GPU demand going through the roof, but in this article, let us assume for giggles that there will be a light at the end of the tunnel, and GPU costs will temper down so it can fuel AI-driven business.

For hybrid SaaS-AI businesses, success depends on integration. AI should deepen customer value, expand lifetime revenue, and justify incremental costs. CFOs and CEOs must manage dual revenue streams, measure blended margins, and communicate transparently with investors about both the promise and the trade-offs of AI adoption.

Ultimately, understanding economics is knowing the truth. I am an economist, and I like to think I am unbiased. It enables leaders to align ambition with reality and design financial models that convey a credible narrative. As the lines between SaaS and AI continue to blur, those who understand the economics underlying innovation will be best equipped to build companies that endure.

How Strategic CFOs Drive Sustainable Growth and Change

When people ask me what the most critical relationship in a company really is, I always say it’s the one between the CEO and the CFO. And no, I am not being flippant. In my thirty years helping companies manage growth, navigate crises, and execute strategic shifts, the moments that most often determine success or spiraled failure often rests on how tightly the CEO and CFO operate together. One sets a vision. The other turns aspiration into action. Alone, each has influence; together, they can transform the business.

Transformation, after all, is not a project. It is a culture shift, a strategic pivot, a redefinition of operating behaviors. It’s more art than engineering and more people than process. And at the heart of it lies a fundamental tension: You need ambition, yet you must manage risk. You need speed, but you cannot abandon discipline. You must pursue new business models while preserving your legacy foundations. In short, you need to build simultaneously on forward momentum and backward certainty.

That complexity is where the strategic CFO becomes indispensable. The CFO’s job is not just to count beans, it’s to clear the ground where new plants can grow. To unlock capital without unleashing chaos. To balance accountable rigor with growth ambition. To design transformation from the numbers up, not just hammer it into the planning cycle. When this role is fulfilled, the CEO finds their most trusted confidante, collaborator, and catalyst.

Think of it this way. A CEO paints a vision: We must double revenue, globalize our go-to-market, pivot into new verticals, revamp the product, or embrace digital. It sounds exciting. It feels bold. But without a financial foundation, it becomes delusional. Does the company have the cash runway? Can the old cost base support the new trajectory? Are incentives aligned? Are the systems ready? Will the board nod or push back? Who is accountable if sales forecast misses or an integration falters? A CFO’s strategic role is to bring those questions forward not cynically, but constructively—so the ambition becomes executable.

The best CEOs I’ve worked with know this partnership instinctively. They build strategy as much with the CFO as with the head of product or sales. They reward honest challenge, not blind consensus. They request dashboards that update daily, not glossy decks that live in PowerPoint. They ask, “What happens to operating income if adoption slows? Can we reverse full-time hiring if needed? Which assumptions unlock upside with minimal downside?” Then they listen. And change. That’s how transformation becomes durable.

Let me share a story. A leader I admire embarked on a bold plan: triple revenue in two years through international expansion and a new channel model. The exec team loved the ambition. Investors cheered. But the CFO, without hesitation, did not say no. She said let us break it down. Suppose it costs $30 million to build international operations, $12 million to fund channel enablement, plus incremental headcount, marketing expenses, R&D coordination, and overhead. Let us stress test the plan. What if licensing stalls? What if fulfillment issues delay launches? What if cross-border tax burdens permanently drag down the margin?

The CEO wanted the bold headline number. But together, they translated it into executable modules. They set up rolling gates: a $5 million pilot, learn, fund next $10 million, learn, and so on. They built exit clauses. They aligned incentives so teams could pivot without losing credibility. They also built redundancy into systems and analytics, with daily data and optionality-based budgeting. The CEO had the vision, but the CFO gave it a frame. That is partnership.

That framing role extends beyond capital structure or P&L. It bleeds into operating rhythm. The strategic CFO becomes the architect of transformation cadence. They design how weekly, monthly, and quarterly look and feel. They align incentive schemes so that geography may outperform globally while still holding central teams accountable. They align finance, people, product, and GTM teams to shared performance metrics—not top-level vanity metrics, but actionable ones: user engagement, cost per new customer, onboarding latency, support burden, renewal velocity. They ensure data is not stashed in silos. They make it usable, trusted, visible. Because transformation is only as effective as your ability to measure missteps, iterate, and learn.

This is why I say the CFO becomes a strategic weapon: a lever for insight, integration, and investment.

Boards understand this too, especially when it is too late. They see CEOs who talk of digital transformation while still approving global headcount hikes. They see operating legacy systems still dragging FY ‘Digital 2.0’ ambition. They see growth funded, but debt rising with little structural benefit. In those moments, they turn to the CFO. The board does not ask the CFO if they can deliver the numbers. They ask whether the CEO can. They ask, “What’s the downside exposure? What are the guardrails? Who is accountable? How long will transformation slow profitability? And can we reverse if needed?”

That board confidence, when positive, is not accidental. It comes from a CFO who built that trust, not by polishing a spreadsheet, but by building strategy together, testing assumptions early, and designing transformation as a financial system.

Indeed, transformation without control is just creative destruction. And while disruption may be trendy, few businesses survive without solid footing. The CFO ensures that disruption does not become destruction. That investments scale with impact. That flexibility is funded. That culture is not ignored. That when exceptions arise, they do not unravel behaviors, but refocus teams.

This is often unseen. Because finance is a support function, not a front-facing one. But consider this: it is finance that approves the first contract. Finance assists in setting the commission structure that defines behavior. Finance sets the credit policy, capital constraints, and invoice timing, and all of these have strategic logic. A CFO who treats each as a tactical lever becomes the heart of transformation.

Take forecasting. Transformation cannot run on backward-moving averages. Yet too many companies rely on year-over-year rates, lagged signals, and static targets. The strategic CFO resurrects forecasting. They bring forward leading indicators of product usage, sales pipeline, supply chain velocity. They reframe forecasts as living systems. We see a dip? We call a pivot meeting. We see high churn? We call the product team. We see hiring cost creep? We call HR. Forewarned is forearmed. That is transformation in flight.

On the capital front, the CFO becomes a barbell strategist. They pair patient growth funding with disciplined structure. They build in fields of optionality: reserves for opportunistic moves, caps on unfunded headcount, staged deployment, and scalable contracts. They calibrate pricing experiments. They design customer acquisition levers with off ramps. They ensure that at every step of change, you can set a gear to reverse—without losing momentum, but with discipline.

And they align people. Transformation hinges on mindset. In fast-moving companies, people often move faster than they think. Great leaders know this. The strategic CFO builds transparency into compensation. They design equity vesting tied to transformation metrics. They design long-term incentives around cross-functional execution. They also design local authority within discipline. Give leaders autonomy, but align them to the rhythm of finance. Even the best strategy dies when every decision is a global approval. Optionality must scale with coordination.

Risk management transforms too. In the past, the CFO’s role in transformation was to shield operations from political turbulence. Today, it is to internally amplify controlled disruption. That means modeling volatility with confidence. Scenario modeling under market shock, regulatory shift, customer segmentation drift. Not just building firewalls, but designing escape ramps and counterweights. A transformation CFO builds risk into transformation—but as a system constraint to be managed, not a gate to prevent ambition.

I once had a CEO tell me they felt alone when delivering digital transformation. HR was not aligned. Product was moving too slowly. Sales was pushing legacy business harder. The CFO had built a bridge. They brought HR, legal, sales, and marketing into weekly update sessions, each with agreed metrics. They brokered resolutions. They surfaced trade-offs confidently. They pressed accountability floor—not blame, but clarity. That is partnership. That is transformation armor.

Transformation also triggers cultural tectonics. And every tectonic shift features friction zones—power renegotiation, process realignment, work redesign. Without financial discipline, politics wins. Mistrust builds. Change derails. The strategic CFO intervenes not as a policeman, but as an arbiter of fairness: If people are asked to stretch, show them the ROI. If processes migrate, show them the rationale. If roles shift, unpack the logic. Maintaining trust alignment during transformation is as important as securing funding.

The ability to align culture, capital, cadence, and accountability around a single north star—that is the strategic CFO’s domain.

And there is another hidden benefit: the CFO’s posture sets the tone for transformation maturity. CFOs who co-create, co-own, and co-pivot build transformation muscle. Those companies that learn together scale transformation together.

I once wrote that investors will forgive a miss if the learning loops are obvious. That is also true inside the company. When a CEO and CFO are aligned, and the CFO is the first to acknowledge what is not working to expectations, when pivots are driven by data rather than ego, that establishes the foundation for resilient leadership. That is how companies rebuild trust in growth every quarter. That is how transformation becomes a norm.

If there is a fear inside the CFO community, it is the fear of being visible. A CFO may believe that financial success is best served quietly. But the moment they step confidently into transformation, they change that dynamic. They say: Yes, we own the books. But we also own the roadmap. Yes, we manage the tail risk. But we also amplify the tail opportunity. That mindset is contagious. It builds confidence across the company and among investors. That shift in posture is more valuable than any forecast.

So let me say it again. Strategy is not a plan. Mechanics do not make execution. Systems do. And at the junction of vision and execution, between boardroom and frontline, stands the CFO. When transformation is on the table, the CFO walks that table from end to end. They make sure the chairs are aligned. The evidence is available. The accountability is shared. The capital is allocated, measured, and adapted.

This is why I refer to the CFO as the CEO’s most important ally. Not simply a confidante. Not just a number-cruncher. A partner in purpose. A designer of execution. A steward of transformation. Which is why, if you are a CFO reading this, I encourage you: step forward. You do not need permission to rethink transformation. You need conviction to shape it. And if you can build clarity around capital, establish a cadence for metrics, align incentives, and implement systems for governance, you will make your CEO’s job easier. You will elevate your entire company. You will unlock optionality not just for tomorrow, but for the years that follow. Because in the end, true transformation is not a moment. It is a movement. And the CFO, when prepared, can lead it.

The Power of Customer Lifetime Value in Modern Business

In contemporary business discourse, few metrics carry the strategic weight of Customer Lifetime Value (CLV). CLV and CAC are prime metrics. For modern enterprises navigating an era defined by digital acceleration, subscription economies, and relentless competition, CLV represents a unifying force, uniting finance, marketing, and strategy into a single metric that measures not only transactions but also the value of relationships. Far more than a spreadsheet calculation, CLV crystallizes lifetime revenue, loyalty, referral impact, and long-term financial performance into a quantifiable asset.

This article explores CLV’s origins, its mathematical foundations, its role as a strategic North Star across organizational functions, and the practical systems required to integrate it fully into corporate culture and capital allocation. It also highlights potential pitfalls and ethical implications.

I. CLV as a Cross-Functional Metric

CLV evolved from a simple acknowledgement: not all customers are equally valuable, and many businesses would prosper more by nurturing relationships than chasing clicks. The transition from single-sale tallies to lifetime relationship value gained momentum with the rise of subscription models—telecom plans, SaaS platforms, and membership programs—where the fiscal significance of recurring revenue became unmistakable.

This shift reframed capital deployment and decision-making:

- Marketing no longer seeks volume unquestioningly but targets segments with high long-term value.

- Finance integrates CLV into valuation models and capital allocation frameworks.

- Strategy uses it to guide M&A decisions, pricing stratagems, and product roadmap prioritization.

Because CLV is simultaneously a financial measurement and a customer-centric tool, it builds bridges—translating marketing activation into board-level impact.

II. How to calculate CLV

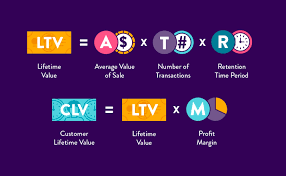

At its core, CLV employs economic modeling similar to net present value. A basic formula:

CLV = ∑ (t=0 to T) [(Rt – Ct) / (1 + d)^t]

- Rt = revenue generated at time t

- Ct = cost to serve/acquire at time t

- d = discount rate

- T = time horizon

This anchors CLV in well-accepted financial principles: discounted future cash flows, cost allocation, and multi-period forecasting. It satisfies CFO requirements for rigor and measurability.

However, marketing leaders often expand this to capture:

- Referral value (Rt includes not just direct sales, but influenced purchases)

- Emotional or brand-lift dimensions (e.g., window customers who convert later)

- Upselling, cross-selling, and tiered monetization over time

These expansions refine CLV into a dynamic forecast rather than a static average—one that responds to segmentation and behavioral triggers.

III. CLV as a Board-Level Metric

A. Investment and Capital Prioritization

Traditional capital decisions rely on ROI, return on invested capital (ROIC), and earnings multiples. CLV adds nuance: it gauges not only immediate returns but extended client relationships. This enables an expanded view of capital returns.

For example, a company might shift budget from low-CLV acquisition channels to retention-focused strategies—investing more in on-boarding, product experience, or customer success. These initiatives, once considered costs, now become yield-generating assets.

B. Segment-Based Acquisition

CLV enables precision targeting. A segment that delivers a 6:1 lifetime value-to-acquisition-cost (LTV:CAC) ratio is clearly more valuable than one delivering 2:1. Marketing reallocates spend accordingly, optimizing strategic segmentation and media mix, tuning messaging for high-value cohorts.

Because CLV is quantifiable and forward-looking, it naturally aligns marketing decisions with shareholder-driven metrics.

C. Tiered Pricing and Customer Monetization

CLV is also central to monetization strategy. Churn, upgrade rates, renewal behaviors, and pricing power all can be evaluated through the lens of customer value over time. Versioning, premium tiers, loyalty benefits—all become levers to maximize lifetime value. Finance and strategy teams model these scenarios to identify combinations that yield optimal returns.

D. Strategic Partnerships and M&A

CLV informs deeper decisions about partnerships and mergers. In evaluating a potential platform acquisition, projected contribution to overall CLV may be a decisive factor, especially when combined customer pools or cross-sell ecosystems can amplify lifetime revenue. It embeds customer value insights into due diligence and valuation calculations.

IV. Organizational Integration: A Strategic Imperative

Effective CLV deployment requires more than good analytics—it demands structural clarity and cultural alignment across three key functions.

A. Finance as Architect

Finance teams frame the assumptions—discount rates, cost allocation, margin calibration—and embed CLV into broader financial planning and analysis. Their task: convert behavioral data and modeling into company-wide decision frameworks used in investment reviews, budgeting, and forecasting processes.

B. Marketing as Activation Engine

Marketing owns customer acquisition, retention campaigns, referral programs, and product messaging. Their role is to feed the CLV model with real data: conversion rates, churn, promotion impact, and engagement flows. In doing so, campaigns become precision tools tuned to maximize customer yield rather than volume alone.

C. Strategy as Systems Designer

The strategy team weaves CLV outputs into product roadmaps, pricing strategy, partnership design, and geographic expansion. Using CLV foliated by cohort and channel, strategy leaders can sequence investments to align with long-term margin objectives—such as a five-year CLV-driven revenue mix.

V. Embedding CLV Into Corporate Processes

The following five practices have proven effective at embedding CLV into organizational DNA:

- Executive Dashboards

Incorporate LTV:CAC ratios, cohort retention rates, and segment CLV curves into executive reporting cycles. Tie leadership incentives (e.g., bonuses, compensation targets) to long-term value outcomes. - Cross-Functional CLV Cells

Establish CLV analytics teams staffed by finance, marketing insights, and data engineers. They own CLV modeling, simulation, and distribution across functions. - Monthly CLV Reviews

Monthly orchestration meetings integrate metrics updates, marketing feedback on campaigns, pricing evolution, and retention efforts. Simultaneous adjustment across functions allows dynamic resource allocation. - Capital Allocation Gateways

Projects involving customer-facing decisions—from new products to geographic pullbacks—must include CLV impact assessments in gating criteria. These can also feed into product investment requests and ROI thresholds. - Continuous Learning Loops

CLV models must be updated with actual lifecycle data. Regular recalibration fosters learning from retention behaviors, pricing experiments, churn drivers, and renewal rates—fueling confidence in incremental decision-making.

VI. Caveats and Limitations

CLV, though powerful, is not a cure-all. These caveats merit attention:

- Data Quality: Poorly integrated systems, missing customer identifiers, or inconsistent cohort logic can produce misleading CLV metrics.

- Assumption Risk: Discount rates, churn decay, turnaround behavior—all are model assumptions. Unqualified confidence can mislead investment.

- Narrow Focus: High CLV may chronically favor established segments, leaving growth through new markets or products underserved.

- Over-Targeting Risk: Over-optimizing for short-term yield may harm brand reputation or equity with broader audiences.

Therefore, CLV must be treated with humility—an advanced tool requiring discipline in measurement, calibration, and multi-dimensional insight.

VII. The Influence of Digital Ecosystems

Modern digital ecosystems deliver immense granularity. Every interaction—click, open, referral, session length—is measurable. These dark data provide context for CLV testing, segment behavior, and risk triggers.

However, this scale introduces overfitting risk: spurious correlations may override structural signals. Successful organizations maintain a balance—leveraging high-frequency signals for short-cycle interventions, while retaining medium-term cohort logic for capital allocation and strategic initiatives.

VIII. Ethical and Brand Implications

“CLV”, when viewed through a values lens, also becomes a cultural and ethical marker. Decisions informed by CLV raise questions:

- To what extent should a business monetize a cohort? Is excessive monetization ethical?

- When loyalty programs disproportionately reward high-value customers, does brand equity suffer among moderate spenders?

- When referral bonuses attract opportunists rather than advocates, is brand authenticity compromised?

These considerations demand that CLV strategies incorporate brand and ethical governance, not just financial optimization.

IX. Cross-Functionally Harmonized Governance

A robust operating model to sustain CLV alignment should include:

- Structured Metrics Governance: Common cohort definitions, discount rates, margin allocation, and data timelines maintained under joint sponsorship.

- Integrated Information Architecture: Real-time reporting, defined data lineage (acquisition to LTV), and cross-functional access.

- Quarterly Board Oversight: Board-level dashboards that track digital customer performance and CLV trends as fundamental risk and opportunity signals.

- Ethical Oversight Layer: Cross-functional reviews ensuring CLV-driven decisions don’t undermine customer trust or brand perception.

X. CLV as Strategic Doctrine

When deployed with discipline, CLV becomes more than a metric—it becomes a cultural doctrine. The essential tenets are:

- Time horizon focus: orienting decisions toward lifetime impact rather than short-cycle transactions.

- Cross-functional governance: embedding CLV into finance, marketing, and strategy with shared accountability.

- Continuous recalibration: creating feedback loops that update assumptions and reinforce trust in the metric.

- Ethical stewardship: ensuring customer relationships are respected, brand equity maintained, and monetization balanced.

With that foundation, CLV can guide everything from media budgets and pricing plans to acquisition strategy and market expansion.

Conclusion

In an age where customer relationships define both resilience and revenue, Customer Lifetime Value stands out as an indispensable compass. It unites finance’s need for systematic rigor, marketing’s drive for relevance and engagement, and strategy’s mandate for long-term value creation. When properly modeled, governed, and governed ethically, CLV enables teams to shift from transactional quarterly mindsets to lifetime portfolios—transforming customers into true franchise assets.

For any organization aspiring to mature its performance, CLV is the next frontier. Not just a metric on a dashboard—but a strategic mechanism capable of aligning functions, informing capital allocation, shaping product trajectories, elevating brand meaning, and forging relationships that transcend a single transaction.

Term Sheets: Landmines and Ticking Time Bombs!

Wall Street is the only place that people ride to in a Rolls Royce to get advice from those who take the subway. – Warren Buffett

So the big day is here. You have evangelized your product across various circles and the good news is that a VC has stepped forward to invest in your company. So the hard work is all done! You can rest on your laurels, sign the term sheet that the VC has pushed across the table, and execute the sheet, trigger the stock purchase, voter and investor rights agreements, get the wire and you are up and running! Wait … sounds too good to be true, doesn’t it? And yes you are right! If only things were that easy. The devil is in the details. So let us go over some of the details that you need to watch out for.

1. First, term sheet does not trigger the wire. Signing a term sheet does not mean that the VC will invest in your company. The road is still long and treacherous. All the term sheet does is that it requires you to keep silent on the negotiations, and may even prevent you to shop the deal to anyone else. The key investment terms are laid out in the sheet and would be used in much greater detail when the stock purchase agreement, the investor rights agreement, the voting agreement and other documents are crafted.

2. Make sure that you have an attorney representing you. And more importantly, an attorney that has experience in the field and has reviewed a lot of such documents. As noted, the devil is in the details. A little “and” or “or” can put you back significantly. But it is just as important for you to know some of the key elements that govern an investment agreement. You can quiz your attorney on these because some of these are important enough to impact your operating degree of freedom in the company.The starting point of a term sheet is valuation of the company. You will hear the concept of pre-money valuation vs. post-money valuation. It is quite simple. The Pre-Money Valuation + Investment = Post-Money Valuation. In other words, Pre-money valuation refers to the value of a company not including external funding or the latest round of funding. Post-Money thus includes the pre-money plus the incremental injection of capital. Let us look at an example:

2. Make sure that you have an attorney representing you. And more importantly, an attorney that has experience in the field and has reviewed a lot of such documents. As noted, the devil is in the details. A little “and” or “or” can put you back significantly. But it is just as important for you to know some of the key elements that govern an investment agreement. You can quiz your attorney on these because some of these are important enough to impact your operating degree of freedom in the company.The starting point of a term sheet is valuation of the company. You will hear the concept of pre-money valuation vs. post-money valuation. It is quite simple. The Pre-Money Valuation + Investment = Post-Money Valuation. In other words, Pre-money valuation refers to the value of a company not including external funding or the latest round of funding. Post-Money thus includes the pre-money plus the incremental injection of capital. Let us look at an example:

Let’s explain the difference by using an example. Suppose that an investor is looking to invest in a start up. Both parties agree that the company is worth $1 million and the investor will put in $250,000.

The ownership percentages will depend on whether this is a $1 million pre-money or post-money valuation. If the $1 million valuation is pre-money, the company is valued at $1 million before the investment and after investment will be valued at $1.25 million. If the $1 million valuation takes into consideration the $250,000 investment, it is referred to as post-money. Thus in a pre-money valuation, the Investor owns 20%. Why? The total valuation is $1.25M which is $1M pre-money + $250K capital. So the math translates to $250K/$1,250K = 20%. If the investor says that they will value company $1M post-money, what they are saying is that they are actually giving you a pre-money valuation of $750K. In other words, they will own 25% of the company rather than 20%. Your ownership rights go down by 5% which, for all intents and purposes, is significant.

3. When a round of financing is done, security is exchanged in lieu of cash received. You already have common stock but these are not the securities being exchanged. The company would issue preferred stock. Preferred stock comes with certain rights, preferences, privileges and covenants. Compared to common stock, it is a superior security. There are a number of important rights and privileges that investors secure via a preferred stock purchase, including a right to a board seat, information rights, a right to participate in future rounds to protect their ownership percentage (called a pro-rata right), a right to purchase any common stock that might come onto the market (called a right of first refusal), a right to participate alongside any common stock that might get sold (called a co-sale right), and an adjustment in the purchase price to reflect sales of stock at lower prices (called an anti-dilution right). Let us examine this in greater detail now. There are two types of preferred. The regular vanilla Convertible Preferred and the Participating Preferred. As the latter name suggests, the Participating Preferred allows the VC to receive back their invested capital and the cumulative dividends, if any before common stockholders (that is you), but also enables them to participate on an as-converted basis in the returns to you, the common stockholder. Here is the math:Let us say company raises $3M at a $3M pre-money valuation. As mentioned before in point (3), the stake is 50%-50% owner-investor.

Let us say company sells for $25M. Now the investor has participating preferred or convertible preferred. How does the difference impact you, the stockholder or the founder. Here goes!

i. Participating Preferred. Investor gets their $3M back. There is still $22M left in the coffers. Investor splits 50-50 based on their participating preferred. You and Investor both take home $11M from the residual pool. Investor has $14M, and you have $11M. Congrats!

ii. Convertible Preferred. Investor gets 50% or $12.5M and you get the same – $12.5M. In other words, convertible preferred just got you a few more drinks at the bar. Hearty Congratulations!

Bear in mind that if the Exit Value is lower, the difference becomes more meaningful. Let us say exit was $10M. The Preferred participant gets $3M + $3.5M = $6.5M while you end up with $3.5M.

4. One of the key provisions is Liquidation Preferences. It can be a ticking time bomb. Careful! Some investors may sometimes ask for a multiple of their investment as a preference. This provision provides downside protection to investors. In the event of liquidation, the company has to pay back the capital injected for preferred. This would mean a 1X liquidation preference. However, you can have a 2X liquidation preference which means the investor will get back twice as much as what they injected. Most liquidation preferences range from 1X to 2X, although you can have higher liquidation preference multiples as well. However, bear in mind that this becomes important only when the company is forced to liquidate and sell of their assets. If all is gung-ho, this is a silent clause and no sweat off your brow.

4. One of the key provisions is Liquidation Preferences. It can be a ticking time bomb. Careful! Some investors may sometimes ask for a multiple of their investment as a preference. This provision provides downside protection to investors. In the event of liquidation, the company has to pay back the capital injected for preferred. This would mean a 1X liquidation preference. However, you can have a 2X liquidation preference which means the investor will get back twice as much as what they injected. Most liquidation preferences range from 1X to 2X, although you can have higher liquidation preference multiples as well. However, bear in mind that this becomes important only when the company is forced to liquidate and sell of their assets. If all is gung-ho, this is a silent clause and no sweat off your brow.

5. Redemption rights. The right of redemption is the right to demand under certain conditions that the company buys back its own shares from its investors at a fixed price. This right may be included to require a company to buy back its shares if there has not been an exit within a pre-determined period. Failure to redeem shares when requested might result in the investors gaining improved rights, such as enhanced voting rights.

6. The terms could demand that a certain option pool or a pot of stock is kept aside for existing and future employees, or other service providers. It could be a range anywhere between 10-20% of the total stock. When you reserve this pool, you are cutting into your ownership stake. In those instances when you have series of financings and each financing requires you to set aside a small pool, it dilutes you and your previous investors. In general, the way these pools are structured is to give you some headroom up to at least 24 months to accommodate employee growth and providing them incentives. The pool only becomes smaller with the passage of time.

7. Another term is the Anti-Dilution Provision. In its simplest form, anti-dilution rights are a zero- sum game. No one has an advantage over the other. However, this becomes important only when there is a down round. A down round basically means that the company is valued lower in subsequent financing than previously. A company valued at $25M in Series A and $15M in Series B – the Series B would be considered a down round. Two Types of Anti-Dilution:

Full ratchet Anti-Dilution: If the new stock is priced lower than prior stock, the early investor has a clause to convert their shares to the new price. For example, if prior investor paid $1.00 and then it was reset in a later round to $0.50, then the prior investors will have 2X rights to common stock. In other words, you are hit with major dilution as are the later investors. This clause is a big hurdle for new investors.

Weighted Average Anti-Dilution. Old investor’s share is adjusted in proportion to the dilution impact of a down round

8. Pay to Play. These are clauses that work in your, the Company, favor. Basically, investors have to invest some money in later financings, and if they do not – their rights may be reduced. However, having these clauses may put your mind at ease, but may create problems in terms of syndicating or getting investments. Some investors are reluctant to put their money in when there are pay to play clauses in the agreement.

9. Right of First Refusal. A company has no obligation to sell stock in future financing rounds to existing investors. Some investors would like to participate and may seek pro-rata participating to keep their ownership stake the same post-financing. Some investors may even want super pro-rata rights which means that they be allowed to participate to such an extent that their new ownership in the company is greater than their previous ownership stake.

10. Board of Directors. A large board creates complexity. Preferable to have a small but strategic board. New investors will require some representation. If too many investors request representation, the Company may have smaller internal representatives and may be outvoted on certain issues. Be aware of the dynamics of a mushrooming board!

11.Voting Rights. Investors may request certain veto authority or have rights to vote in favor of or against a corporate initiative. Company founders may want super-voting rights to exercise greater control. These matters are delicate and going one way or the other may cause personal issues among the participants. However, these matters can be easily resolved by essentially having carve-outs that spell out rights and encumbrances.

12.Drag Along Provision. Might create an obligation on all shareholders of the company to sell their shares to a potential purchaser if a certain percentage of the shareholders (or of a specific class of shareholders) votes to sell to that purchaser. Often in early rounds drag along rights can only be enforced with the consent of those holding at least a majority of the shares held by investors. These rights can be useful in the context of a sale where potential purchasers will want to acquire 100% of the shares of the company in order to avoid having responsibilities to minority shareholders after the acquisition. Many jurisdictions provide for such a process, usually when a third party has acquired at least 90% of the shares.

13.Representations and Warranties. Venture capital investors expect appropriate representations and warranties to be provided by key founders, management and the company. The primary purpose of the representations and warranties is to provide the investors with a complete and accurate understanding of the current condition of the company and its past history so that the investors can evaluate the risks of investing in the company prior to subscribing for their shares. The representations and warranties will typically cover areas such as the legal existence of the company (including all share capital details), the company’s financial statements, the business plan, asset ownership (in particular intellectual property rights), liabilities (contingent or otherwise), material contracts, employees and litigation. It is very rare that a company is in a perfect state. The warrantors have the opportunity to set out issues which ought to be brought to the attention of the new investors through a disclosure letter or schedule of exceptions. This is usually provided by the warrantors and discloses detailed information concerning any exceptions to or carve-outs from the representations and warranties. If a matter is referred to in the disclosure letter the investors are deemed to have notice of it and will not be able to claim for breach of warranty in respect of that matter. Investors expect those providing representations and warranties about the company to reimburse the investors for the diminution in share value attributable to the representations and warranties being inaccurate or if there are exceptions to them that have not been fully disclosed. There are usually limits to the exposure of the warrantors (i.e. a dollar cap on the amount that can be recovered from individual warrantors). These are matters for negotiation when documentation is being finalized. The limits may vary according to the severity of the breach, the size of the investment and the financial resources of the warrantors. The limits which typically apply to founders are lower than for the company itself (where the company limit will typically be the sum invested or that sum plus a minimum return).

14. Information Rights. In order for venture capital investors to monitor the condition of their investment, it is essential that the company provides them with certain regular updates concerning its financial condition and budgets, as well as a general right to visit the company and examine its books and records. This sometimes includes direct access to the company’s auditors and bankers. These contractually defined obligations typically include timely transmittal of annual financial statements (including audit requirements, if applicable), annual budgets, and audited monthly and quarterly financial statements.

15. Exit. Venture capital investors want to see a path from their investment in the company leading to an exit, most often in the form of a disposal of their shares following an IPO or by participating in a sale. Sometimes the threshold for a liquidity event or will be a qualified exit. If used, it will mean that a liquidity event will only occur, and conversion of preferred shares will only be compulsory, if an IPO falls within the definition of a qualified exit. A qualified exit is usually defined as a sale or IPO on a recognized investment exchange which, in either case, is of a certain value to ensure the investors get a minimum return on their investment. Consequently, investors usually require undertakings from the company and other shareholders that they will endeavor to achieve an appropriate share listing or trade sale within a limited period of time (typically anywhere between 3 and 7 years depending on the stage of investment and the maturity of the company). If such an exit is not achieved, investors often build in structures which will allow them to withdraw some or the entire amount of their investment.