Author Archives: Hindol Datta

Joseph Campbell, The Power of Myth, and the Art of Envisioning System Architecture

Joseph Campbell believed that mythology is not merely a collection of old stories; it is the human mind’s original operating system: a universal architecture that encodes how we understand change, complexity, and meaning. In The Power of Myth, his celebrated conversation with Bill Moyers ( I binged on this entire series this Saturday after a long while), Campbell argued that myths are “clues to the spiritual potentialities of human life.” Yet let’s read these myths more broadly. They are also models of systemic behavior, blueprints for how transformation unfolds, whether in an individual, an enterprise, or a technological ecosystem.

Modern system architecture, whether in finance, operations, or digital transformation, faces a challenge similar to that of mythology: to impose order without rigidity, to design for change without losing coherence, and to align many moving parts into a living, breathing whole. Seen through Campbell’s lens, architecture is not an engineering diagram but a hero’s journey in structure and function. It is a story of departure from legacy, confrontation with uncertainty, and eventual return with renewal and insight.

This essay examines how Campbell’s mythic framework can guide the way we envision and construct systems. It explores myth as the original design language, shows how the Hero’s Journey mirrors architectural transformation, and offers a practical synthesis for leaders designing resilient, meaningful, and adaptive systems.

I. Myth as the Blueprint of Human Systems

Campbell’s insight begins with a profound observation: across all civilizations, the same basic pattern repeats. Whether one reads the Odyssey, the Bhagavad Gita, or Star Wars, the storyline follows a universal topology which he calls the monomyth. The hero is called to adventure, crosses a threshold into the unknown, undergoes trials and transformation, and returns with an “elixir” that restores the community.

This pattern is not confined to literature. It is embedded in the human experience of transformation itself. Every system, be it biological, social, or organizational, must at times break its equilibrium, traverse chaos, and re-emerge at a higher level of order. Myth thus becomes the architecture of change.

In modern terms, one could call it a recursive algorithm: a self-similar process that repeats at different scales. Each subsystem, individual team, department, or platform undergoes its own hero’s journey within the larger enterprise narrative. The organization evolves as these micro-journeys interact, merge, and reinforce each other.

This recursive layering of journeys parallels how system architects think. They model modules, interfaces, and flows. Bear in mind that each operates with local autonomy while maintaining global coherence. The aim is to create a structure in which each part serves both its own function and the integrity of the whole. Myth, in essence, is the human mind’s first architecture diagram. It shows that enduring systems are not built from control alone, but from patterns of interaction guided by purpose.

II. The Hero’s Journey as a Systemic Map

To see how Campbell’s mythic model translates into architectural thinking, it helps to map the significant phases of the Hero’s Journey onto the process of system design and transformation.

1. Departure – The Call to Transformation

In the mythic narrative, the hero receives a call to adventure that disturbs the stability of the familiar world. There is usually resistance, hesitation, or denial. Similarly, in system design, the first step is to acknowledge that the current state—legacy infrastructure, static reporting, siloed processes—can no longer support the enterprise’s evolving goals.

The “call to adventure” in this context might be a strategic imperative: the need for automation, scalability, or predictive insight. Yet just as in mythology, departure demands courage. Organizations cling to legacy environments because they are stable and known. The departure phase requires both leadership and faith that what lies beyond the threshold, though uncertain, holds greater value.

In architectural terms, this is the moment of disruption: namely, when the system is deliberately unsettled so that it may evolve. It is the point at which a decision is made to move from existing architectures to adaptive, modular ones, often involving distributed systems, advanced analytics, or artificial intelligence.

2. Initiation – The Trials of Integration

The initiation phase in myth is the crucible, a period of trials, tests, and revelations. Heroes encounter helpers and enemies, face ordeals, and undergo symbolic death and rebirth. In a system architecture, this is the transformation stage, where integration, design, and implementation converge.

Architects at this stage must navigate a complex landscape: data pipelines, governance models, user adoption, and competing design philosophies. Conflicts arise between speed and control, between local autonomy and global standardization, between innovation and compliance. These are the dragons of modern enterprise.

The successful architect, like the mythic hero, learns to balance forces rather than eliminate them. Campbell called this the “coincidence of opposites”: the ability to hold dualities in creative tension. In system terms, this means designing with trade-offs in mind. One must weigh the time-space balance of computation (pre-aggregated versus real-time), the entropy of data models (flexibility versus discipline), and the complexity of governance (centralization versus decentralization).

The most powerful systems emerge not from perfect control but from simple rules that enable emergence. This aligns with complexity theory and with leadership models that empower decision-making at the edge. Just as the hero must rely on intuition and allies, architects must rely on principles rather than micromanagement. When simple, clear standards such as data schema conventions or API contracts are consistently enforced, teams can innovate within shared boundaries.

The initiation phase is therefore not a linear build but a living negotiation of a dance between structure and spontaneity, design and discovery.

3. Return – The Elixir of Integration

In Campbell’s framework, the hero’s return is not merely homecoming but integration. The hero brings back the “boon” which I think of as a gift of insight, knowledge, or capability that renews the community. The journey is complete only when this new wisdom is assimilated into ordinary life.

In architecture, this is the post-deployment phase: the system becomes operational, knowledge is institutionalized, and the organization experiences measurable improvement. Yet return is often underestimated. Many transformation efforts fail not in design but in integration. It is the inability to embed new capabilities into the daily rhythm.

For the architect, therefore, the return phase requires a self-sustaining design, a system that continues to evolve without heroic intervention. It must include feedback loops, performance metrics, and maintenance protocols that act as the organizational immune system. This is the modern equivalent of the mythic “elixir”: a living capability that strengthens the enterprise against future entropy.

When the system achieves this equilibrium, it ceases to be a project and becomes part of the organism’s identity. In mythic terms, the hero becomes king, sage, or teacher or if I may call it the new custodian of order.

III. The Mythic Mindset for System Architects

Campbell once said that myth reveals “what it means to be alive.” In the same way, a well-designed architecture reveals what it means for an organization to live and evolve. Both operate through pattern recognition, which is the ability to discern structure within chaos.

For a system architect or a finance executive overseeing transformation, adopting a mythic mindset provides several advantages.

1. Framing Transformation as a Narrative

Data flows and process diagrams rarely inspire people, but stories do. A transformation project framed as a hero’s journey resonates deeply: there is a clear beginning, a quest, obstacles, and a collective triumph. When teams understand the “why” behind change in narrative terms, resistance decreases and participation increases.

Instead of abstract technical objectives, the story might read: We are leaving behind outdated systems to seek a single source of truth. We will face integration challenges, but we will return with a platform that empowers every team to see the business clearly. This narrative coherence can align stakeholders more effectively than a dozen technical presentations.

2. Recognizing the Role of Threshold Guardians

In myth, every hero meets gatekeepers—figures who test their worthiness to enter the unknown. In organizations, these constraints include compliance requirements, data security mandates, and resource limitations. They are not enemies but necessary filters that preserve integrity. Recognizing them as part of the journey, not obstacles to it, transforms frustration into design wisdom.

3. Building for Adaptation, Not Perfection

Myths survive because they evolve. Each retelling adapts to a new context while preserving core patterns. System architecture must do the same. Designing for adaptability means embracing modularity, reusability, and continuous learning. The goal is not a flawless system but a resilient structure that can absorb change without collapsing.

4. Controlling Entropy Through Meaningful Standards

Campbell often spoke of the mythic hero’s task to bring order to chaos. In systems, chaos appears as entropy, and that is none other than data drift, process decay, or the uncontrolled proliferation of tools. The counterforce is the creation of durable “moats”: documentation, automation, standardized controls, and governance frameworks that maintain order without suffocating flexibility.

Entropy cannot be eliminated; it must be managed through renewal. Just as myths are periodically reinterpreted to stay alive, systems must be periodically refactored and retrained to remain relevant.

IV. The Architecture of Return: Sustaining Renewal

The power of Campbell’s model lies not in its sequence but in its cyclicality. The end of one journey becomes the beginning of another. Each return sows the seeds for a new departure. In systemic terms, this is the principle of continuous improvement. You have already read a few of my essays on feedback loops. Continuous Improvement is the ongoing feedback loop that transforms learning into capability.

A healthy architecture therefore, embodies the following qualities:

- Transparency: Every component knows how it connects to the whole.

- Traceability: Decisions and data can be followed back to their origins.

- Feedback: Systems collect information about their own performance.

- Redundancy: Critical functions are protected through diversity of design.

- Evolution: Components can be upgraded or replaced without destabilizing the core.

These qualities echo biological systems and myths alike. Both persist not through rigidity but through structured adaptability.

When leadership fosters the mindset of viewing every change as part of an ongoing journey rather than a discrete project, then inevitably the transformation becomes cultural rather than episodic. The system itself develops narrative intelligence: an awareness of its own history, purpose, and trajectory.

V. The Meeting of Myth and Mathematics

The connection between mythology and system design might appear poetic, but it rests on a logical foundation. Campbell’s framework of transformation parallels the logic of complex adaptive systems, information theory, and control dynamics.

When a system departs from equilibrium, it enters a state of increased entropy. Through feedback and adaptation, it reorganizes into a higher level of complexity. This process mirrors the mythic initiation: chaos followed by renewal.

Turing’s concepts of time-space trade-offs apply here as well. Every system must balance computation time against storage space; every organization must balance speed of change against depth of structure. The mythic hero faces the same trade-off—venturing quickly risks failure, but hesitation costs opportunity.

Von Neumann’s idea of self-replication in systems echoes Campbell’s notion of mythic renewal: patterns that reproduce themselves across generations, adapting but never losing identity. Both imply that enduring design depends on self-similarity, which is a rule simple enough to be inherited and flexible enough to evolve.

Thus, mythology and system architecture share a mathematical symmetry: both translate chaos into pattern and time into structure.

VI. The Practical Framework: A Mythic Checklist for Architects

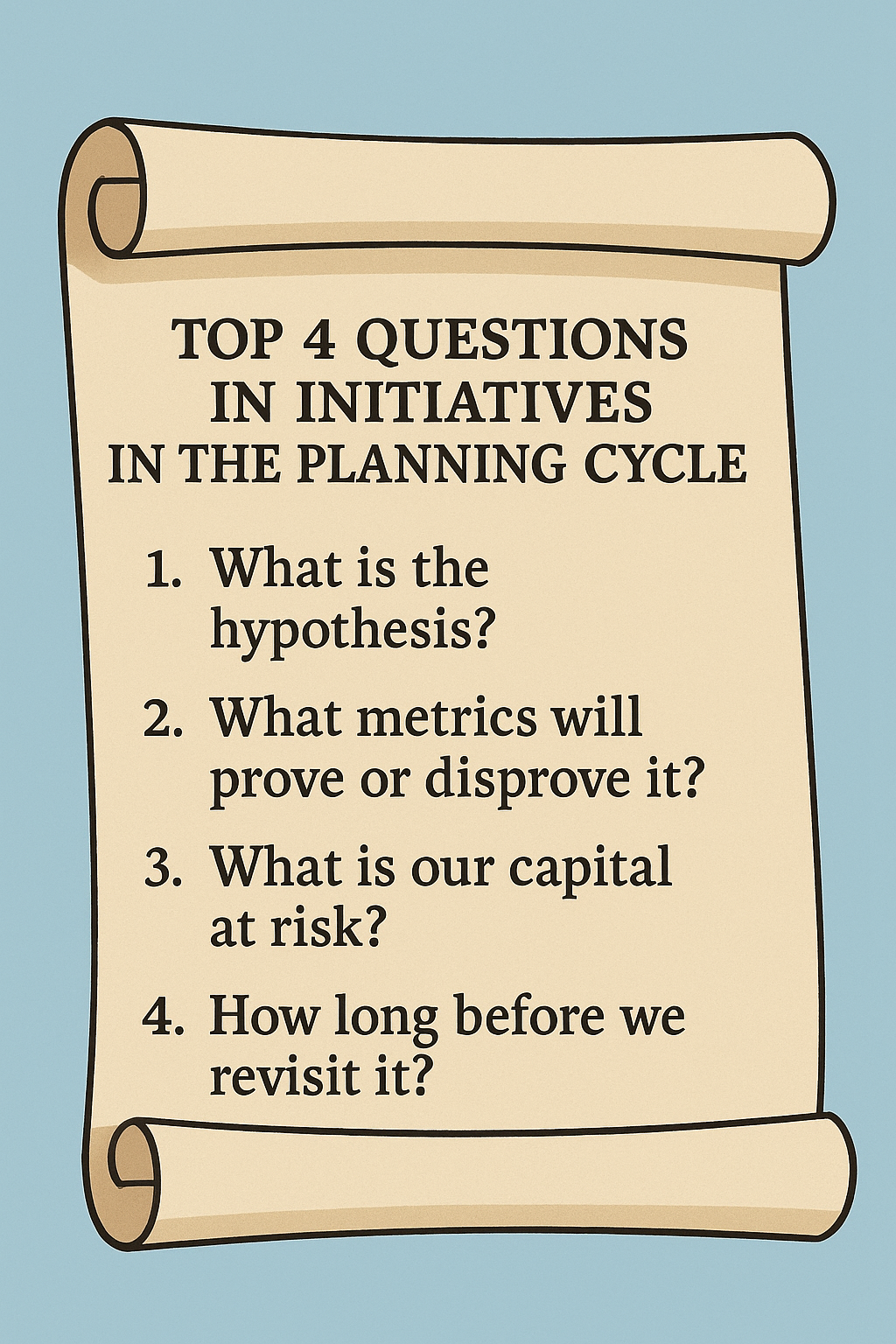

To translate these ideas into practice, one can structure any major architectural initiative around a mythic framework:

- Call to Adventure: Identify the disruption or opportunity demanding change. Define why the current architecture must evolve.

- Crossing the Threshold: Establish guiding principles and governance. Recognize what risks and constraints must be respected.

- Tests and Trials: Confront integration challenges, data quality issues, and cultural resistance. Allow small failures to inform larger design choices.

- Allies and Mentors: Engage cross-functional teams, experts, and governance bodies as supporting archetypes.

- The Abyss: Confront the hardest problem—the one that threatens to derail progress. Often this is not technical but human: lack of trust, clarity, or alignment.

- Revelation and Transformation: Discover the new design paradigm—simpler, modular, and resilient. Institutionalize the insight through documentation and standards.

- Return with the Elixir: Deliver measurable value—reduced cost, improved insight, faster decisions—and embed the capability into the organization’s rhythm.

- Guardians of the Moat: Establish controls and feedback loops to preserve integrity against entropy.

- Cycle of Renewal: Use metrics and retrospectives to begin the next improvement journey.

This framework is as much about psychology as it is about technology. It ensures that every stakeholder sees the architecture not as a static deliverable but as a living system, perpetually evolving toward greater coherence and value.

VII. The Leader as Architect and Storyteller

The most effective system architects and financial leaders are not just process engineers; they are storytellers of transformation. They understand that structure without story becomes sterile, while story without structure becomes chaos.

Campbell’s enduring message was that myths reveal the shared patterns of human striving. The architect’s task is similar: to design systems that honor those patterns—systems that empower, clarify, and sustain.

When a leader presents a transformation as a narrative, people locate themselves within it. They understand their role in the larger pattern. The architecture ceases to be an abstraction; it becomes a collective journey.

VIII. The Power of Myth in the Age of Systems

Today’s organizations operate in a constant state of flux and are drowning in data proliferation, algorithmic decision-making, and distributed intelligence. The temptation is to manage this complexity through control. Yet as both Campbell and complexity theorists remind us, true order arises not from rigidity but from the right balance between structure and freedom.

A mythic approach invites humility. It acknowledges that no single designer can foresee all interactions within a living system. Instead, the architect sets conditions for emergence by defining simple, consistent principles and trusting the system to self-organize.

This mindset transforms the role of the modern executive. The leader becomes less a commander and more a gardener, cultivating conditions where coherence can emerge naturally. The hero’s journey becomes not the story of one individual but the collective saga of a learning organization.

IX. The Enduring Lesson

Campbell wrote that the purpose of the hero’s journey is not the triumph of the individual but the renewal of the community. The same is true of every architectural transformation. The goal is not the perfection of a platform but the evolution of the enterprise’s capacity to learn, adapt, and thrive.

When systems are designed with this principle in mind, they become more than tools; they become living frameworks of intelligence and purpose. They reflect not only the logic of technology but the logic of life itself.

Just as myths endure because they embody the deep grammar of human meaning, great architecture endures because it represents the deep grammar of systemic integrity. Both must balance chaos and order, change and continuity, freedom and discipline.

In the end, the most elegant architecture, like the most enduring myth, is one that transcends its designer. It continues to evolve, teaching new generations how to navigate uncertainty and find coherence amid change.

To envision architecture through Joseph Campbell’s eyes is to recognize that our systems are not merely mechanical, but they are mythic. It is the expressions of our collective will to bring order to chaos, meaning to data, and story to structure. When we build with that awareness, we design not only for efficiency but for resilience, not only for output but for renewal.

We create systems that, like the great myths, stand the test of time because they speak to something universal: the perpetual journey of transformation, return, and rebirth that defines both humanity and the organizations we build.

Transforming Finance: From ERP to Real-Time Decision Making

There was a time when the role of the CFO could be summarized with a handful of verbs: report, reconcile, allocate, forecast. In the 20th century, the finance office was a bastion of structure and control. The CFO was the high priest of compliance and the gatekeeper of capital. The systems were linear, the rhythms were quarterly, and the decisions were based on historical truths.

That era has passed. In its place emerges the Digital CFO 3.0 – a new kind of enterprise leader who moves beyond control towers and static spreadsheets to architect digital infrastructure, orchestrate intelligent systems, and enable predictive, adaptive, and real-time decision-making across the enterprise.

This is not a change in tools. It is a change in mindset, muscle, and mandate.

The Digital CFO 3.0 is not just a steward of financial truth. They are a strategic systems architect, a data supply chain engineer, and a design thinker for the cognitive enterprise. Their domain now includes APIs, cloud data lakes, process automation, AI-enabled forecasting, and trust-layer governance models. They must reimagine the finance function not as a back-office cost center, but as the neural core of a learning organization.

Let us explore the core principles, capabilities, and operating architecture that define this new role, and how today’s finance leaders must prepare to build the infrastructure of the future enterprise.

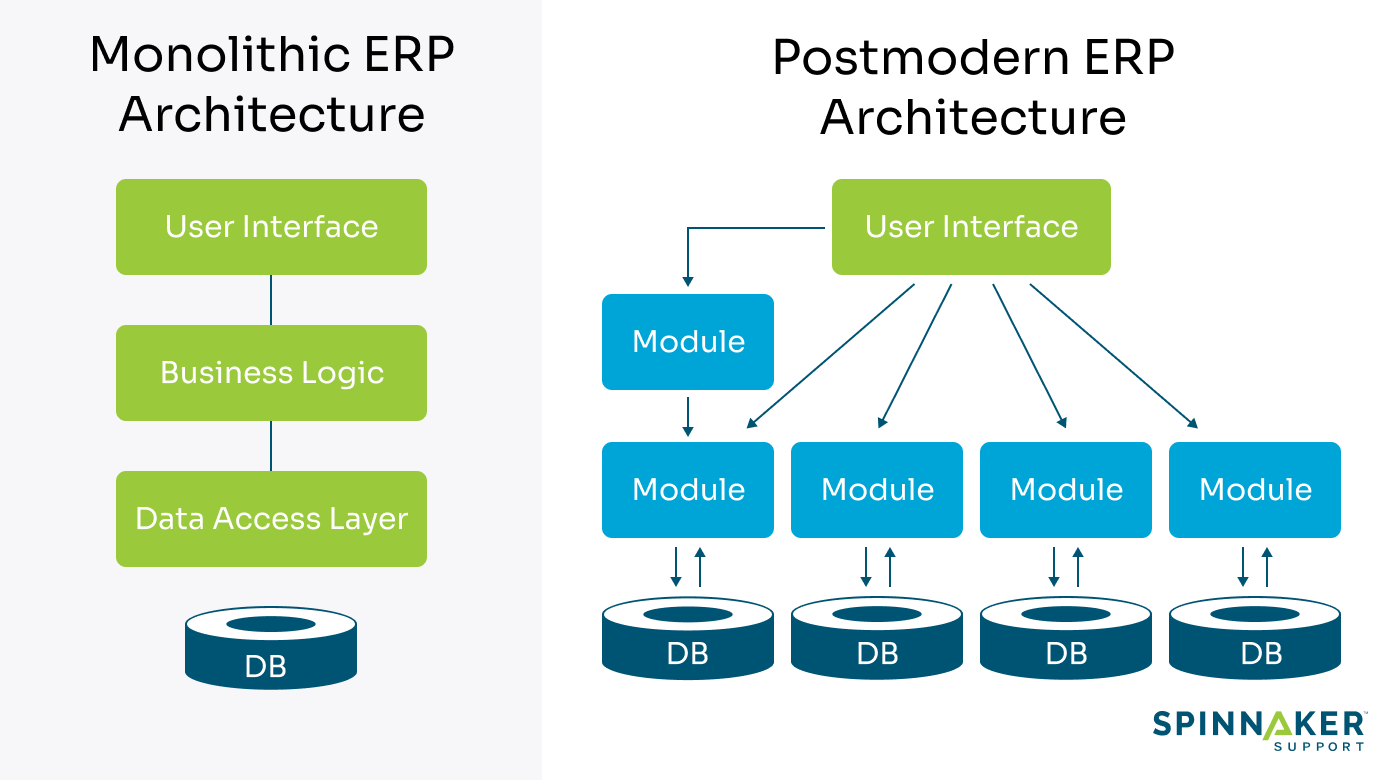

1. From Monolithic ERP to Modular Intelligence

Traditional finance infrastructure was built on monolithic ERP systems – massive, integrated, but inflexible. Every upgrade was painful. Data latency was high. Insight was slow.

The Digital CFO 3.0 shifts toward a modular, composable architecture. Finance tools are API-connected, event-driven, and cloud-native. Data moves in real time through finance operations, from procure-to-pay to order-to-cash.

- Core systems remain but are surrounded by microservices for specific tasks: forecasting, scenario modeling, spend analytics, compliance monitoring.

- Data lakes and warehouses serve as integration layers, decoupling applications from reporting.

- AI and ML modules plug into these environments to generate insights on demand.

This architecture enables agility. New use cases can be spun up quickly. Forecasting models can be retrained in hours, not months. Finance becomes a responsive, intelligent grid rather than a transactional pipe.

2. Finance as a Real-Time Operating System

In legacy models, finance operated in batch mode: monthly closes, quarterly forecasts, annual planning. But the modern enterprise operates in real time. Markets shift hourly. Customer behavior changes daily. Capital decisions must respond accordingly.

The Digital CFO builds a real-time finance engine:

- Continuous Close: Transactions are reconciled daily, not monthly. Variances are flagged immediately. The books are always nearly closed.

- Rolling Forecasting: Plans update with each new signal – not by calendar, but by context.

- Embedded Analytics: Metrics travel with the business – inside CRM, procurement, inventory, and workforce systems.

- Streaming KPIs: Finance watches the enterprise like a heart monitor, not a photograph.

This changes how decisions are made. Instead of waiting for reports, leaders ask questions in the flow of business – and get answers in seconds.

3. Trust by Design: The New Governance Layer

As data velocity increases, so does the risk of error, bias, and misinterpretation. The CFO has always been a guardian of trust. But for the Digital CFO 3.0, this mandate extends to the digital trust layer:

- Data Lineage: Every number is traceable. Every transformation is logged.

- Model Governance: AI models used in finance must be explainable, auditable, and ethical.

- Access Control: Fine-grained permissions ensure only the right people see the right numbers.

- Validation Rules: Embedded in pipelines to flag anomalies before they reach the dashboard.

Trust is not a byproduct of strong reporting. It is an outcome of intentional design.

4. Orchestrating the Intelligent Workflow

In the digital enterprise, no team operates in isolation. Sales, operations, procurement, HR are interconnected. The Digital CFO 3.0 builds infrastructure to orchestrate intelligent workflows across silos.

- AP automation connects with vendor portals and treasury systems.

- Forecast adjustments trigger alerts to sourcing and demand planning teams.

- Employee cost changes ripple through headcount plans and productivity dashboards.

This orchestration requires more than software. It demands process choreography and data interoperability. The CFO becomes the conductor of a distributed, dynamic finance system.

5. Redesigning Talent for a Cognitive Finance Team

Digital infrastructure is only as powerful as the team that runs it. The finance org of the future looks different:

- Analysts become insight designers, curating stories from signals.

- Controllers become data quality stewards.

- FP&A teams become simulation strategists.

- Finance business partners become embedded value engineers.

The Digital CFO invests in technical fluency, data storytelling, and systems thinking. Upskilling is continuous. Learning velocity becomes a core KPI.

6. From Reporting the Past to Architecting the Future

Ultimately, the Digital CFO 3.0 is not building systems to describe yesterday. They are designing infrastructure to anticipate tomorrow:

- Capex investments are modeled across geopolitical scenarios.

- ESG metrics are embedded into supplier scoring and budget cycles.

- Strategic choices are evaluated with real option models and probabilistic simulations.

- M&A integration plans are automated, with finance playbooks triggered by transaction type.

The finance function becomes a predictive nerve center, informing everything from product pricing to market entry.

Conclusion: The CFO as Enterprise Architect

The shift to Digital CFO 2.0 is not optional. It is inevitable. Markets are faster. Technology is smarter. Stakeholders expect more. What was once a support function is now a strategic command center.

This is not about buying tools. It is about designing an operating system for the enterprise that is intelligent, adaptive, and deeply aligned with value creation.

The future CFO does not just report results. They engineer outcomes. They do not just forecast growth. They architect the infrastructure to make it happen.

CFOs as Venture Capitalists: Rethinking ERP Strategies

Most CFOs view their ERP systems the way civil engineers view bridges—vital, expensive, and terrifying to replace. They are the arteries of the enterprise, moving data and dollars across finance and operations. Yet, despite all the cost and effort, most ERPs underperform their potential.

The reason is not lack of functionality—it is lack of imagination.

After leading multiple ERP transformations—from NetSuite and Sage and BaaN MRP implementations to a global rollout of Oracle Financials integrated with Hyperion and MicroStrategy, I have come to believe that the real return on ERP investment lies not in the code, but in the design philosophy.

It is time CFOs started thinking like venture capitalists and systems engineers.

From Infrastructure to Investment Portfolio

Traditional ERP thinking is defensive: avoid disruption, close the books, ensure compliance. It is the financial equivalent of playing not to lose.

But a venture capitalist asks a different question: where is the next multiple coming from?

We can treat ERP initiatives the same way—segmenting them into:

- Core Maintenance: compliance, upgrades, and security.

- Leverage Plays: automation, reporting, and workflow redesign.

- Optionality Bets: AI-powered forecasting, agentic automation, and embedded analytics.

This portfolio mindset ensures capital is allocated to where it generates the most operational leverage, not where it merely reduces anxiety.

The Power of Horizontal Thinking

Most ERP failures are not technical – they are architectural. Companies build vertical silos: Finance here, Procurement there, HR in another system. Each one optimized locally but misaligned globally.

The future belongs to horizontal, workstream-focused systems—built around flows like Order-to-Cash, Procure-to-Pay, and Record-to-Report.

Why does this matter? Because workstreams are where value flows. That is where automation compounds, latency disappears, and teams feel the impact of technology.

When I oversaw our Oracle-Hyperion-MicroStrategy global rollout, the biggest unlock did not come from adding modules. It came from aligning processes horizontally—so that planning, consolidation, and analytics spoke the same language. That is when the ERP stopped being a ledger and started being an intelligence engine.

Why Modularity Enables Agentic AI

Horizontal ERPs are, by nature, modular. Each component—finance, procurement, analytics—interacts through clean APIs and governed data layers. This modularity is exactly what Agentic AI systems need to thrive.

AI agents are not magic—they are orchestration tools. They need consistent structures, good metadata, and systems that can “talk” to each other. A modular ERP built on sound governance becomes the perfect substrate for AI copilots that can:

- Reconcile accounts automatically,

- Trigger proactive alerts for anomalies,

- Forecast cash flow in real time, and

- Suggest workflow optimizations based on patterns.

When the ERP is monolithic, AI is decorative. When it is modular, AI becomes multiplicative.

Designing for Hidden ROI

The hidden ROI zones are everywhere once you start looking:

- Process Acceleration – Automating intercompany eliminations or close cycles.

- Data Visibility – Converting stale reports into live dashboards.

- Workflow Integration – Syncing ERP with CRM, HRIS, and procurement to eliminate handoffs.

Each enhancement may look small, but compounded across a finance organization, they can save thousands of hours per year.

That is how venture thinking turns into financial engineering.

Metrics Boards Actually Care About

We do not measure ERP ROI in “go-live” dates anymore. We measure it in:

- Days to close,

- Time to insight,

- Cost per transaction, and

- Productivity per finance FTE.

These are tangible, board-level metrics that link system efficiency directly to enterprise value.

Governance: The Unsung Hero

The best ERPs die slowly—not from bugs, but from bloat. Over-customization, consultant dependence, and poor data hygiene suffocate agility.

Good governance means lean design, modular rollouts, transparent contracts, and internal ownership. It is less glamorous than AI, but without it, innovation becomes entropy.

Final Word: ERP as a Competitive Advantage

ERPs are not going away: they are the spine of the enterprise. But we can make them smarter, faster, and more horizontal.

When designed with modularity, governed with discipline, and infused with agentic intelligence, the ERP evolves from a cost center into a compounding asset.

The CFO who thinks like a venture capitalist and designs like a systems architect will find that the next great ROI story is already sitting inside the general ledger waiting to be unlocked.

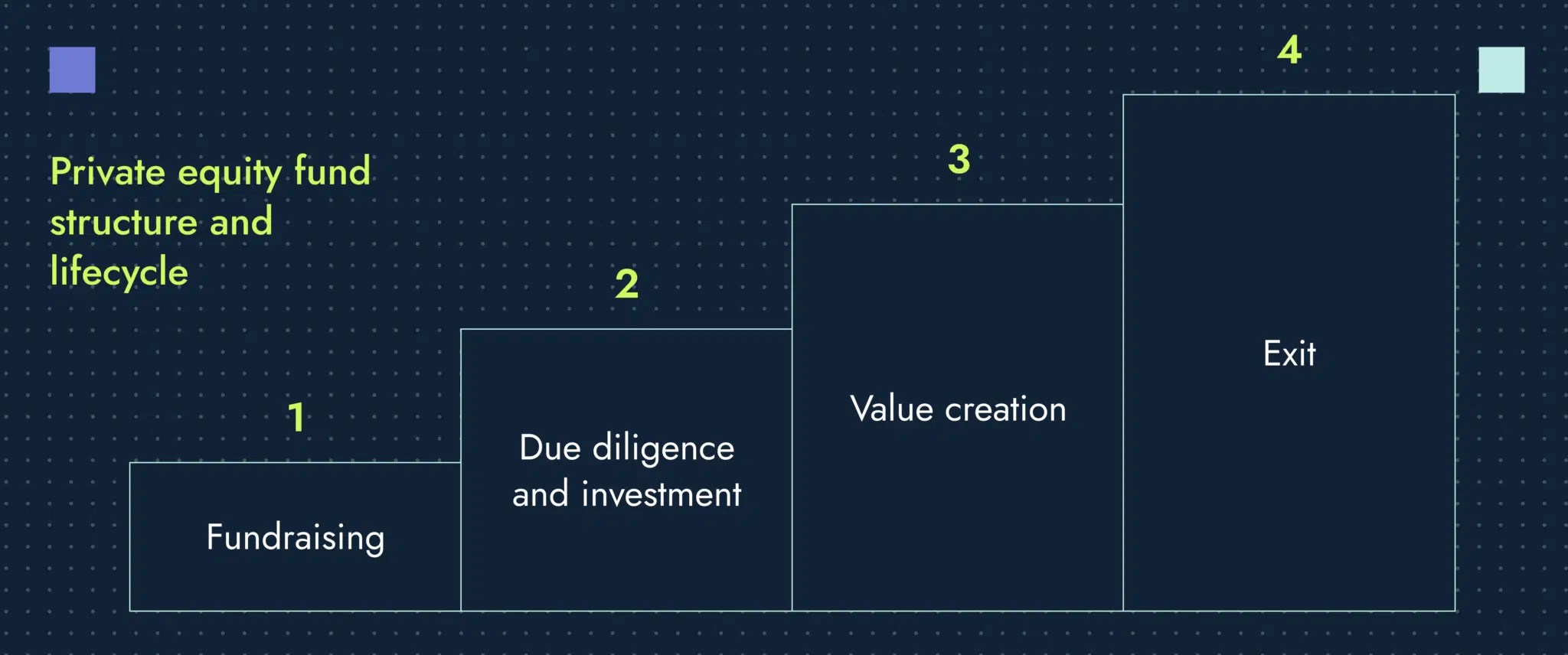

Building Value in Private Equity: A Story of Growth and Time

The Big Idea

Some people think value is something you find like treasure hidden in a cave. But in private equity, value is not found. It is built. It grows the way cities, trees, or living systems grow—by following simple rules, adapting to change, and using energy wisely.

As Geoffrey West explains in Scale, all living and business systems follow patterns of growth and decay. A private equity investment is no different. It begins with a spark of belief, grows through learning and adjustment, and must fight against the natural pull of entropy which is the quiet slide toward disorder.

Building value is not about being clever once. It is about staying disciplined over time.

1. The Beginning: Choosing with Care

Before an investor buys a company, they face the most challenging question: What will be different because we own it?

In this stage, we do not just look at spreadsheets. We ask questions about people, processes, and potential. We look for “scaling rules”—places where minor improvements can multiply results. A good investor studies the system the way a biologist studies an ecosystem. Every number in the model connects to behavior, incentives, and feedback. You cannot fix what you don’t understand.

As someone who has spent decades in finance and operations, I have learned that the best deals start not with excitement, but with honesty. Ask challenging questions before signing the check. Anything you ignore before buying will hurt you later.

2. The First Hundred Days: From Paper to People

Once the deal closes, the real work begins. The first hundred days are like the early growth phase of a city or an organism which is where rhythm, energy, and culture take shape.

The key is not speed, but sequencing. Move too fast, and the organization breaks. Move too slowly, and energy fades. Early wins matter, but trust matters more.

The plan must be simple enough for everyone to understand. I often remind teams: “If the warehouse manager and the sales lead cannot explain the strategy in one sentence, it is not ready.”

As in complex systems, feedback loops keep things healthy. Weekly check-ins, small data dashboards, and short decision cycles build transparency. Trust is the oxygen of transformation—without it, even good plans suffocate.

3. The Middle Years: Fighting Entropy

Every growing system eventually slows down. In cities, it shows up as traffic jams. In companies, it appears as missed deadlines, tired teams, and too many reports.

This is entropy which is the quiet drift toward disorder. You cannot eliminate it, but you can manage it.

The middle years of a private equity investment test the investor’s patience. It is no longer about ideas; it is about maintenance. Which projects still matter? Which metrics still measure the right things? Which leaders are ready for the next phase?

I have seen this pattern repeatedly: the companies that survive entropy are the ones that stay curious. They ask, “Is this still working?” and “What signal are we missing?” Complexity thinking reminds us—adaptation, not rigidity, creates resilience.

4. The Exit: Leaving Gracefully

Exiting an investment is like a scientist passing their experiment to the next researcher. The goal is not to make it perfect; it is to make it understandable and repeatable.

A great exit story is clear and accurate. It does not hide mistakes; it shows learning. Buyers pay a premium for systems they can trust. That means clean data, steady teams, and a clear narrative of progress.

In my own career, the best exits were not the flashiest; they were the ones where the company kept growing long after we left. That is when you know value was built, not borrowed.

Leaving well is an act of leadership. It requires detachment and pride in what’s been created. The company should no longer depend on you. Like a child leaving home, it should stand on its own.

5. The Bigger Picture: Value as a Living System

When I read Geoffrey West’s work, I saw private equity through a new lens. A company is a living system—it consumes energy (capital), grows through networks (people and information), and produces entropy (waste and drift).

The investor’s job is to keep the system alive long enough for it to evolve into something more substantial. That means designing feedback loops, respecting natural limits, and recognizing that scaling is not just about getting bigger, but it is also about getting smarter.

Complexity Theory teaches that order and chaos are partners. Growth always produces tension. The best investors, like good scientists, don’t try to control every variable. They design simple rules and let self-organization take care of the rest.

Final Thoughts

Private equity is really about time—how we use it, manage it, and give it shape. Each phase of the lifecycle tests a different kind of intelligence:

- Imagination at the start

- Discipline in the first hundred days

- Resilience in the middle years

- Clarity at exit

Actual value creation is not about squeezing numbers. It is about building systems that keep learning.

When capital meets curiosity, when plans meet patience, and when leadership meets humility—companies don’t just grow, they evolve.

That is the art of private equity. It is about system building and transformation.

The Rise of AI Agents in Enterprise Architecture

Explores the blueprint for how AI agents will eventually become a layer of the enterprise stack, including roles, hierarchies, and error loops.

From Automation to Autonomy: The Next Enterprise Layer

In three decades of working with companies across SaaS, freight logistics, edtech, nonprofit, and professional IT services, I have seen firsthand how every operational breakthrough begins with a design choice. Early ERP implementations promised visibility. Cloud migration promised scale. Now, we enter a new phase where enterprises don’t just automate processes; they delegate judgment. The rise of autonomous AI agents, which are decision-making systems embedded within workflows, is forcing companies to confront a fundamental question: What does a self-steering enterprise look like?

We are not talking about automation in the narrow sense of bots that click, sort, and file. We are referring to multi-agent systems that are autonomous entities trained to reason, escalate, and learn, and are embedded in revenue operations, compliance, finance, procurement, and even customer interaction. These agents do not merely follow logic trees. They operate with context. They perform functions that once required analysts, managers, and operations leads. They make decisions on your behalf.

The implications for enterprise design are profound. An architecture where humans and agents coexist must solve for hierarchy, interoperability, accountability, and trust. The autonomous enterprise will not emerge by stitching tools together. It will require a blueprint: a reimagination of systems, roles, and error recovery.

The AI Agent Stack: A New Operating System for Business

Just as companies once layered CRM on top of sales, or HRIS over people operations, we are now entering an era where AI agents form a cognitive layer across the enterprise. This layer does not replace ERP, CRM, or BI tools, but it orchestrates them.

In a Series C logistics company, the technology partner deployed a multi-agent system that monitored shipping costs, demand volatility, and SLA compliance. One agent forecasted volume. Another recommended pricing change. A third adjusted partner allocations based on reliability scores. None of these agents was isolated. They coordinated, negotiated, and escalated.

This layered system, what I now call the autonomous stack, includes four key components:

- Task Agents – Specialized agents designed for discrete workflows (forecasting, invoice reconciliation, contract flagging).

- Orchestration Agents – Meta-level agents that manage workflows across task agents, sequence dependencies, and ensure prioritization.

- Governance Agents – Watchdog systems that track agent behavior, decision logs, exception rates, and escalation patterns.

- Interface Agents – Agents that serve as the human-agent bridge, summarizing decisions, flagging anomalies, and allowing overrides.

The success of this architecture depends not just on model quality, but on how these agents interact, escalate, and recover. This is the true challenge of enterprise AI. Coordination, not capability, defines success.

Redefining Roles: From Managers to Model Supervisors

With agents taking over operational workflows, human roles must shift. The manager of tomorrow is not a task assigner. They are model supervisors: individuals who monitor agent behavior, fine-tune training data, review decision logs, and serve as an escalation point for unresolved ambiguities.

In a professional services firm, the CIO’s team deployed a time entry validation agent that cross-checked submitted hours against project charters and budget thresholds. Initially, the agent raised too many false flags. The team assigned a “controller”, a person trained in prompt design, logic validation, and pattern review. Within weeks, the number of false positives dropped by 60 percent. The agent learned. The controller’s role evolved into AI stewardship.

This is not a theoretical role. It is a design imperative. Every agent requires a human fallback path, a named individual or team who owns the domain, monitors behavior, and retrains the system when edge cases emerge.

Escalation Logic: Designing for Ambiguity

Autonomous systems thrive in structured environments. But ambiguity is a feature of enterprise life. A PO with mismatched terms, a billing dispute, a policy exception: all trigger the need for escalation. The best autonomous architecture does not suppress ambiguity. They design for it.

Each agent must be given confidence thresholds. When the confidence falls below a defined level, the agent escalates to a human, not with a question, but with a case file: data, context, options, and likely outcomes. The human then resolves and returns the resolution, which becomes new training data.

In an edtech firm, a finance agent reviews vendor payments. When faced with ambiguous tax classifications, it did not guess. It flagged the issue, explained the decision gap, and requested a policy update. Over time, this feedback loop reduced exception rates while improving policy precision.

Escalation is not a failure mode. It is a learning mode. When embedded into architecture, it becomes a source of resilience.

Trust and Transparency: Making the Invisible Visible

The most significant barrier to adoption in autonomous systems is not performance. It is opacity. Boards, CFOs, legal counsel, and frontline employees all ask the same question: How did the agent arrive at that decision?

The answer lies in decision traceability. Every autonomous agent must produce a log: inputs, model pathway, thresholds met, policies triggered, and the final action taken. These logs are not just for compliance; instead, they are for confidence.

In a compliance-heavy nonprofit, the autonomous grant review agent produced a “decision card” for every action. It listed the logic, risk flags, and supporting data. Reviewers could override or approve with a click. This created a culture of collaboration between humans and agents, not dependency or distrust.

Transparency is not a UI feature. It is an architectural principle. Trust compounds when systems explain themselves.

Error Loops and Systemic Recovery

All systems fail. The question is whether they recover intelligently. In autonomous enterprises, we must distinguish between local errors (a single agent failing to complete a task) and systemic errors (a cascade triggered by flawed agent assumptions).

This requires two safeguards:

- Autonomous monitoring agents – Designed to spot pattern anomalies, such as sudden drops in forecast accuracy or an increase in override frequency.

- Incident response playbooks – Predefined recovery paths that define when to roll back, retrain, or override models across the stack.

In a Series D SaaS company, a pricing optimization agent triggered an unexpected churn spike in a low-volume segment. The governance agent flagged an anomaly. The system auto-escalated. Human supervisors reviewed the pattern, adjusted the weighting of recent data, and retrained the model. The system self-healed within 48 hours. That agility is only possible when recovery is designed in advance.

Hierarchies of Intelligence: Flat Structure, Layered Control

Autonomous agents do not require hierarchy in the traditional sense. But they do require layered control. Orchestration agents must coordinate task agents. Governance agents must oversee orchestration. Interface agents must ensure humans stay in the loop.

This control plane enables a CFO, CRO, or COO to delegate with clarity. Not “let the machine decide,” but “let the system decide under these conditions, with this fallback, and with this visibility.”

We are not building a flat organization. We are building a layered intelligence architecture. And every layer must serve a different purpose: execution, synthesis, escalation, and communication.

From Workflows to Decision Flows

Most enterprise systems are designed around workflows, which are sequences of tasks that are completed by both systems and people. But autonomous enterprises operate on decision flows. The question becomes: What decisions are being made, by whom, with what confidence, and what outcome?

That is the CFO’s new visibility requirement. Not just “how long did the close take?” but “how many agent decisions were made, how many required escalation, and how many were corrected?”

In one multinational manufacturing organization, they tracked decision flow analytics and created a heatmap of friction points. It highlighted areas where agents struggled, where humans overrode too frequently, and where process ambiguity required design. That heatmap became their product roadmap.

Final Reflections: Designing With Responsibility

Autonomy is not a destination. It is a design choice. The companies that succeed will not be the ones that deploy the most agents. They will be the ones who design the clearest systems of accountability, oversight, and coordination.

We must build enterprises that not only scale output but also scale judgment. That not only eliminates work but also elevates insight.

The autonomous enterprise is not science fiction. It is already emerging: one agent at a time, one recovery loop at a time, and one design decision at a time.

The Finance Playbook for Scaling Complexity Without Chaos

From Controlled Growth to Operational Grace

Somewhere between Series A optimism and Series D pressure sits the very real challenge of scale. Not just growth for its own sake but growth with control, precision, and purpose. A well-run finance function becomes less about keeping the lights on and more about lighting the runway. I have seen it repeatedly. You can double ARR, but if your deal desk, revenue operations, or quote-to-cash processes are even slightly out of step, you are scaling chaos, not a company.

Finance does not scale with spreadsheets and heroics. It scales with clarity. With every dollar, every headcount, and every workflow needing to be justified in terms of scale, simplicity must be the goal. I recall sitting in a boardroom where the CEO proudly announced a doubling of the top line. But it came at the cost of three overlapping CPQ systems, elongated sales cycles, rogue discounting, and a pipeline no one trusted. We did not have a scale problem. We had a complexity problem disguised as growth.

OKRs Are Not Just for Product Teams

When finance is integrated into company OKRs, magic happens. We begin aligning incentives across sales, legal, product, and customer success teams. Suddenly, the sales operations team is not just counting bookings but shaping them. Deal desk isn’t just a speed bump before legal review, but a value architect. Our quote-to-cash process is no longer a ticketing system but a flywheel for margin expansion.

At a Series B company, their shift began by tying financial metrics directly to the revenue team’s OKRs. Quota retirement was not enough. They measured the booked gross margin. Customer acquisition cost. Implementation of velocity. The sales team was initially skeptical but soon began asking more insightful questions. Deals that initially appeared promising were flagged early. Others that seemed too complicated were simplified before they even reached RevOps. Revenue is often seen as art. But finance gives it rhythm.

Scaling Complexity Despite the Chaos

The truth is that chaos is not the enemy of scale. Chaos is the cost of momentum. Every startup that is truly growing at a pace inevitably creates complexity. Systems become tangled. Roles blur. Approvals drift. That is not failure. That is physics. What separates successful companies is not the absence of chaos but their ability to organize it.

I often compare this to managing a growing city. You do not stop new buildings from going up just because traffic worsens. You introduce traffic lights, zoning laws, and transit systems that support the growth. In finance, that means being ready to evolve processes as soon as growth introduces friction. It means designing modular systems where complexity is absorbed rather than resisted. You do not simplify the growth. You streamline the experience of growing. Read Scale by Geoffrey West. Much of my interest in complexity theory and architecture for scale comes from it. Also, look out for my book, which will be published in February 2026: Complexity and Scale: Managing Order from Chaos. This book aligns literature in complexity theory with the microeconomics of scaling vectors and enterprise architecture.

At a late-stage Series C company, the sales motion had shifted from land-and-expand to enterprise deals with multi-year terms and custom payment structures. The CPQ tool was unable to keep up. Rather than immediately overhauling the tool, they developed middleware logic that routed high-complexity deals through a streamlined approval process, while allowing low-risk deals to proceed unimpeded. The system scaled without slowing. Complexity still existed, but it no longer dictated pace.

Cash Discipline: The Ultimate Growth KPI

Cash is not just oxygen. It is alignment. When finance speaks early and often about burn efficiency, marginal unit economics, and working capital velocity, we move from gatekeepers to enablers. I often remind founders that the cost of sales is not just the commission plan. It’s in the way deals are structured. It’s in how fast a contract can be approved. It’s in how many hands a quote needs to pass through.

At one Series A professional services firm, they introduced a “Deal ROI Calculator” at the deal desk. It calculated not just price and term but implementation effort, support burden, and payback period. The result was staggering. Win rates remained stable, but average deal profitability increased by 17 percent. Sales teams began choosing deals differently. Finance was not saying no. It was saying, “Say yes, but smarter.”

Velocity is a Decision, Not a Circumstance

The best-run companies are not faster because they have fewer meetings. They are faster because decisions are closer to the data. Finance’s job is to put insight into the hands of those making the call. The goal is not to make perfect decisions. It is to make the best decision possible with the available data and revisit it quickly.

In one post-Series A firm, we embedded finance analysts inside revenue operations. It blurred the traditional lines but sped up decision-making. Discount approvals have been reduced from 48 hours to 12-24 hours. Pricing strategies became iterative. A finance analyst co-piloted the forecast and flagged gaps weeks earlier than our CRM did. It wasn’t about more control. It was about more confidence.

When Process Feels Like Progress

It is tempting to think that structure slows things down. However, the right QTC design can unlock margin, trust, and speed simultaneously. Imagine a deal desk that empowers sales to configure deals within prudent guardrails. Or a contract management workflow that automatically flags legal risks. These are not dreams. These are the functions we have implemented.

The companies that scale well are not perfect. But their finance teams understand that complexity compounds quietly. And so, we design our systems not to prevent chaos but to make good decisions routine. We don’t wait for the fire drill. We design out the fire.

Make Your Revenue Operations Your Secret Weapon

If your finance team still views sales operations as a reporting function, you are underutilizing a strategic lever. Revenue operations, when empowered, can close the gap between bookings and billings. They can forecast with precision. They can flag incentive misalignment. One of the best RevOps leaders I worked with used to say, “I don’t run reports. I run clarity.” That clarity was worth more than any point solution we bought.

In scaling environments, automation is not optional. But automation alone does not save a broken process. Finance must own the blueprint. Every system, from CRM to CPQ to ERP, must speak the same language. Data fragmentation is not just annoying. It is value-destructive.

What Should You Do Now?

Ask yourself: Does finance have visibility into every step of the revenue funnel? Do our QTC processes support strategic flexibility? Is our deal desk a source of friction or a source of enablement? Can our sales comp plan be audited and justified in a board meeting without flinching?

These are not theoretical. They are the difference between Series C confusion and Series D confidence.

Let’s Make This Personal

I have seen incredible operators get buried under process debt because they mistook motion for progress. I have seen lean finance teams punch above their weight because they anchored their operating model in OKRs, cash efficiency, and rapid decision cycles. I have also seen the opposite. A sales ops function sitting in the corner. A deal desk no one trusts. A QTC process where no one knows who owns what.

These are fixable. But only if finance decides to lead. Not just report.

So here is my invitation. If you are a CFO, a CRO, a GC, or a CEO reading this, take one day this quarter to walk your revenue path from lead to cash. Sit with the people who feel the friction. Map the handoffs. And then ask, is this how we scale with control? Do you have the right processes in place? Do you have the technology to activate the process and minimize the friction?

Beyond the Buzz: The Real Economics Behind SaaS, AI, and Everything in Between

Introduction

Throughout my career, I have had the privilege of working in and leading finance teams across several SaaS companies. The SaaS model is familiar territory to me: its economics are well understood, its metrics are measurable, and its value creation pathways have been tested over time. Erich Mersch’s book on SaaS Hacks is my Bible. In contrast, my exposure to pure AI companies has been more limited. I have directly supported two AI-driven businesses, and much of my perspective comes from observation, benchmarking, and research. This combination of direct experience and external study has hopefully shaped a balanced view: one grounded in practicality yet open to the new dynamics emerging in the AI era.

Across both models, one principle remains constant: a business is only as strong as its unit economics. When leaders understand the economics of their business, they gain the ability to map them to daily operations, and from there, to the financial model. The linkage from unit economics to operations to financial statements is what turns financial insight into strategic control. It ensures that decisions on pricing, product design, and investment are all anchored in how value is truly created and captured.

Today, CFOs and CEOs must not only manage their profit and loss (P&L) statement but also understand the anatomy of revenue, cost, and cash flow at the micro level. SaaS, AI, and hybrid SaaS-AI models each have unique economic signatures. SaaS rewards scalability and predictability. AI introduces variability and infrastructure intensity. Hybrids offer both opportunity and complexity. This article examines the financial structure, gross margin profile, and investor lens of each model to help finance leaders not only measure performance but also interpret it by turning data into judgment and judgment into a better strategy.

Part I: SaaS Companies — Economics, Margins, and Investor Lens

The heart of any SaaS business is its recurring revenue model. Unlike traditional software, where revenue is recognized upfront, SaaS companies earn revenue over time as customers subscribe to a service. This shift from ownership to access creates predictable revenue streams but also introduces delayed payback cycles and continuous obligations to deliver value. Understanding the unit economics behind this model is essential for CFOs and CEOs, as it enables them to see beyond top-line growth and assess whether each customer, contract, or cohort truly creates long-term value.

A strong SaaS company operates like a flywheel. Customer acquisition drives recurring revenue, which funds continued innovation and improved service, in turn driving more customer retention and referrals. But a flywheel is only as strong as its components. The economics of SaaS can be boiled down to a handful of measurable levers: gross margin, customer acquisition cost, retention rate, lifetime value, and cash efficiency. Each one tells a story about how the company converts growth into profit.

The SaaS Revenue Engine

At its simplest, a SaaS company makes money by providing access to its platform on a subscription basis. The standard measure of health is Annual Recurring Revenue (ARR). ARR represents the contracted annualized value of active subscriptions. It is the lifeblood metric of the business. When ARR grows steadily with low churn, the company can project future cash flows with confidence.

Revenue recognition in SaaS is governed by time. Even if a customer pays upfront, the revenue is recognized over the duration of the contract. This creates timing differences between bookings, billings, and revenue. CFOs must track all three to understand both liquidity and profitability. Bookings signal demand, billings signal cash inflow, and revenue reflects the value earned.

One of the most significant advantages of SaaS is predictability. High renewal rates lead to stable revenues. Upsells and cross-sells increase customer lifetime value. However, predictability can also mask underlying inefficiencies. A SaaS business can grow fast and still destroy value if each new customer costs more to acquire than they bring in lifetime revenue. This is where unit economics comes into play.

Core Unit Metrics in SaaS

The three central metrics every CFO and CEO must know are:

- Customer Acquisition Cost (CAC): The total sales and marketing expenses needed to acquire one new customer.

- Lifetime Value (LTV): The total revenue a customer is expected to generate over their relationship with the company.

- Payback Period: The time it takes for gross profit from a customer to recover CAC.

A healthy SaaS business typically maintains an LTV-to-CAC ratio of at least 3:1. This means that for every dollar spent acquiring a customer, the company earns three dollars in lifetime value. Payback periods under twelve months are typically considered strong, especially in mid-market or enterprise SaaS. Long payback periods signal cash inefficiency and high-risk during downturns.

Retention is equally essential. The stickier the product, the lower the churn, and the more predictable the revenue. Net revenue retention (NRR) is a powerful metric because it combines churn and expansion. A business with 120 percent NRR is growing revenue even without adding new customers, which investors love to see.

Gross Margin Dynamics

Gross margin is the backbone of SaaS profitability. It measures how much of each revenue dollar remains after deducting direct costs, such as hosting, support, and third-party software fees. Well-run SaaS companies typically achieve gross margins of between 75% and 85%. This reflects the fact that software is highly scalable. Once built, it can be replicated at almost no additional cost. They use the margins to fund their GTM strategy. They have room until they don’t.

However, gross margin is not guaranteed. In practice, it can erode for several reasons. First, rising cloud infrastructure costs can quietly eat into margins if not carefully managed. Companies that rely heavily on AWS, Azure, or Google Cloud need cost optimization strategies, including reserved instances and workload tuning. Second, customer support and success functions, while essential, can become heavy if processes are not automated. Third, complex integrations or data-heavy products can increase variable costs per customer.

Freemium and low-entry pricing models can also dilute margins if too many users remain on free tiers or lower-paying plans. The CFO’s job is to ensure that pricing reflects the actual value delivered and that the cost-to-serve remains aligned with revenue per user. A mature SaaS company tracks unit margins by customer segment to identify where profitability thrives or erodes.

Operating Leverage and the Rule of 40

The power of SaaS lies in its potential for operating leverage. Fixed costs, such as R&D, engineering, and sales infrastructure, remain relatively constant as revenue scales. As a result, incremental revenue flows disproportionately to the bottom line once the business passes break-even. This makes SaaS an attractive model once scale is achieved, although reaching that scale can take a considerable amount of time.

The Rule of 40 is a shorthand metric many investors use to gauge the balance between growth and profitability. It states that a SaaS company’s revenue growth rate, plus its EBITDA margin, should equal or exceed 40 percent. A company growing 30 percent annually with a 15 percent EBITDA margin scores 45, which is considered healthy. A company growing at 60 percent but losing 30 percent EBITDA would score 30, suggesting inefficiency. This rule forces management to strike a balance between ambition and discipline. This 40% rule was based on empirical analysis, and every Jack and Jill swears by it. I am not sure that we can have this Rule and apply it blindly. I am not generally in favor of these broad rules. That is a lot of fodder for a different conversation.

Cash Flow and Efficiency

Cash flow timing is another defining feature of SaaS. Many customers prepay annually, creating favorable working capital dynamics. This gives SaaS companies negative net working capital, which can help fund growth. However, high upfront CAC and long payback periods can strain cash reserves. CFOs must ensure growth is financed efficiently and that burn multiples remain sustainable. Burn-multiple measures the cash burn relative to net new ARR added. A burn rate of multiple below 1 is excellent; it means the company spends one dollar to generate one dollar of recurring revenue. Ratios above 2 suggest inefficiency.

As markets have tightened, investors have shifted focus from pure growth to efficient growth. Cash is no longer cheap, and dilution from equity raises is costly. I attended a networking event in San Jose about a month ago, and one of the finance leaders said, “We are in the middle of a nuclear winter.” I thought that summarized the current state of the funding market. Therefore, SaaS CFOs must guide companies toward self-funding growth, improving gross margins, and shortening CAC payback cycles.

Valuation and Investor Perspective

Investors view SaaS companies through the lens of predictability, scalability, and margin potential. Historically, during low-interest-rate periods, high-growth SaaS companies traded at 10 to 15 times ARR. In the current normalized environment, top performers trade between 5 and 8 times ARR, with discounts for slower growth or lower margins.

The key drivers of valuation include:

- Growth Rate: Faster ARR growth leads to higher multiples, provided it is efficient.

- Gross Margin: High margins indicate scalability and control over cost structure.

- Retention and Expansion: Strong NRR signals durable revenue and pricing power.

- Profitability Trajectory: Investors reward companies that balance growth with clear paths to cash flow breakeven.

Investors now differentiate between the quality of growth and the quantity of growth. Revenue driven by deep discounts or heavy incentives is less valuable than revenue driven by customer adoption and satisfaction. CFOs must clearly communicate cohort performance, renewal trends, and contribution margins to demonstrate that growth is sustainable and durable.

Emerging Challenges in SaaS Economics

While SaaS remains a powerful model, new challenges have emerged. Cloud infrastructure costs are rising, putting pressure on gross margins. AI features are becoming table stakes, but they introduce new variable costs tied to compute. Customer expectations are also shifting toward usage-based pricing, which can lead to reduced predictability in revenue recognition.

To navigate these shifts, CFOs must evolve their financial reporting and pricing strategies. Gross margin analysis must now include compute efficiency metrics. Sales compensation plans must reflect profitability, not just bookings. Pricing teams must test elasticity to ensure ARPU growth outpaces cost increases.

SaaS CFOs must also deepen their understanding of cohort economics. Not all customers are equal. Some segments deliver faster payback and higher retention, while others create drag. Segmented reporting enables management to allocate capital wisely and avoid pursuing unprofitable markets.

The Path Forward

The essence of SaaS unit economics is discipline. Growth only creates value when each unit of growth strengthens the financial foundation. This requires continuous monitoring of margins, CAC, retention, and payback. It also requires cross-functional collaboration between finance, product, and operations. Finance must not only report outcomes but also shape strategy, ensuring that pricing aligns with value and product decisions reflect cost realities.

For CEOs, understanding these dynamics is vital to setting priorities. For CFOs, the task is to build a transparent model that links operational levers to financial outcomes. Investors reward companies that can tell a clear story with data: a path from top-line growth to sustainable free cash flow.

Ultimately, SaaS remains one of the most attractive business models when executed effectively. The combination of recurring revenue, high margins, and operating leverage creates long-term compounding value. But it rewards precision. The CFO who masters unit economics can turn growth into wealth, while the one who ignores it may find that scale without discipline is simply a faster road to inefficiency. The king is not dead: Long live the king.

Part II: Pure AI Companies — Economics, Margins, and Investor Lens

Artificial intelligence companies represent a fundamentally different business model from traditional SaaS. Where SaaS companies monetize access to pre-built software, AI companies monetize intelligence: the ability of models to learn, predict, and generate. This shift changes everything about unit economics. The cost per unit of value is no longer near zero. It is tied to the underlying cost of computation, data processing, and model maintenance. As a result, CFOs and CEOs leading AI-first companies must rethink what scale, margin, and profitability truly mean.

While SaaS scales easily once software is built, AI scales conditionally. Each customer interaction may trigger new inference requests, consume GPU time, and incur variable costs. Every additional unit of demand brings incremental expenses. The CFO’s challenge is to translate these technical realities into financial discipline, which involves building an organization that can sustain growth without being constrained by its own cost structure.

Understanding the AI Business Model

AI-native companies generate revenue by providing intelligence as a service. Their offerings typically fall into three categories:

- Platform APIs: Selling access to models that perform tasks such as image recognition, text generation, or speech processing.

- Enterprise Solutions: Custom model deployments tailored for specific industries like healthcare, finance, or retail.

- Consumer Applications: AI-powered tools like copilots, assistants, or creative generators.

Each model has unique economics. API-based businesses often employ usage-based pricing, resembling utilities. Enterprise AI firms resemble consulting hybrids, blending software with services. Consumer AI apps focus on scale, requiring low-cost inference to remain profitable.

Unlike SaaS subscriptions, AI revenue is often usage-driven. This makes it more elastic but less predictable. When customers consume more tokens, queries, or inferences, revenue rises but so do costs. This tight coupling between revenue and cost means margins depend heavily on technical efficiency. CFOs must treat cost-per-inference as a central KPI, just as SaaS leaders track gross margin percentage.

Gross Margins and Cost Structures

For pure AI companies, the gross margin reflects the efficiency of their infrastructure. In the early stages, margins often range between 40% and 60%. With optimization, some mature players approach 70 percent or higher. However, achieving SaaS-like margins requires significant investment in optimization techniques, such as model compression, caching, and hardware acceleration.

The key cost components include:

- Compute: GPU and cloud infrastructure costs are the most significant variable expenses. Each inference consumes compute cycles, and large models require expensive hardware.

- Data: Training and fine-tuning models involve significant data acquisition, labeling, and storage costs.

- Serving Infrastructure: Orchestration, latency management, and load balancing add further expenses.

- Personnel: Machine learning engineers, data scientists, and research teams represent high fixed costs.

Unlike SaaS, where the marginal cost per user declines toward zero, AI marginal costs can remain flat or even rise with increasing complexity. The more sophisticated the model, the more expensive it is to serve each request. CFOs must therefore design pricing strategies that match the cost-to-serve, ensuring unit economics remain positive.

To track progress, leading AI finance teams adopt new metrics such as cost per 1,000 tokens, cost per inference, or cost per output. These become the foundation for gross margin improvement programs. Without these metrics, management cannot distinguish between profitable and loss-making usage.

Capital Intensity and Model Training

A defining feature of AI economics is capital intensity. Training large models can cost tens or even hundreds of millions of dollars. These are not operating expenses in the traditional sense; they are long-term investments. The question for CFOs is how to treat them. Should they be expensed, like research and development, or capitalized, like long-lived assets? The answer depends on accounting standards and the potential for model reuse.

If a model will serve as a foundation for multiple products or customers over several years, partial capitalization may be a defensible approach. However, accounting conservatism often favors expensing, which depresses near-term profits. Regardless of treatment, management must view training costs as sunk investments that must earn a return through widespread reuse.

Due to these high upfront costs, AI firms must carefully plan their capital allocation. Not every model warrants training from scratch. Fine-tuning open-source or pre-trained models may achieve similar outcomes at a fraction of the cost. The CFO’s role is to evaluate return on invested capital in R&D and ensure technical ambition aligns with commercial opportunity.

Cash Flow Dynamics

Cash flow management in AI businesses is a significant challenge. Revenue often scales more slowly than costs in early phases. Infrastructure bills accrue monthly, while customers may still be in pilot stages. This results in negative contribution margins and high burn rates. Without discipline, rapid scaling can amplify losses.

The path to positive unit economics comes from optimization. Model compression, quantization, and batching can lower the cost per inference. Strategic use of lower-cost hardware, such as CPUs for lighter tasks, can also be beneficial. Some firms pursue vertical integration, building proprietary chips or partnering for preferential GPU pricing. Others use caching and heuristic layers to reduce the number of repeated inference calls.

Cash efficiency improves as AI companies move from experimentation to productization. Once a model stabilizes and workload patterns become predictable, cost forecasting and margin planning become more reliable. CFOs must carefully time their fundraising and growth, ensuring the company does not overbuild infrastructure before demand materializes.

Pricing Strategies

AI pricing remains an evolving art. Standard models include pay-per-use, subscription tiers with usage caps, or hybrid pricing that blends base access fees with variable usage charges. The proper structure depends on the predictability of usage, customer willingness to pay, and cost volatility.

Usage-based pricing aligns revenue with cost but increases forecasting uncertainty. Subscription pricing provides stability but can lead to margin compression if usage spikes. CFOs often employ blended approaches, utilizing base subscriptions that cover average usage, with additional fees for exceeding demand. This provides a buffer against runaway costs while maintaining customer flexibility.

Transparent pricing is crucial. Customers need clarity about what drives cost. Complexity breeds disputes and churn. Finance leaders should collaborate with product and sales teams to develop pricing models that are straightforward, equitable, and profitable. Scenario modeling helps anticipate edge cases where heavy usage erodes margins.

Valuation and Investor Perspective

Investors evaluate AI companies through a different lens than SaaS. Because AI is still an emerging field, investors look beyond current profitability and focus on technical moats, data advantages, and the scalability of cost curves. A strong AI company demonstrates three things:

- Proprietary Model or Data: Access to unique data sets or model architectures that competitors cannot easily replicate.

- Cost Curve Mastery: A clear path to reducing cost per inference as scale grows.

- Market Pull: Evidence of real-world demand and willingness to pay for intelligence-driven outcomes.

Valuations often blend software multiples with hardware-like considerations. Early AI firms may be valued at 6 to 10 times forward revenue if they show strong growth and clear cost reduction plans. Companies perceived as purely research-driven, without commercial traction, face steeper discounts. Investors are increasingly skeptical of hype and now seek proof of sustainable margins.

In diligence, investors focus on gross margin trajectory, data defensibility, and customer concentration. They ask questions like: How fast is the cost per inference declining? What portion of revenue comes from repeat customers? How dependent is the business on third-party models or infrastructure? The CFO’s job is to prepare crisp, data-backed answers.

Measuring Efficiency and Scale

AI CFOs must introduce new forms of cost accounting. Traditional SaaS dashboards that focus solely on ARR and churn are insufficient. AI demands metrics that link compute usage to financial outcomes. Examples include:

- Compute Utilization Rate: Percentage of GPU capacity effectively used.

- Model Reuse Ratio: Number of applications or customers served by a single trained model.

- Cost per Output Unit: Expense per generated item, prediction, or token.

By tying these technical metrics to revenue and gross margin, CFOs can guide engineering priorities. Finance becomes a strategic partner in improving efficiency, not just reporting cost overruns. In a later article, we will discuss complexity and Scale. I am writing a book on that subject, and this is highly relevant to how AI-based businesses are evolving. It is expected to be released by late February next year and will be available on Kindle as an e-book.

Risk Management and Uncertainty

AI companies face unique risks. Dependence on external cloud providers introduces pricing and supply risks. Regulatory scrutiny over data usage can limit access to models or increase compliance costs. Rapid technological shifts may render models obsolete before their amortization is complete. CFOs must build contingency plans, diversify infrastructure partners, and maintain agile capital allocation processes.

Scenario planning is essential. CFOs should model high, medium, and low usage cases with corresponding cost structures. Sensitivity analysis on cloud pricing, GPU availability, and demand elasticity helps avoid surprises. Resilience matters as much as growth.

The Path Forward

For AI companies, the journey to sustainable economics is one of learning curves. Every technical improvement that reduces the cost per unit enhances the margin. Every dataset that improves model accuracy also enhances customer retention. Over time, these compounding efficiencies create leverage like SaaS, but the path is steeper.

CFOs must view AI as a cost-compression opportunity. The winners will not simply have the best models but the most efficient ones. Investors will increasingly value businesses that show declining cost curves, strong data moats, and precise product-market fit.

For CEOs, the message is focus. Building every model from scratch or chasing every vertical can drain capital. The best AI firms choose their battles wisely, investing deeply in one or two defensible areas. Finance leaders play a crucial role in guiding these choices with evidence, rather than emotion.

In summary, pure AI companies operate in a world where scale is earned, not assumed. The economics are challenging but not insurmountable. With disciplined pricing, rigorous cost tracking, and clear communication to investors, AI businesses can evolve from capital-intensive experiments into enduring, high-margin enterprises. The key is turning intelligence into economics and tackling it one inference at a time.

Part III: SaaS + AI Hybrid Models: Economics and Investor Lens

In today’s market, most SaaS companies are no longer purely software providers. They are becoming intelligence platforms, integrating artificial intelligence into their products to enhance customer value. These hybrid models combine the predictability of SaaS with the innovation of AI. They hold great promises, but they also introduce new complexities in economics, margin structure, and investor expectations. For CFOs and CEOs, the challenge is not just understanding how these elements coexist but managing them in harmony to deliver profitable growth.

The hybrid SaaS-AI model is not simply the sum of its parts. It requires balancing two different economic engines: one that thrives on recurring, high-margin revenue and another that incurs variable costs linked to compute usage. The key to success lies in recognizing where AI enhances value and where it risks eroding profitability. Leaders who can measure, isolate, and manage these dynamics can unlock superior economics and investor confidence.

The Nature of Hybrid SaaS-AI Businesses

A hybrid SaaS-AI company starts with a core subscription-based platform. Customers pay recurring fees for access, support, and updates. Additionally, the company leverages AI-powered capabilities to enhance automation, personalization, analytics, and decision-making. These features can be embedded into existing workflows or offered as add-ons, sometimes billed based on usage.

Examples include CRMs with AI-assisted forecasting, HR platforms with intelligent candidate screening, or project tools with predictive insights. In each case, AI transforms user experience and perceived value, but it also introduces incremental cost per transaction. Every inference call, data model query, or real-time prediction consumes compute power and storage.