Blog Archives

The CFO as Chief Option Architect: Embracing Uncertainty

Part I: Embracing the Options Mindset

This first half explores the philosophical and practical foundation of real options thinking, scenario-based planning, and the CFO’s evolving role in navigating complexity. The voice is grounded in experience, built on systems thinking, and infused with a deep respect for the unpredictability of business life.

I learned early that finance, for all its formulas and rigor, rarely rewards control. In one of my earliest roles, I designed a seemingly watertight budget, complete with perfectly reconciled assumptions and cash flow projections. The spreadsheet sang. The market didn’t. A key customer delayed a renewal. A regulatory shift in a foreign jurisdiction quietly unraveled a tax credit. In just six weeks, our pristine model looked obsolete. I still remember staring at the same Excel sheet and realizing that the budget was not a map, but a photograph, already out of date. That moment shaped much of how I came to see my role as a CFO. Not as controller-in-chief, but as architect of adaptive choices.

The world has only become more uncertain since. Revenue operations now sit squarely in the storm path of volatility. Between shifting buying cycles, hybrid GTM models, and global macro noise, what used to be predictable has become probabilistic. Forecasting a quarter now feels less like plotting points on a trendline and more like tracing potential paths through fog. It is in this context that I began adopting and later, championing, the role of the CFO as “Chief Option Architect.” Because when prediction fails, design must take over.

This mindset draws deeply from systems thinking. In complex systems, what matters is not control, but structure. A system that adapts will outperform one that resists. And the best way to structure flexibility, I have found, is through the lens of real options. Borrowed from financial theory, real options describe the value of maintaining flexibility under uncertainty. Instead of forcing an all-in decision today, you make a series of smaller decisions, each one preserving the right, but not the obligation, to act in a future state. This concept, though rooted in asset pricing, holds powerful relevance for how we run companies.

When I began modeling capital deployment for new GTM motions, I stopped thinking in terms of “budget now, or not at all.” Instead, I started building scenario trees. Each branch represented a choice: deploy full headcount at launch or split into a two-phase pilot with a learning checkpoint. Invest in a new product SKU with full marketing spend, or wait for usage threshold signals to pass before escalation. These decision trees capture something that most budgets never do—the reality of the paths not taken, the contingencies we rarely discuss. And most importantly, they made us better at allocating not just capital, but attention. I am sharing my Bible on this topic, which was referred to me by Dr. Alexander Cassuto at Cal State Hayward in the Econometrics course. It was definitely more pleasant and easier to read than Jiang’s book on Econometrics.

This change in framing altered my approach to every part of revenue operations. Take, for instance, the deal desk. In traditional settings, deal desk is a compliance checkpoint where pricing, terms, and margin constraints are reviewed. But when viewed through an options lens, the deal desk becomes a staging ground for strategic bets. A deeply discounted deal might seem reckless on paper, but if structured with expansion clauses, usage gates, or future upsell options, it can behave like a call option on account growth. The key is to recognize and price the option value. Once I began modeling deals this way, I found we were saying “yes” more often, and with far better clarity on risk.

Data analytics became essential here not for forecasting the exact outcome, but for simulating plausible ones. I leaned heavily on regression modeling, time-series decomposition, and agent-based simulation. We used R to create time-based churn scenarios across customer cohorts. We used Arena to simulate resource allocation under delayed expansion assumptions. These were not predictions. They were controlled chaos exercises, designed to show what could happen, not what would. But the power of this was not just in the results, but it was in the mindset it built. We stopped asking, “What will happen?” and started asking, “What could we do if it does?”

From these simulations, we developed internal thresholds to trigger further investment. For example, if three out of five expansion triggers were fired, such as usage spike, NPS improvement, and additional department adoption, then we would greenlight phase two of GTM spend. That logic replaced endless debate with a predefined structure. It also gave our board more confidence. Rather than asking them to bless a single future, we offered a roadmap of choices, each with its own decision gates. They didn’t need to believe our base case. They only needed to believe we had options.

Yet, as elegant as these models were, the most difficult challenge remained human. People, understandably, want certainty. They want confidence in forecasts, commitment to plans, and clarity in messaging. I had to coach my team and myself to get comfortable with the discomfort of ambiguity. I invoked the concept of bounded rationality from decision science: we make the best decisions we can with the information available to us, within the time allotted. There is no perfect foresight. There is only better framing.

This is where the law of unintended consequences makes its entrance. In traditional finance functions, overplanning often leads to rigidity. You commit to hiring plans that no longer make sense three months in. You promise CAC thresholds that collapse under macro pressure. You bake linearity into a market that moves in waves. When this happens, companies double down, pushing harder against the wrong wall. But when you think in options, you pull back when the signal tells you to. You course-correct. You adapt. And paradoxically, you appear more stable.

As we embedded this thinking deeper into our revenue operations, we also became more cross-functional. Sales began to understand the value of deferring certain go-to-market investments until usage signals validated demand. Product began to view feature development as portfolio choices: some high-risk, high-return, others safer but with less upside. Customer Success began surfacing renewal and expansion probabilities not as binary yes/no forecasts, but as weighted signals on a decision curve. The shared vocabulary of real options gave us a language for navigating ambiguity together.

We also brought this into our capital allocation rhythm. Instead of annual budget cycles, we moved to rolling forecasts with embedded thresholds. If churn stayed below 8% and expansion held steady, we would greenlight an additional five SDRs. If product-led growth signals in EMEA hit critical mass, we’d fund a localized support pod. These weren’t whims. They were contingent commitments, bound by logic, not inertia. And that changed everything.

The results were not perfect. We made wrong bets. Some options expired worthless. Others took longer to mature than we expected. But overall, we made faster decisions with greater alignment. We used our capital more efficiently. And most of all, we built a culture that didn’t flinch at uncertainty—but designed for it.

In the next part of this essay, I will go deeper into the mechanics of implementing this philosophy across the deal desk, QTC architecture, and pipeline forecasting. I will also show how to build dashboards that visualize decision trees and option paths, and how to teach your teams to reason probabilistically without losing speed. Because in a world where volatility is the only certainty, the CFO’s most enduring edge is not control, but it is optionality, structured by design and deployed with discipline.

Part II: Implementing Option Architecture Inside RevOps

A CFO cannot simply preach agility from a whiteboard. To embed optionality into the operational fabric of a company, the theory must show up in tools, in dashboards, in planning cadences, and in the daily decisions made by deal desks, revenue teams, and systems owners. I have found that fundamental transformation comes not from frameworks, but from friction—the friction of trying to make the idea work across functions, under pressure, and at scale. That’s where option thinking proves its worth.

We began by reimagining the deal desk, not as a compliance stop but as a structured betting table. In conventional models, deal desks enforce pricing integrity, review payment terms, and ensure T’s and C’s fall within approved tolerances. That’s necessary, but not sufficient. In uncertain environments—where customer buying behavior, competitive pressure, or adoption curves wobble without warning: rigid deal policies become brittle. The opportunity lies in recasting the deal desk as a decision node within a larger options tree.

Consider a SaaS enterprise deal involving land-and-expand potential. A rigid model forces either full commitment upfront or defers expansion, hoping for a vague “later.” But if we treat the deal like a compound call option, we see more apparent logic. You price the initial land deal aggressively, with usage-based triggers that, when met, unlock favorable expansion terms. You embed a re-pricing clause if usage crosses a defined threshold in 90 days. You insert a “soft commit” expansion clause tied to the active user count. None of these is just a term. They are embedded with real options. And when structured well, they deliver upside without requiring the customer to commit to uncertain future needs.

In practice, this approach meant reworking CPQ systems, retraining legal, and coaching reps to frame options credibly. We designed templates with optionality clauses already coded into Salesforce workflows. Once an account crossed a pre-defined trigger say, 80% license utilization, then the next best action flowed to the account executive and customer success manager. The logic wasn’t linear. It was branching. We visualized deal paths in a way that corresponds to mapping a decision tree in a risk-adjusted capital model.

Yet even the most elegant structure can fail if the operating rhythm stays linear. That is why we transitioned away from rigid quarterly forecasts toward rolling scenario-based planning. Forecasting ceased to be a spreadsheet contest. Instead, we evaluated forecast bands, not point estimates. If base churn exceeded X% in a specific cohort, how did that impact our expansion coverage ratio? If deal velocity in EMEA slowed by two weeks, how would that compress the bookings-to-billings gap? We visualized these as cascading outcomes, not just isolated misses.

To build this capability, we used what I came to call “option dashboards.” These were layered, interactive models with inputs tied to a live pipeline and post-sale telemetry. Each card on the dashboard represented a decision node—an inflection point. Would we deploy more headcount into SMB if the average CAC-to-LTV fell below 3:1? Would we pause feature rollout in one region to redirect support toward a segment with stronger usage signals? Each choice was pre-wired with boundary logic. The decisions didn’t live in a drawer—they lived in motion.

Building these dashboards required investment. But more than tools, it required permission. Teams needed to know they could act on signal, not wait for executive validation every time a deviation emerged. We institutionalized the language of “early signal actionability.” If revenue leaders spotted a decline in renewal health across a cluster of customers tied to the same integration module, they didn’t wait for a churn event. They pulled forward roadmap fixes. That wasn’t just good customer service, but it was real options in flight.

This also brought a new flavor to our capital allocation rhythm. Rather than annual planning cycles that locked resources into static swim lanes, we adopted gated resourcing tied to defined thresholds. Our FP&A team built simulation models in Python and R, forecasting the expected value of a resourcing move based on scenario weightings. For example, if a new vertical showed a 60% likelihood of crossing a 10-deal threshold by mid-Q3, we pre-approved GTM spend to activate contingent on hitting that signal. This looked cautious to some. But in reality, it was aggressive and in the right direction, at the right moment.

Throughout all of this, I kept returning to a central truth: uncertainty punishes rigidity, but rewards those who respect its contours. A pricing policy that cannot flex will leave margin on the table or kill deals in flight. A hiring plan that commits too early will choke working capital. And a CFO who waits for clarity before making bets will find they arrive too late. In decision theory, we often talk about “the cost of delay” versus “the cost of error.” A good options model minimizes both, which, interestingly, is not by being just right, but by being ready.

Of course, optionality without discipline can devolve into indecision. We embedded guardrails. We defined thresholds that made decision inertia unacceptable. If a cohort’s NRR dropped for three consecutive months and win-back campaigns failed, we sunsetted that motion. If a beta feature was unable to hit usage velocity within a quarter, we reallocated the development budget. These were not emotional decisions, but they were logical conclusions of failed options. And we celebrated them. A failed option, tested and closed, beats a zombie investment every time.

We also revised our communication with the board. Instead of defending fixed forecasts, we presented probability-weighted trees. “If churn holds, and expansion triggers fire, we’ll beat target by X.” “If macro shifts pull SMB renewals down by 5%, we stay within plan by flexing mid-market initiatives.” This shifted the conversation from finger-pointing to scenario readiness. Investors liked it. More importantly, so did the executive team. We could disagree on base assumptions but still align on decisions because we’d mapped the branches ahead of time.

One area where this thought made an outsized impact was compensation planning. Sales comp is notoriously fragile under volatility. We redesigned quota targets and commission accelerators using scenario bands, not fixed assumptions. We tested payout curves under best, base, and downside cases. We then ran Monte Carlo simulations to see how frequently actuals would fall into the “too much upside” or “demotivating downside” zones. This led to more durable comp plans, which meant fewer panicked mid-year resets. Our reps trusted the system. And our CFO team could model cost predictability with far greater confidence.

In retrospection, all these loops back to a single mindset shift: you don’t plan to be right. You plan to stay in the game. And staying in the game requires options that are well-designed, embedded into the process, and respected by every function. Sales needs to know they can escalate an expansion offer once particular customer signals fire. Success needs to know they have the budget authority to engage support when early churn flags arise. Product needs to know they can pause a roadmap stream if NPV no longer justifies it. And finance needs to know that its most significant power is not in control, but in preparation.

Today, when I walk into a revenue operations review or a strategic planning offsite, I do not bring a budget with fixed forecasts. I get a map. It has branches. It has signals. It has gates. And it has options, and each one designed not to predict the future, but to help us meet it with composure, and to move quickly when the fog clears.

Because in the world I have operated in, spanning economic cycles, geopolitical events, sudden buyer hesitation, system failures, and moments of exponential product success since 1994 until now, one principle has held. The companies that win are not the ones who guess right. They are the ones who remain ready. And readiness, I have learned, is the true hallmark of a great CFO.

Internal versus External Scale

This article discusses internal and external complexity before we tee up a more detailed discussion on internal versus external scale. This chapter acknowledges that complex adaptive systems have inherent internal and external complexities which are not additive. The impact of these complexities is exponential. Hence, we have to sift through our understanding and perhaps even review the salient aspects of complexity science which have already been covered in relatively more detail in earlier chapter. However, revisiting complexity science is important, and we will often revisit this across other blog posts to really hit home the fundamental concepts and its practical implications as it relates to management and solving challenges at a business or even a grander social scale.

A complex system is a part of a larger environment. It is a safe to say that the larger environment is more complex than the system itself. But for the complex system to work, it needs to depend upon a certain level of predictability and regularity between the impact of initial state and the events associated with it or the interaction of the variables in the system itself. Note that I am covering both – complex physical systems and complex adaptive systems in this discussion. A system within an environment has an important attribute: it serves as a receptor to signals of external variables of the environment that impact the system. The system will either process that signal or discard the signal which is largely based on what the system is trying to achieve. We will dedicate an entire article on system engineering and thinking later, but the uber point is that a system exists to serve a definite purpose. All systems are dependent on resources and exhibits a certain capacity to process information. Hence, a system will try to extract as many regularities as possible to enable a predictable dynamic in an efficient manner to fulfill its higher-level purpose.

Let us understand external complexities. We can interchangeably use the word environmental complexity as well. External complexity represents physical, cultural, social, and technological elements that are intertwined. These environments beleaguered with its own grades of complexity acts as a mold to affect operating systems that are mere artifacts. If operating systems can fit well within the mold, then there is a measure of fitness or harmony that arises between an internal complexity and external complexity. This is the root of dynamic adaptation. When external environments are very complex, that means that there are a lot of variables at play and thus, an internal system has to process more information in order to survive. So how the internal system will react to external systems is important and they key bridge between those two systems is in learning. Does the system learn and improve outcomes on account of continuous learning and does it continually modify its existing form and functional objectives as it learns from external complexity? How is the feedback loop monitored and managed when one deals with internal and external complexities? The environment generates random problems and challenges and the internal system has to accept or discard these problems and then establish a process to distribute the problems among its agents to efficiently solve those problems that it hopes to solve for. There is always a mechanism at work which tries to align the internal complexity with external complexity since it is widely believed that the ability to efficiently align the systems is the key to maintaining a relatively competitive edge or intentionally making progress in solving a set of important challenges.

Internal complexity are sub-elements that interact and are constituents of a system that resides within the larger context of an external complex system or the environment. Internal complexity arises based on the number of variables in the system, the hierarchical complexity of the variables, the internal capabilities of information pass-through between the levels and the variables, and finally how it learns from the external environment. There are five dimensions of complexity: interdependence, diversity of system elements, unpredictability and ambiguity, the rate of dynamic mobility and adaptability, and the capability of the agents to process information and their individual channel capacities.

If we are discussing scale management, we need to ask a fundamental question. What is scale in the context of complex systems? Why do we manage for scale? How does management for scale advance us toward a meaningful outcome? How does scale compute in internal and external complex systems? What do we expect to see if we have managed for scale well? What does the future bode for us if we assume that we have optimized for scale and that is the key objective function that we have to pursue?

Scaling Considerations in Complex Systems and Organizations: Implications

Scale represents size. In a two-dimensional world, it is a linear measurement that presents a nominal ordering of numbers. In other words, 4 is two times two and 6 would be 3 times two. In other words, the difference between 4 and 6 represents an increase in scale by two. We will discuss various aspects of scale and the learnings that we can draw from it. However, before we go down this path, we would like to touch on resource consumption.

As living organisms, we consume resources. An average human being requires 2000 calories of food per day to sustain themselves. An average human being, by the way, is largely defined in terms of size. So it would be better put if we say that a 200lb person would require 2000 calories. However, if we were to regard a specimen that is 10X the size or 2000 lbs., would it require 10X the calories to sustain itself? Conversely, if the specimen was 1/100th the size of the average human being, then would it require 1/100th the calories to sustain itself. Thus, will we consume resources linearly to our size? Are we operating in a simple linear world? And if not, what are the ramifications for science, physics, biology, organizations, cities, climate, etc.?

Let us digress a little bit from the above questions and lay out a few interesting facts. Almost half of the population in the world today live in cities. This is compared to less than 15% of the world population that lived in cities a hundred years ago. It is anticipated that almost 75% of the world population will be living in cities by 2050. The number of cities will increase and so will the size. But for cities to increase in size and numbers, it requires vast amount of resources. In fact, the resource requirements in cities are far more extensive than in agrarian societies. If there is a limit to the resources from a natural standpoint – in other words, if the world is operating on a budget of natural resources – then would this mean that the growth of the cities will be naturally reined in? Will cities collapse because of lack of resources to support its mass?

What about companies? Can companies grow infinitely? Is there a natural point where companies might hit their limit beyond which growth would not be possible? Could a company collapse because the amount of resources that is required to sustain the size would be compromised? Are there other factors aside from resource consumption that play into what might cap the growth and hence the size of the company? Are there overriding factors that come into play that would superimpose the size-resource usage equation such that our worries could be safely kept aside? Are cities and companies governed by some sort of metabolic rate that governs the sustenance of life?

Geoffrey West, a theoretical physicist, has touched on a lot of the questions in his book: Scale: The Universal Laws of Growth, Innovation, Sustainability, and the Pace of Life in Organisms, Cities, Economies, and Companies. He says that a person requires about 90W (watts) of energy to survive. That is a light bulb burning in your living room in one day. That is our metabolic rate. However, just like man does not live by bread alone, an average man has to depend on a number of other artifacts that have agglomerated in bits and pieces to provide a quality of life to maximize sustenance. The person has to have laws, electricity, fuel, automobile, plumbing and water, markets, banks, clothes, phones and engage with other folks in a complex social network to collaborate and compete to achieve their goals. Geoffrey West says that the average person requires almost 11000W or the equivalent of almost 125 90W light bulbs. To put things in greater perspective, the social metabolic rate of 11,000W is almost equivalent to a dozen elephants. (An elephant requires 10X more energy than humans even though they might be 60X the size of the physical human being). Thus, a major portion of our energy is diverted to maintain the social and physical network that closely interplay to maintain our sustenance. And while we consume massive amounts of energy, we also create a massive amount of waste – and that is an inevitable outcome. This is called the entropy impact and we will touch on this in greater detail in later articles. Hence, our growth is not only constrained by our metabolic rate: it is further dampened by entropy that exists as the Second Law of Thermodynamics. And as a system ages, the impact of entropy increases manifold. Yes, it is true: once we get old, we are racing toward our death at a faster pace than when we were young. Our bodies are exhibiting fatigue faster than normal.

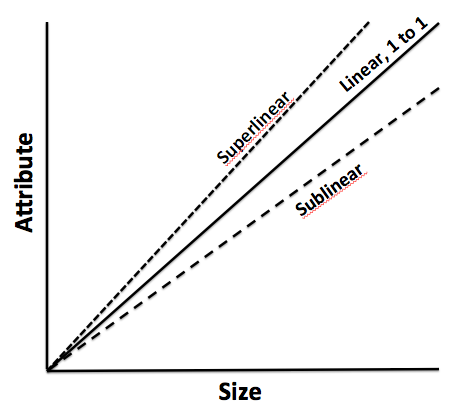

Scaling refers to how a system responds when its size changes. As mentioned earlier, does scaling follow a linear model? Do we need to consume 2X resources if we increase the size by 2X? How does scaling impact a Complex Physical System versus a Complex Adaptive System? Will a 2X impact on the initial state create perturbations in a CPS model which is equivalent to 2X? How would this work on a CAS model where the complexity is far from defined and understood because these systems are continuously evolving? Does half as big requires half as much or conversely twice as big requires twice as much? Once again, I have liberally dipped into this fantastic work by Geoffrey West to summarize, as best as possible, the definitions and implications. He proves that we cannot linearly extrapolate energy consumption and size: the world is smattered with evidence that undermines the linear extrapolation model. In fact, as you grow, you become more efficient with respect to energy consumption. The savings of energy due to growth in size is commonly called the economy of scale. His research also suggests two interesting results. When cities or social systems grow, they require an infrastructure to help with the growth. He discovered that it takes 85% resource consumption to grow the systems by 100%. Thus, there is a savings of 15% which is slightly lower than what has been studied on the biological front wherein organisms save 25% as they grow. He calls this sub linear scaling. In contrast, he also introduces the concept of super linear scaling wherein there is a 15% increasing returns to scale when the city or a social system grows. In other words, if the system grows by 100%, the positive returns with respect to such elements like patents, innovation, etc. will grow by 115%. In addition, the negative elements also grow in an equivalent manner – crime, disease, social unrest, etc. Thus, the growth in cities are supported by an efficient infrastructure that generates increasing returns of good and bad elements.

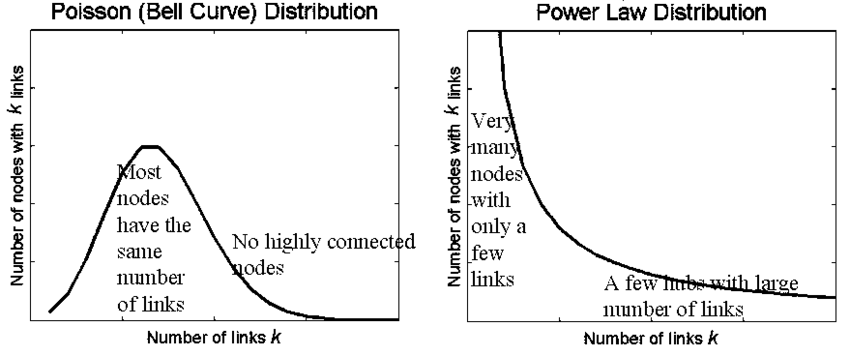

Max Kleiber, a Swiss chemist, in the 1930’s proposed the Kleiber’s law which sheds a lot of light on metabolic rates as energy consumption per unit of time. As mass increases so does the overall metabolic rate but it is not a linear relation – it obeys the power law. It stays that a living organism’s metabolic rate scales to the ¾ power of its mass. If the cat has a mass 100 times that of a mouse, the cat will metabolize about 100 ¾ = 31.63 times more energy per day rather than 100 times more energy per day. Kleiber’s law has led to the metabolic theory of energy and posits that the metabolic rate of organisms is the fundamental biological rate that governs most observed patters in our immediate ecology. There is some ongoing debate on the mechanism that allows metabolic rate to differ based on size. One mechanism is that smaller organisms have higher surface area to volume and thus needs relatively higher energy versus large organisms that have lower surface area to volume. This assumes that energy consumption occurs across surface areas. However, there is another mechanism that argues that energy consumption happens when energy needs are distributed through a transport network that delivers and synthesizes energy. Thus, smaller organisms do not have as a rich a network as large organisms and thus there is greater energy efficiency usage among smaller organisms than larger organisms. Either way, the implications are that body size and temperature (which is a result of internal activity) provide fundamental and natural constraints by which our ecological processes are governed. This leads to another concept called finite time singularity which predicts that unbounded growth cannot be sustained because it would need infinite resources or some K factor that would allow it to increase. The K factor could be innovation, a structural shift in how humans and objects cooperate, or even a matter of jumping on a spaceship and relocating to Mars.

We are getting bigger faster. That is real. The specter of a dystopian future hangs upon us like the sword of Damocles. The thinking is that this rate of growth and scale is not sustainable since it is impossible to marshal the resources to feed the beast in an adequate and timely manner. But interestingly, if we were to dig deeper into history – these thoughts prevailed in earlier times as well but perhaps at different scale. In 1798 Thomas Robert Malthus famously predicted that short-term gains in living standards would inevitably be undermined as human population growth outstripped food production, and thereby drive living standards back toward subsistence. Humanity thus was checkmated into an inevitable conclusion: a veritable collapse spurred by the tendency of population to grow geometrically while food production would increase only arithmetically. Almost two hundred years later, a group of scientists contributed to the 1972 book called Limits to Growth which had similar refrains like Malthus: the population is growing and there are not enough resources to support the growth and that would lead to the collapse of our civilization. However, humanity has negotiated those dark thoughts and we continue to prosper. If indeed, we are governed by this finite time singularity, we are aware that human ingenuity has largely won the day. Technology advancements, policy and institutional changes, new ways of collaboration, etc. have emerged to further delay this “inevitable collapse” that could be result of more mouths to feed than possible. What is true is that the need for new innovative models and new ways of doing things to solve the global challenges wrought by increased population and their correspondent demands will continue to increase at a quicker pace. Once could thus argue that the increased pace of life would not be sustainable. However, that is not a plausible hypothesis based on our assessment of where we are and where we have been.

Let us turn our attention to a business. We want the business to grow or do we want the business to scale? What is the difference? To grow means that your company is adding resources or infrastructure to handle increased demand, at a cost which is equivalent to the level of increased revenue coming in. Scaling occurs when the business is growing faster than the resources that are being consumed. We have already explored that outlier when you grow so big that you are crushed by your weight. It is that fact which limits the growth of organism regardless of issues related to scale. Similarly, one could conceivably argue that there are limits to growth of a company and might even turn to history and show that a lot of large companies of yesteryears have collapsed. However, it is also safe to say that large organizations today are by several factors larger than the largest organizations in the past, and that is largely on account of accumulated knowledge and new forms of innovation and collaboration that have allowed that to happen. In other words, the future bodes well for even larger organizations and if those organizations indeed reach those gargantuan size, it is also safe to draw the conclusion that they will be consuming far less resources relative to current organizations, thus saving more energy and distributing more wealth to the consumers.

Thus, scaling laws limit growth when it assumes that everything else is constant. However, if there is innovation that leads to structural changes of a system, then the limits to growth becomes variable. So how do we effect structural changes? What is the basis? What is the starting point? We look at modeling as a means to arrive at new structures that might allow the systems to be shaped in a manner such that the growth in the systems are not limited by its own constraints of size and motion and temperature (in physics parlance). Thus, a system is modeled at a presumably small scale but with the understanding that as the system is increases in size, the inner workings of emergent complexity could be a problem. Hence, it would be prudent to not linearly extrapolate the model of a small system to that of a large one but rather to exponential extrapolate the complexity of the new system that would emerge. We will discuss this in later articles, but it would be wise to keep this as a mental note as we forge ahead and refine our understanding of scale and its practical implications for our daily consumption.